Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. The ‘more mega store’ retail chain belongs to which Indian Industry ?

(A): Reliance Industry

(B): Bharti Enterprises

(C): Aditya Birla Group

(D): None of these

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

SSC CGL 2014 Tier 1 19 Oct shift 2

Show Similar Question And Answers

QA->Star Hyper is a chain of retail stores in India created as a JV between Tatas and which global retail chain ?....

QA->A large retail store.....

QA->Which animal belongs to the family in which Panda belongs?....

QA->Parliament of which country has allowed 51% Foreign Direct Investment(FDI) in the country"s multi-brand retail sector on December 7, 2012?....

QA->The StateGovernment of Odisha on December 24 has named Rs. 7,600 crore Mega LiftIrrigation Scheme after which freedom fighter as a mark ofrespect?....

MCQ->

Read the following passage to answer the given question based on it. Some words/phrases are printed in bold to help you locate them while answering some of the questions.

Organized retail has “

fuelled

” new growth categories like liquid hand wash, breakfast cereals and pet foods in the consumer goods industry accounting for almost 50% of their sales said data from market search firm Nielsen The figures showed some of these new categories got more than 40% of their business from modern retail outlets.The data also suggests how products in these categories reach the neighbourhood kirana stores after they have established themselves in modern trade While grocers continue to be an important channel for the new and evolving categories we saw an increased presence of the high end products in modern trade For example

premium

products in laundry detergents dishwashing car air fresheners and surface care increased in availability through this format as these products are aimed at “

affluent

” consumers who are more likely to shop in supermarket/hypermarket outlets and who are willing to pay more for specialized products Some other categories that have grown exceptionally and now account for bulk of the sales from modern retail are frozen and With the evolution of modern trade our growth in this channel has been healthy as it is for several other categories Modern retail is an important part of our business said managing director Kellogg India. What modern retail offers to companies experimenting with new categories is the chance to educate customers which was not the case with a general trade store Category creation and market development starts with modern trade but as more consumer start consuming this category they “penetrate into other channels” said president food FMCG category Future Group the country’s largest retailer which operates stores like Big Bazaar But a point to note here is that modern retailers themselves push their own private brands in these very categories and can emerge as a big threat for the consumers goods and foods companies For instance Big Bazaar’s private label Clean Mate is hugely popular and sells more than a brand like Harpic in its own stores So there is a certain amount of conflict and competition that will play out over the next few years which the FMCG companies will have to watch out for said KPMG’s executive director (retail) In the past there have been instances of retailers boycotting products from big FMCG players on the issue of margins but as modern retail become increasingly significant for “

pushing

” new categories experts say we could see more partnerships being forged between retailers and FMCG companies Market development for new categories takes time so brand wars for leadership and consumer franchise will be fought on the modern retail platform A new brand can overnight compete with “

established

” companies by trying up with few retailers in these categories president of Future Group addedWhich of the following is being referred to as new growth category ?

....

