Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in -current-affairs-2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. In a class C amplifier, full cycle conductor of the current is achieved by employing

(A): tuned circuit

(B): transformers

(C): complementary pair

(D): Push pull configuration

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->There are 50 students in a class. In a class test 22 students get 25 marks each, 18 students get 30 marks each. Each of the remaining gets 16 marks. The average mark of the whole class is :....

QA->In a class of 20 students the average age is 16 years.If the age of the class teacher is added to that of students,the average age of the class becomes 17 years.What is the age of the teacher?....

QA->Which substance is a bad conductor of electricity but a good conductor of heat?....

QA->When current flows through a metallic conductor, heat is produced, known as :....

QA->In a class of 60 students, 55% are boys. The number of girls in the class is :....

MCQ->In a class C amplifier, full cycle conductor of the current is achieved by employing....

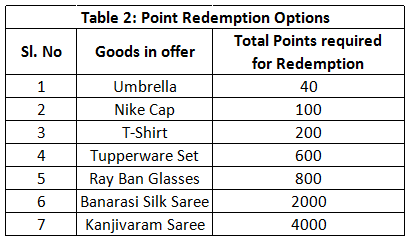

MCQ-> In order to quantify the intangibles and incentives to the multi brand dealers (dealers who stock multiple goods as well as competing brands) and the associated channel members, a

Company(X)

formulates a point score card, which is called as brand building points. This brand building point is added to the sales target achieved points for redemption. The sales target achieved point is allotted as per the table 3 of this question. The sum of brand building point and sales achieved points is the total point that can be redeemed by the dealer against certain goods, as shown in the second table.

The detail of the system is shown in the tables below

There are 10 multi brand dealers in Nasik and the sales that they have achieved in the end of a quarter are:

Maheshwari & Co has Company X signage along with other brand signage in the main entrance of the store, the exterior walls of the store have the painting of only company X, the side wall in the interior has the painting of Company X. The POP display of Company X is above the eye level with other brands while the stacking of goods of Company X is in the back row of the shelves. The brand building points when combined with the sales achieved points amounts to the total points that a dealer can accumulate in a quarter. The number of Tupperware Sets that Maheshwari & Co can redeem after the quarter (July to September) is?

....

MCQ-> Study the following information carefully and answer the questions given below :P, Q, R, S, T and M are six students of a school, one each studies in Class 1-VI. Each of them has a favourite colour from red, black, blue, yellow, pink and green, not necessarily in the same order. Q likes black and does not study in Class IV or V. The one who studies in class IV does not like green. P studies in class II, M likes blue and does suidy in class IV. The one who likes ,t•Ilow studies in class VI. S likes pink itu I studies in class I. R does not study at class VI.In which class does R study ?

....

MCQ-> There are two Trains, Train-A and Train-B. Both Trains have four different types of Coaches viz. General Coaches, Sleeper Coaches, First Class Coaches and AC Coaches. In Train A there are total 700 passengers. Train-B has thirty percent more passengers than Train A. Twenty percent of the passengers of Train-A are in General Coaches. One-fourth of the total number of passengers of Train-A are in AC coaches. Twenty three percent of the passengers of Train-A are in Sleeper Class Coaches. Remaining passengers of Train-A are in first class coaches. Total number of passengers in AC coaches in both the trains together is 480. Thirty percent of the number of passengers of Train-B is in Sleeper Class Coaches. Ten percent of the total passengers of Train-B are in first class coaches. Remaining passengers of Train-B are in general class coaches.What is the respective ratio between the number of passengers in first class Coaches of Train A and number of passengers in Sleeper Class coaches of Train - B ?

....

