Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in

Multiple Choice Question in 049

Multiple Choice Question in 020/2016

Multiple Choice Question in -current-affairs-2016

Multiple Choice Question in 2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in KPSC

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. Scriber points are very

(A): Multi-point

(B): Sharp point

(C): Single point

(D): Knurled point

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

kerala-psc

TRADESMAN---TURNING---TECHNICAL-EDUCATION

013/2016

Show Similar Question And Answers

QA->Which material is very hard and very ductile?....

QA->ISOBARS connect points of equal :....

QA->The team which positions the last spot in both Fair play award and winning points standings of IPL-2009?....

QA->The line joining points of equal dip are called:....

QA->League or Nations was formed on the basis of the 'Fourteen Points' put forward by ?....

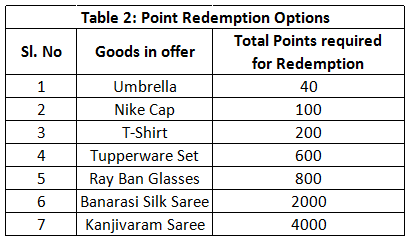

MCQ-> In order to quantify the intangibles and incentives to the multi brand dealers (dealers who stock multiple goods as well as competing brands) and the associated channel members, a

Company(X)

formulates a point score card, which is called as brand building points. This brand building point is added to the sales target achieved points for redemption. The sales target achieved point is allotted as per the table 3 of this question. The sum of brand building point and sales achieved points is the total point that can be redeemed by the dealer against certain goods, as shown in the second table.

The detail of the system is shown in the tables below

There are 10 multi brand dealers in Nasik and the sales that they have achieved in the end of a quarter are:

Maheshwari & Co has Company X signage along with other brand signage in the main entrance of the store, the exterior walls of the store have the painting of only company X, the side wall in the interior has the painting of Company X. The POP display of Company X is above the eye level with other brands while the stacking of goods of Company X is in the back row of the shelves. The brand building points when combined with the sales achieved points amounts to the total points that a dealer can accumulate in a quarter. The number of Tupperware Sets that Maheshwari & Co can redeem after the quarter (July to September) is?

....

MCQ->Scriber points are very....

MCQ->A graph may be defined as a set of points connected by lines called edges. Every edge connects a pair of points. Thus, a triangle is a graph with 3 edges and 3 points. The degree of a point is the number of edges connected to it. For example, a triangle is a graph with three points of degree 2 each. Consider a graph with 12 points. It is possible to reach any point from any point through a sequence of edges. The number of edges, e, in the graph must satisfy the condition....

MCQ-> Read the following passage based on an Interview to answer the given questions based on it. Certain words are printed in bold to help you locate them while answering some of the questions.A spate of farmer suicides linked to harassment by recovery agents employed by micro finance institutions (MFLs) in Andhra Pradesh

spurned

the state government to bring in regulation to protect consumer interests. But, while the Bill has brought into sharp focus the need for consumer protection, it tries to micro-manage MFI operations and in the process it could

scuttle

some of the crucial bene ts that MFIs bring to farmers, says the author of Micro nance India, State Of The Sec-for Report 2010. In an interview he points out that prudent regulation can ensure the original goal of the MFIs - social uplift of the poor.

Do you feel the AP Bill to regulate Mils is well thought out? Does it ensure fairness to the borrowers and the long-term health of the sector?

The AP Bill has brought into sharp focus the need for customer protection in four critical areas. First is pricing. Second is lender's liability whether the lender can give too much loan without assessing the customer's ability to pay. Third is the structure of loan repayment - whether you can ask money on a weekly basis from people who don't produce weekly incomes. Fourth is the practices that attend to how you deal with defaults. But the Act should have looked at the positive bene ts that institutions could bring in, and where they need to be regulated in the interests of the customers. It should have brought only those features in. Say, you want the recovery practices to be consistent with what the customers can really

manage

. If the customer is aggrieved and complains that somebody is harassing him, then those complaints should be investigated by the District Rural Development Authority. Instead what the Bill says is that MF1s cannot go to the customer's premises to ask for recovery and that all transactions will be done in the Panchayat of ce. With great dif culty, MFIs brought services to the door of people. It is such a relief for the customers not to be spending time out going to banks or Panchayat of ces, which could be 10 km away in some cases. A facility which has brought some relief to people is being shut. Moreover, you are practically telling the MFI where it should do business and how it should do it.