MCQ-> Read the passage carefully and answer the questions given at the end of each passage:Turning the business involved more than segmenting and pulling out of retail. It also meant maximizing every strength we had in order to boost our profit margins. In re-examining the direct model, we realized that inventory management was not just core strength; it could be an incredible opportunity for us, and one that had not yet been discovered by any of our competitors. In Version 1.0 the direct model, we eliminated the reseller, thereby eliminating the mark-up and the cost of maintaining a store. In Version 1.1, we went one step further to reduce inventory inefficiencies. Traditionally, a long chain of partners was involved in getting a product to the customer. Let’s say you have a factory building a PC we’ll call model #4000. The system is then sent to the distributor, which sends it to the warehouse, which sends it to the dealer, who eventually pushes it on to the consumer by advertising, “I’ve got model #4000. Come and buy it.” If the consumer says, “But I want model #8000,” the dealer replies, “Sorry, I only have model #4000.” Meanwhile, the factory keeps building model #4000s and pushing the inventory into the channel. The result is a glut of model #4000s that nobody wants. Inevitably, someone ends up with too much inventory, and you see big price corrections. The retailer can’t sell it at the suggested retail price, so the manufacturer loses money on price protection (a practice common in our industry of compensating dealers for reductions in suggested selling price). Companies with long, multi-step distribution systems will often fill their distribution channels with products in an attempt to clear out older targets. This dangerous and inefficient practice is called “channel stuffing”. Worst of all, the customer ends up paying for it by purchasing systems that are already out of date Because we were building directly to fill our customers’ orders, we didn’t have finished goods inventory devaluing on a daily basis. Because we aligned our suppliers to deliver components as we used them, we were able to minimize raw material inventory. Reductions in component costs could be passed on to our customers quickly, which made them happier and improved our competitive advantage. It also allowed us to deliver the latest technology to our customers faster than our competitors. The direct model turns conventional manufacturing inside out. Conventional manufacturing, because your plant can’t keep going. But if you don’t know what you need to build because of dramatic changes in demand, you run the risk of ending up with terrific amounts of excess and obsolete inventory. That is not the goal. The concept behind the direct model has nothing to do with stockpiling and everything to do with information. The quality of your information is inversely proportional to the amount of assets required, in this case excess inventory. With less information about customer needs, you need massive amounts of inventory. So, if you have great information – that is, you know exactly what people want and how much - you need that much less inventory. Less inventory, of course, corresponds to less inventory depreciation. In the computer industry, component prices are always falling as suppliers introduce faster chips, bigger disk drives and modems with ever-greater bandwidth. Let’s say that Dell has six days of inventory. Compare that to an indirect competitor who has twenty-five days of inventory with another thirty in their distribution channel. That’s a difference of forty-nine days, and in forty-nine days, the cost of materials will decline about 6 percent. Then there’s the threat of getting stuck with obsolete inventory if you’re caught in a transition to a next- generation product, as we were with those memory chip in 1989. As the product approaches the end of its life, the manufacturer has to worry about whether it has too much in the channel and whether a competitor will dump products, destroying profit margins for everyone. This is a perpetual problem in the computer industry, but with the direct model, we have virtually eliminated it. We know when our customers are ready to move on technologically, and we can get out of the market before its most precarious time. We don’t have to subsidize our losses by charging higher prices for other products. And ultimately, our customer wins. Optimal inventory management really starts with the design process. You want to design the product so that the entire product supply chain, as well as the manufacturing process, is oriented not just for speed but for what we call velocity. Speed means being fast in the first place. Velocity means squeezing time out of every step in the process. Inventory velocity has become a passion for us. To achieve maximum velocity, you have to design your products in a way that covers the largest part of the market with the fewest number of parts. For example, you don’t need nine different disk drives when you can serve 98 percent of the market with only four. We also learned to take into account the variability of the lost cost and high cost components. Systems were reconfigured to allow for a greater variety of low-cost parts and a limited variety of expensive parts. The goal was to decrease the number of components to manage, which increased the velocity, which decreased the risk of inventory depreciation, which increased the overall health of our business system. We were also able to reduce inventory well below the levels anyone thought possible by constantly challenging and surprising ourselves with the result. We had our internal skeptics when we first started pushing for ever-lower levels of inventory. I remember the head of our procurement group telling me that this was like “flying low to the ground 300 knots.” He was worried that we wouldn’t see the trees.In 1993, we had $2.9 billion in sales and $220 million in inventory. Four years later, we posted $12.3 billion in sales and had inventory of $33 million. We’re now down to six days of inventory and we’re starting to measure it in hours instead of days. Once you reduce your inventory while maintaining your growth rate, a significant amount of risk comes from the transition from one generation of product to the next. Without traditional stockpiles of inventory, it is critical to precisely time the discontinuance of the older product line with the ramp-up in customer demand for the newer one. Since we were introducing new products all the time, it became imperative to avoid the huge drag effect from mistakes made during transitions. E&O; – short for “excess and obsolete” - became taboo at Dell. We would debate about whether our E&O; was 30 or 50 cent per PC. Since anything less than $20 per PC is not bad, when you’re down in the cents range, you’re approaching stellar performance.Find out the TRUE statement:

....