MCQ-> I suggest that the essential character of the Trade Cycle and, especially, the regularity of time-sequence and of duration which justifies us in calling it a cycle, is mainly due to the way in which the marginal efficiency of capital fluctuates. The Trade Cycle is best regarded, I think, as being occasioned by a cyclical change in the marginal efficiency of capital, though complicated and often aggravated by associated changes in the other significant short period variables of the economic system.By a cyclical movement we mean that as the system progresses in, e.g. the upward direction, the forces propelling it upwards at first gather force and have a cumulative effect on one another but gradually lose their strength until at a certain point they tend to be replaced by forces operating in the opposite direction; which in turn gather force for a time and accentuate one another, until they too, having reached their maximum development, wane and give place to their opposite. We do not, however, merely mean by a cyclical movement that upward and downward tendencies, once started, do not persist for ever in the same direction but are ultimately reversed. We mean also that there is some recognizable degree of regularity in the time-sequence and duration of the upward and downward movements. There is, however, another characteristic of what we call the Trade Cycle which our explanation must cover if it is to be adequate; namely, the phenomenon of the ‘crisis’ the fact that the substitution of a downward for an upward tendency often takes place suddenly and violently, whereas there is, as a rule, no such sharp turning-point when an upward is substituted for a downward tendency. Any fluctuation in investment not offset by a corresponding change in the propensity to consume will, of course, result in a fluctuation in employment. Since, therefore, the volume of investment is subject to highly complex influences, it is highly improbable that all fluctuations either in investment itself or in the marginal efficiency of capital will be of a cyclical character.We have seen above that the marginal efficiency of capital depends, not only on the existing abundance or scarcity of capital-goods and the current cost of production of capital- goods, but also on current expectations as to the future yield of capital-goods. In the case of durable assets it is, therefore, natural and reasonable that expectations of the future should play a dominant part in determining the scale on which new investment is deemed advisable. But, as we have seen, the basis for such expectations is very precarious. Being based on shifting and unreliable evidence, they are subject to sudden and violent changes. Now, we have been accustomed in explaining the ‘crisis’ to lay stress on the rising tendency of the rate of interest under the influence of the increased demand for money both for trade and speculative purposes. At times this factor may certainly play an aggravating and, occasionally perhaps, an initiating part. But I suggest that a more typical, and often the predominant, explanation of the crisis is, not primarily a rise in the rate of interest, but a sudden collapse in the marginal efficiency of capital. The later stages of the boom are characterized by optimistic expectations as to the future yield of capital goods sufficiently strong to offset their growing abundance and their rising costs of production and, probably, a rise in the rate of interest also. It is of the nature of organized investment markets, under the influence of purchasers largely ignorant of what they are buying and of speculators who are more concerned with forecasting the next shift of market sentiment than with a reasonable estimate of the future yield of capital-assets, that, when disillusion falls upon an over-optimistic and over- bought market, it should fall with sudden and even catastrophic force. Moreover, the dismay and uncertainty as to the future which accompanies a collapse in the marginal efficiency of capital naturally precipitates a sharp increase in liquidity-preference and hence a rise in the rate of interest. Thus the fact that a collapse in the marginal efficiency of capital tends to be associated with a rise in the rate of interest may seriously aggravate the decline in investment. But the essence of the situation is to be found, nevertheless, in the collapse in the marginal efficiency of capital, particularly in the case of those types of capital which have been contributing most to the previous phase of heavy new investment. Liquidity preference, except those manifestations of it which are associated with increasing trade and speculation, does not increase until after the collapse in the marginal efficiency of capital. It is this, indeed, which renders the slump so intractable. Which of the following does not describe the features of cyclical movement?

....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions

There are 10 multi brand dealers in Nasik and the sales that they have achieved in the end of a quarter are:

There are 10 multi brand dealers in Nasik and the sales that they have achieved in the end of a quarter are:

Maheshwari & Co has Company X signage along with other brand signage in the main entrance of the store, the exterior walls of the store have the painting of only company X, the side wall in the interior has the painting of Company X. The POP display of Company X is above the eye level with other brands while the stacking of goods of Company X is in the back row of the shelves. The brand building points when combined with the sales achieved points amounts to the total points that a dealer can accumulate in a quarter. The number of Tupperware Sets that Maheshwari & Co can redeem after the quarter (July to September) is?

Maheshwari & Co has Company X signage along with other brand signage in the main entrance of the store, the exterior walls of the store have the painting of only company X, the side wall in the interior has the painting of Company X. The POP display of Company X is above the eye level with other brands while the stacking of goods of Company X is in the back row of the shelves. The brand building points when combined with the sales achieved points amounts to the total points that a dealer can accumulate in a quarter. The number of Tupperware Sets that Maheshwari & Co can redeem after the quarter (July to September) is?