Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in

Multiple Choice Question in 049

Multiple Choice Question in 2016

Multiple Choice Question in -current-affairs-2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. Doping semiconductive material is the process of putting a small amount of pentavalent or trivalent atoms in with tetravalent atoms.

(A): True

(B): False

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->American former professional road racing cyclist who has banned from cycling for life for doping offenses by the United States Anti-Doping Agency (USADA) in 2012?....

QA->Wherethe National Anti-Doping Laboratory is located whose accreditation wassuspended by the World Anti-Doping Agency (WADA) on 21 April 2016?....

QA->Process of putting up previous correspondence for disposal of a case is :....

QA->Which becomes first state of India for putting records of all 13,040 village Panchayats online?....

QA->Government of which country began a partial shutdown on October 1, 2013 for the first time in 17 years, potentially putting up to 1 million workers on unpaid leave, closing national parks and stalling medical research projects?....

MCQ->Doping semiconductive material is the process of putting a small amount of pentavalent or trivalent atoms in with tetravalent atoms.....

MCQ-> People are continually enticed by such "hot" performance, even if it lasts for brief periods. Because of this susceptibility, brokers or analysts who have had one or two stocks move up sharply, or technicians who call one turn correctly, are believed to have established a credible record and can readily find market followings. Likewise, an advisory service that is right for a brief time can beat its drums loudly. Elaine Garzarelli gained near immortality when she purportedly "called" the 1987 crash. Although, as the market strategist for Shearson Lehman, her forecast was never published in a research report, nor indeed communicated to its clients, she still received widespread recognition and publicity for this call, which was made in a short TV interview on CNBC. Still, her remark on CNBC that the Dow could drop sharply from its then 5300 level rocked an already nervous market on July 23, 1996. What had been a 40-point gain for the Dow turned into a 40-point loss, a good deal of which was attributed to her comments.The truth is, market-letter writers have been wrong in their judgments far more often than they would like to remember. However, advisors understand that the public considers short-term results meaningful when they are, more often than not, simply chance. Those in the public eye usually gain large numbers of new subscribers for being right by random luck. Which brings us to another important probability error that falls under the broad rubric of representativeness. Amos Tversky and Daniel Kahneman call this one the "law of small numbers.". The statistically valid "law of large numbers" states that large samples will usually be highly representative of the population from which they are drawn; for example, public opinion polls are fairly accurate because they draw on large and representative groups. The smaller the sample used, however (or the shorter the record), the more likely the findings are chance rather than meaningful. Yet the Tversky and Kahneman study showed that typical psychological or educational experimenters gamble their research theories on samples so small that the results have a very high probability of being chance. This is the same as gambling on the single good call of an advisor. The psychologists and educators are far too confident in the significance of results based on a few observations or a short period of time, even though they are trained in statistical techniques and are aware of the dangers.Note how readily people over generalize the meaning of a small number of supporting facts. Limited statistical evidence seems to satisfy our intuition no matter how inadequate the depiction of reality. Sometimes the evidence we accept runs to the absurd. A good example of the major overemphasis on small numbers is the almost blind faith investors place in governmental economic releases on employment, industrial production, the consumer price index, the money supply, the leading economic indicators, etc. These statistics frequently trigger major stock- and bond-market reactions, particularly if the news is bad. Flash statistics, more times than not, are near worthless. Initial economic and Fed figures are revised significantly for weeks or months after their release, as new and "better" information flows in. Thus, an increase in the money supply can turn into a decrease, or a large drop in the leading indicators can change to a moderate increase. These revisions occur with such regularity you would think that investors, particularly pros, would treat them with the skepticism they deserve. Alas, the real world refuses to follow the textbooks. Experience notwithstanding, investors treat as gospel all authoritative-sounding releases that they think pinpoint the development of important trends. An example of how instant news threw investors into a tailspin occurred in July of 1996. Preliminary statistics indicated the economy was beginning to gain steam. The flash figures showed that GDP (gross domestic product) would rise at a 3% rate in the next several quarters, a rate higher than expected. Many people, convinced by these statistics that rising interest rates were imminent, bailed out of the stock market that month. To the end of that year, the GDP growth figures had been revised down significantly (unofficially, a minimum of a dozen times, and officially at least twice). The market rocketed ahead to new highs to August l997, but a lot of investors had retreated to the sidelines on the preliminary bad news. The advice of a world champion chess player when asked how to avoid making a bad move. His answer: "Sit on your hands”. But professional investors don't sit on their hands; they dance on tiptoe, ready to flit after the least particle of information as if it were a strongly documented trend. The law of small numbers, in such cases, results in decisions sometimes bordering on the inane. Tversky and Kahneman‘s findings, which have been repeatedly confirmed, are particularly important to our understanding of some stock market errors and lead to another rule that investors should follow.Which statement does not reflect the true essence of the passage? I. Tversky and Kahneman understood that small representative groups bias the research theories to generalize results that can be categorized as meaningful result and people simplify the real impact of passable portray of reality by small number of supporting facts. II. Governmental economic releases on macroeconomic indicators fetch blind faith from investors who appropriately discount these announcements which are ideally reflected in the stock and bond market prices. III. Investors take into consideration myopic gain and make it meaningful investment choice and fail to see it as a chance of occurrence. IV. lrrational overreaction to key regulators expressions is same as intuitive statistician stumbling disastrously when unable to sustain spectacular performance.....