Social responsibilities were inbuilt when the MIrls were rst conceived. If kills go for profit with loose regulations, how are they different from moneylenders?

Even among moneylenders there are very good people who take care of the customer's circumstance, and there are really bad ones. A large number of the MF1s are good and there are some who are coercive because of the kind of prices and processes they have adopted. But Moneylenders never got this organised. They did not have such a large footprint. An MFI brought in organisation, it mobilized the equity, it brought in commercial funding. It invested in systems. It appointed a large number of people. But some of them

exacted

a much higher price than they should have. They wanted to break even very fast and greed did take over in some cases.

Are the for-profit 'Ms the only ones harassing people for recoveries?

Some not-for-profit out ts have also adopted the same kind of recovery methods. That may be because you have to show that you are very ef cient in your recovery methods and that your portfolio is of a very high quality if you want to get commercial funding from a bank. In fact, among for-profits there are many who have sensible recovery practices. Some have fortnightly recovery, some have monthly recovery. So we have differing practices. We just describe a few dominant ones and assume every for-profit MFI operates like that. How can you introduce regulations to ensure social upliftment in a sector that is moving towards for-profit models? I am not really concerned whether someone wants to make a profit or not The bottom-line for me is customer protection. The rst area is fair practices. Are you telling your customers how the loan is structured ? Are you being transparent about your performance? There should also be a lender's liability attached to what you do. Suppose you lend excessively to a customer without assessing their ability to service the loan, you have to take the hit. Then there's the question of limiting returns. You can say that an MFI cannot have a return on assets more than X, a return on equity of more than Y. Then suppose there is a privately promoted MFI, there should be a regulation to ensure the MFI cannot access equity markets till a certain amount of time. MFIs went to markets perhaps because of the need to grow too big too fast. The government thought they were making profit off the poor, and that's an indirect reason why they decided to clamp down on MF1s. If you say an MFI won't go to capital market, then it will keep political compulsions under rein.Which of the following best explains "structure of loan repayment" in this context of the rst question asked to the author ?....

MCQ->I have a total of Rs. 1,000. Item A costs Rs. 110, item B costs Rs. 90, item C costs Rs. 70, item D costs Rs. 40 and item E costs Rs. 45. For every item D that I purchase, I must also buy two of item B. For every item A, I must buy one of item C. For every item E, I must also buy two of item D and one of item B. For every item purchased I earn 1,000 points and for every rupee not spent I earn a penalty of 1,500 points. My objective is to maximise the points I earn. What is the number of items that I must purchase to maximise my points?....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions

There are 10 multi brand dealers in Nasik and the sales that they have achieved in the end of a quarter are:

There are 10 multi brand dealers in Nasik and the sales that they have achieved in the end of a quarter are:

Maheshwari & Co has Company X signage along with other brand signage in the main entrance of the store, the exterior walls of the store have the painting of only company X, the side wall in the interior has the painting of Company X. The POP display of Company X is above the eye level with other brands while the stacking of goods of Company X is in the back row of the shelves. The brand building points when combined with the sales achieved points amounts to the total points that a dealer can accumulate in a quarter. The number of Tupperware Sets that Maheshwari & Co can redeem after the quarter (July to September) is?

Maheshwari & Co has Company X signage along with other brand signage in the main entrance of the store, the exterior walls of the store have the painting of only company X, the side wall in the interior has the painting of Company X. The POP display of Company X is above the eye level with other brands while the stacking of goods of Company X is in the back row of the shelves. The brand building points when combined with the sales achieved points amounts to the total points that a dealer can accumulate in a quarter. The number of Tupperware Sets that Maheshwari & Co can redeem after the quarter (July to September) is?