Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in

Multiple Choice Question in 049

Multiple Choice Question in -current-affairs-2016

Multiple Choice Question in 2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. Prepaid expenses Account is a

(A): Real account

(B): Personal account

(C): Nominal account

(D): Capital account

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->Voyage Account is ............account:....

QA->Deputy Speaker of the House of Lords who resigned recently following his suspension from the House over his expenses claims?....

QA->Travel expenses of a Government servant for travel on duty connected with an outside body is debitable to:....

QA->……….. is that segment of activity of a business which is responsible for both revenue and expenses.....

QA->The Raslitilya Swasthya Bima Yojana provides cover for hospitalization expenses up to _____?....

MCQ-> Read the following passage carefully and answer the questions given below it. Certain words are printed in bold to help you to locate them while answering some of the questions.A large majority of the poor in India are outside the formal banking system. The policy of financial inclusion sets out to

remedy

this by making available a basic banking ‘no frills’ account either with nil or very minimum balances as well as charges that would make such accounts

accessible

to vast sections of the population. However, the mere opening of a bank account in the name of every household or adult person may not be enough, unless these accounts and financial services offered to them are used by the account holders. At present, commercial banks do not find it viable to provide services to the poor especially in the rural areas because of huge transaction costs, low volumes of savings in the accounts, lack of information on the account holder, etc. For the poor. interacting with the banks with their paper work, economic costs of going to the bank and the need for flexibility in their accounts, make them turn to other informal channels or other institutions. Thus, there are constraints on both the supply and the demand side.Till now, banks were looking at these accounts from a

purely

credit perspective. Instead, they should look at this from the point of view of meeting the huge need of the poor for savings. Poor households want to save and, contrary to the common perception, do have the funds to save, but lack control. Informal mutual saving systems like the Rotating Savings and Credit Associations (ROSCAs), widespread in Africa, and ‘thrift and credit groups’ in India

demonstrate

that poor households save. For the poor household, which lack access to the formal insurance system and the credit system, savings provide a safety net and help them tide over crises. Savings can also keep them away from the clutches of moneylenders, make formal institutions more favourable to lending to them, encourage investment and make them shift to more productive activities, as they may invest in slightly more risky activities which have an overall higher rate of return.Research shows the efficacy of informal institutions in increasing the savings of the small account holders. An MFI in the Philippines, which had existing account holders, was studied. They offered new products with ‘commitment features’. One type had withdrawal restrictions in the sense that it required individuals to restrict their right to withdraw any funds from their own accounts until they reached a self-specified and documented goal. The other type was deposit options. Clients could purchase a locked box for a small fee. The key was with the bank and the client has to bring the box to the bank to make the deposit. He could not dip into the savings even if he wanted to. These accounts did not pay extra money and were illiquid. Surprisingly, these products were popular even though these had restrictions. Results showed that those who opted for these accounts with restrictions had substantially greater savings rates than those who did not. The policy of financial inclusion can be a success if financial inclusion focuses onboth saving needs and credit needs, having a diversified product portfolio for the poor but recognising that self-control problems need to be addressed by having commitment devices. The products with commitment features should be

optional

. Furthermore transaction costs for the poor could be cut down, by making innovative use of technology available and offering mobile vans with ATM and deposit collection features which could visit villages periodically.What is the aim of the financial inclusion policy ?

....

MCQ->Prepaid expenses Account is a....

MCQ->Ln a bank the account numbers are all 8 digit numbers, and they all start with the digit 2. So, an account number can be represented as $$2x_1x_2x_3x_4x_5x_6x_7$$. An account number is considered to be a ‘magic’ number if $$x_{1}x_{2}x_{3}$$ is exactly the same as $$x_{4}x_{5}x_{6}$$ or $$x_{5}x_{6}x_{7}$$ or both. $$X_{i}$$ can take values from 0 to 9, but 2 followed by seven $$0_{s}$$ is not a valid account number. What is the maximum possible number of customers having a ‘magic’ account number?....

MCQ->Statement: A sentence in the letter to the candidates called for written examination - 'You have to bear your expenses on travel etc'. Assumptions: If not clarified all the candidates may claim reimbursement of expenses. Many organizations reimburse expenses on travel to candidates called for written examination. ....

MCQ-> Read the following caselet and choose the best alternative

The BIG and Colourful Company

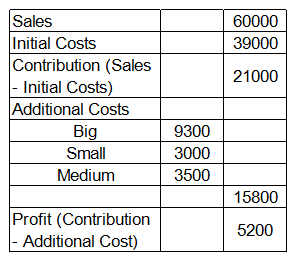

You are running "BIG and Colourful (BnC)" company that sells books to customers through three retail formats: a. You can buy books from bookstores, b. You can buy books from supermarket, c. You can order books over the Internet (Online). Your manager has an interesting way of classifying expenses: some of the expenses are classified in terms of size: Big, Small and Medium; and others are classified in terms of the colors, Red, Yellow, Green and Violet. The company has a history of categorizing overall costs into initial costs and additional costs. Additional costs are equal to the sum of Big, Small and Medium expenses. There are two types of margins, contribution (sales minus initial costs) and profit (contribution minus additional costs). Given below is the data about sales and costs of BnC:

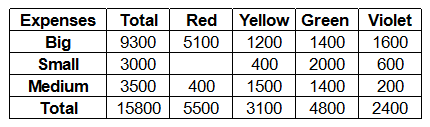

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below:

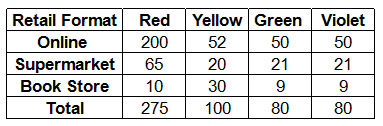

Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below:

Read the following statements: Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2. Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below:

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below: Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below:

Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below: Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....

Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....