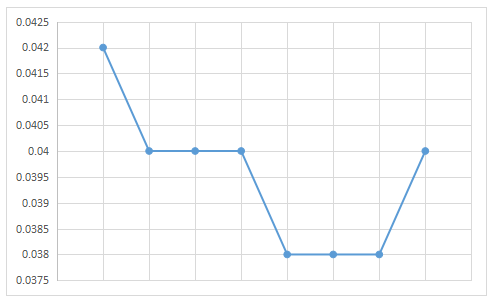

MCQ->The estimated material cost given in the table titled “Variable Cost Estimates of Mulchand Textiles” included the cost of material that gets spoiled in the production process. Mr. Sharma decomposed the estimated material cost into material spoilage cost and material usage cost, but he lost the data when his computer crashed. When he saw the following line diagram, here called that he measured the estimate of material spoilage cost per square feet of output on the y - axis and monthly output on the x - axis.

Estimated material usage cost per square feet of output.....

MCQ-> Read carefully the four passages that follow and answer the questions given at the end of each passage:PASSAGE I The most important task is revitalizing the institution of independent directors. The independent directors of a company should be faithful fiduciaries protecting, the long-term interests of shareholders while ensuring fairness to employees, investor, customer, regulators, the government of the land and society. Unfortunately, very often, directors are chosen based of friendship and, sadly, pliability. Today, unfortunately, in the majority of cases, independence is only true on paper.The need of the hour is to strengthen the independence of the board. We have to put in place stringent standards for the independence of directors. The board should adopt global standards for director-independence, and should disclose how each independent director meets these standards. It is desirable to have a comprehensive report showing the names of the company employees of fellow board members who are related to each director on the board. This report should accompany the annual report of all listed companies. Another important step is to regularly assess the board members for performance. The assessment should focus on issues like competence, preparation, participation and contribution. Ideally, this evaluation should be performed by a third party. Underperforming directors should be allowed to leave at the end of their term in a gentle manner so that they do not lose face. Rather than being the rubber stamp of a company’s management policies, the board should become a true active partner of the management. For this, independent directors should be trained in their in their in roles and responsibilities. Independent directors should be trained on the business model and risk model of the company, on the governance practices, and the responsibilities of various committees of the board of the company. The board members should interact frequently with executives to understand operational issues. As part of the board meeting agenda, the independent directors should have a meeting among themselves without the management being present. The independent board members should periodically review the performance of the company’s CEO, the internal directors and the senior management. This has to be based on clearly defined objective criteria, and these criteria should be known to the CEO and other executive directors well before the start of the evolution period. Moreover, there should be a clearly laid down procedure for communicating the board’s review to the CEO and his/her team of executive directors. Managerial remuneration should be based on such reviews. Additionally, senior management compensation should be determined by the board in a manner that is fair to all stakeholders. We have to look at three important criteria in deciding managerial remuneration-fairness accountability and transparency. Fairness of compensation is determined by how employees and investors react to the compensation of the CEO. Accountability is enhanced by splitting the total compensation into a small fixed component and a large variable component. In other words, the CEO, other executive directors and the senior management should rise or fall with the fortunes of the company. The variable component should be linked to achieving the long-term objectives of the firm. Senior management compensation should be reviewed by the compensation committee of the board consisting of only the independent directors. This should be approved by the shareholders. It is important that no member of the internal management has a say in the compensation of the CEO, the internal board members or the senior management. The SEBI regulations and the CII code of conduct have been very helpful in enhancing the level of accountability of independent directors. The independent directors should decide voluntarily how they want to contribute to the company. Their performance should decide voluntarily how they want to contribute to the company. Their performance should be appraised through a peer evaluation process. Ideally, the compensation committee should decide on the compensation of each independent director based on such a performance appraisal. Auditing is another major area that needs reforms for effective corporate governance. An audit is the Independent examination of financial transactions of any entity to provide assurance to shareholder and other stakeholders that the financial statements are free of material misstatement. Auditors are qualified professionals appointed by the shareholders to report on the reliability of financial statements prepared by the management. Financial markets look to the auditor’s report for an independent