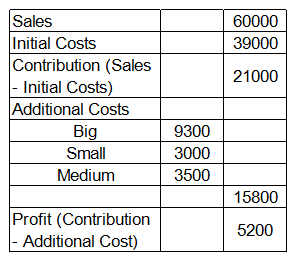

MCQ-> Read the following caselet and choose the best alternative

The BIG and Colourful Company

You are running "BIG and Colourful (BnC)" company that sells books to customers through three retail formats: a. You can buy books from bookstores, b. You can buy books from supermarket, c. You can order books over the Internet (Online). Your manager has an interesting way of classifying expenses: some of the expenses are classified in terms of size: Big, Small and Medium; and others are classified in terms of the colors, Red, Yellow, Green and Violet. The company has a history of categorizing overall costs into initial costs and additional costs. Additional costs are equal to the sum of Big, Small and Medium expenses. There are two types of margins, contribution (sales minus initial costs) and profit (contribution minus additional costs). Given below is the data about sales and costs of BnC:

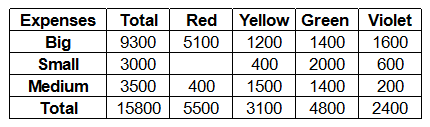

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below:

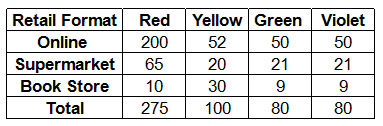

Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below:

Read the following statements: Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2. Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....

MCQ-> The controversy over genetically modified food continues unabated in the West. Genetic modification (GM) is the science by which the genetic material of a plant is altered, perhaps to make it more resistant to pests or killer weeds, or to enhance its nutritional value. Many food biotechnologists claim that GM will be a major contribution of science to mankind in the 21st century. On the other hand, large numbers of opponents, mainly in Europe, claim that the benefits of GM are a myth propagated by multinational corporations to increase their profits, that they pose a health hazard, and have therefore called for government to ban the sale of genetically-modified food.The anti-GM campaign has been quite effective in Europe, with several European Union member countries imposing a virtual ban for five years over genetically-modified food imports. Since the genetically-modified food industry is particularly strong in the United States of America, the controversy also constitutes another chapter in the US-Europe skirmishes which have become particularly acerbic after the US invasion of Iraq.To a large extent, the GM controversy has been ignored in the Indian media, although Indian biotechnologists have been quite active in GM research. Several groups of Indian biotechnologists have been working on various issues connected with crops grown in India. One concrete achievement which has recently figured in the news is that of a team led by the former vice-chancellor of Jawaharlal Nehru university, Asis Datta — it has successfully added an extra gene to potatoes to enhance the protein content of the tuber by at least 30 percent. It is quite likely that the GM controversy will soon hit the headlines in India since a spokesperson of the Indian Central government has recently announced that the government may use the protato in its midday meal programme for schools as early as next year.Why should “scientific progress”, with huge potential benefits to the poor and malnourished, be so controversial? The anti-GM lobby contends that pernicious propaganda has vastly exaggerated the benefits of GM and completely evaded the costs which will have to be incurred if the genetically-modified food industry is allowed to grow unchecked. In particular, they allude to different types of costs.This group contends that the most important potential cost is that the widespread distribution and growth of genetically-modified food will enable the corporate world (alias the multinational corporations – MNCs) to completely capture the food chain. A “small” group of biotech companies will patent the transferred genes as well as the technology associated with them. They will then buy up the competing seed merchants and seed-breeding centers, thereby controlling the production of food at every possible level. Independent farmers, big and small, will be completely wiped out of the food industry. At best, they will be reduced to the status of being subcontractors.This line of argument goes on to claim that the control of the food chain will be disastrous for the poor since the MNCs, guided by the profit motive, will only focus on the high-value food items demanded by the affluent. Thus, in the long run, the production of basic staples which constitute the food basket of the poor will taper off. However, this vastly overestimates the power of the MNCs. Even if the research promoted by them does focus on the high-value food items, much of biotechnology research is also funded by governments in both developing and developed countries. Indeed, the protato is a by-product of this type of research. If the protato passes the field trials, there is no reason to believe that it cannot be marketed in the global potato market. And this type of success story can be repeated with other basic food items.The second type of cost associated with the genetically modified food industry is environmental damage. The most common type of “genetic engineering” involved gene modification in plants designed to make them resistant to applications of weed-killers. This then enables farmers to use massive dosages of weedkillers so as to destroy or wipe out all competing varieties of plants in their field. However, some weeds through genetically-modified pollen contamination may acquire resistance to a variety of weed-killers. The only way to destroy these weeds is through the use of ever-stronger herbicides which are poisonous and linger on in the environment.The author doubts the anti-GM lobby’s contention that MNC control of the food chain will be disastrous for the poor because

....

MCQ->The ‘more mega store’ retail chain belongs to which Indian Industry ?....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below:

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below: Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below:

Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below: Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....

Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....