opinion on the financial and risk situation of a company. We have to separate such auditing form other services. For a truly independent opinion, the auditing firm should not provide services that are perceived to be materially in conflict with the role of the auditor. These include investigations, consulting advice, sub contraction of operational activities normally undertaken by the management, due diligence on potential acquisitions or investments, advice on deal structuring, designing/implementing IT systems, bookkeeping, valuations and executive recruitment. Any departure from this practice should be approved by the audit committee in advance. Further, information on any such exceptions must be disclosed in the company’s quarterly and annual reports. To ensure the integrity of the audit team, it is desirable to rotate auditor partners. The lead audit partner and the audit partner responsible for reviewing a company’s audit must be rotated at least once every three to five years. This eliminates the possibility of the lead auditor and the company management getting into the kind of close, cozy relationship that results in lower objectivity in audit opinions. Further, a registered auditor should not audit a chief accounting office was associated with the auditing firm. It is best that members of the audit teams are prohibited from taking up employment in the audited corporations for at least a year after they have stopped being members of the audit team.A competent audit committee is essential to effectively oversee the financial accounting and reporting process. Hence, each member of the audit committee must be ‘financially literate’, further, at least one member of the audit committee, preferably the chairman, should be a financial expert-a person who has an understanding of financial statements and accounting rules, and has experience in auditing. The audit committee should establish procedures for the treatment of complaints received through anonymous submission by employees and whistleblowers. These complaints may be regarding questionable accounting or auditing issues, any harassment to an employee or any unethical practice in the company. The whistleblowers must be protected. Any related-party transaction should require prior approval by the audit committee, the full board and the shareholders if it is material. Related parties are those that are able to control or exercise significant influence. These include; parent- subsidiary relationships; entities under common control; individuals who, through ownership, have significant influence over the enterprise and close members of their families; and dey management personnel.Accounting standards provide a framework for preparation and presentation of financial statements and assist auditors in forming an opinion on the financial statements. However, today, accounting standards are issued by bodies comprising primarily of accountants. Therefore, accounting standards do not always keep pace with changes in the business environment. Hence, the accounting standards-setting body should include members drawn from the industry, the profession and regulatory bodies. This body should be independently funded. Currently, an independent oversight of the accounting profession does not exist. Hence, an independent body should be constituted to oversee the functioning of auditors for Independence, the quality of audit and professional competence. This body should comprise a "majority of non- practicing accountants to ensure independent oversight. To avoid any bias, the chairman of this body should not have practiced as an accountant during the preceding five years. Auditors of all public companies must register with this body. It should enforce compliance with the laws by auditors and should mandate that auditors must maintain audit working papers for at least seven years.To ensure the materiality of information, the CEO and CFO of the company should certify annual and quarterly reports. They should certify that the information in the reports fairly presents the financial condition and results of operations of the company, and that all material facts have been disclosed. Further, CEOs and CFOs should certify that they have established internal controls to ensure that all information relating to the operations of the company is freely available to the auditors and the audit committee. They should also certify that they have evaluated the effectiveness of these controls within ninety days prior to the report. False certifications by the CEO and CFO should be subject to significant criminal penalties (fines and imprisonment, if willful and knowing). If a company is required to restate its reports due to material non-compliance with the laws, the CEO and CFO must face severe punishment including loss of job and forfeiting bonuses or equity-based compensation received during the twelve months following the filing.The problem with the independent directors has been that: I. Their selection has been based upon their compatibility with the company management II. There has been lack of proper training and development to improve their skill set III. Their independent views have often come in conflict with the views of company management. This has hindered the company’s decision-making process IV. Stringent standards for independent directors have been lacking....

MCQ-> Read the following case-let and answer the questions that follow Rajinder Singh was 32 years old from the small town of Bhathinda, Punjab. Most of the families living there had middle class incomes, with about 10% of the population living below the poverty level. The population consisted of 10 percent small traders, 30 percent farmers, besides others. Rajinder liked growing up in Bhathinda, where people knew and cared about each other. Even as a youngster it was clear that Rajinder was smart and ambitious. Neighbors would often say, “Someday you’re going to make us proud!” He always had a job growing up at Singh’s General Store - Uncle Balwant’s store. Balwant was a well-intentioned person. Rajinder loved being at the store and not just because Balwant paid him well. He liked helping customers, most of who were known by the nicknames. Setting up displays and changing the merchandise for different seasons and holidays was always exciting. Uncle Balwant had one child and off late, his interest in business had declined. But he had taught Rajinder ‘the ins and outs of retailing’. He had taught Rajinder everything, including ordering merchandise, putting on a sale, customer relations, and keeping the books. The best part about working at the store was Balwant himself. Balwant loved the store as much as Rajinder did. Balwant had set up the store with a mission to make sure his neighbors got everything they needed at a fair price. He carried a wide variety of goods, based on the needs of the community. If you needed a snow shovel or piece of jewelry for your wife, it was no problem - Singh’s had it all. Rajinder was impressed by Balwant’s way of handling and caring for customers. If somebody was going through “hard times”, Balwant somehow knew it. When they came into the store, Balwant would make them feel comfortable, and say something like, “you know Jaswant, let’s put everything on credit today”. This kind of generosity made it easy to understand why Balwant was loved and respected throughout the community. Rajinder grew up and went to school and college in Bhathinda. Later on, he made it to an MBA program in Delhi. Rajinder did well in the MBA course and was goal oriented. After first year of his MBA, the career advisor and Balwant advised Rajinder for an internship at Bigmart. That summer, Rajinder was amazed by the breadth and comprehensiveness of the internship experience. Rajinder got inspired by the life story of the founder of Bigmart, and the value the founder held. Bigmart was one of the best companies in the world. The people that Rajinder worked for at Bigmart during the internship noticed Rajinder’s work ethic, knowledge, and enthusiasm for the business. Before the summer ended, Rajinder had been offered a job as a Management Trainee by Bigmart, to start upon graduation. Balwant was happy to see Rajinder succeed. Even for Rajinder, this was a dream job - holding the opportunity to move up the ranks in a big company. Rajinder did indeed move up the ranks quickly, from management trainee, to assistant store manager, to supervising manager of three stores, to the present position - Real Estate Manager, North India. This job involved locating new sites within targeted locations and community relations. One day Rajinder was eagerly looking forward to the next assignment. When he received email for the same, his world came crashing down. He was asked to identify next site in Bhathinda. It was not that Rajinder didn’t believe in Bigmart’s explanation. What was printed in the popular press,especially the business press, only reinforced Rajinder’s belief in Bigmart. An executive viewed as one of the wisest business persons in the world was quoted as saying, “Bigmart had been a major force in improving the quality of life for the average consumer around the world offering great prices on good, giving them one stop solution for almost everything.” Many big farmers also benefitted through low prices, as middlemen were removed. At the same time, Rajinder knew that opening a new Bigmart could disrupt small business in Bhathinda. Some local stores in small towns went out of business within a year of the Bigmart’s opening. In Bhathinda, one of the local stores Singh’s,now run by Balwant’s son, although Balwant still came in every day to “straighten out the merchandise.” As Rajinder thought about this assignment, depression set in, and the nightmares followed. Rajinder was frozen in time and space. Rajinder’s nightmares involved Balwant screaming something- although Rajinder could not make out what Balwant was saying. This especially troubled Rajinder, since Balwant never raised his voice. Rajinder didn’t know what to do - who might be helpful? Rajinder’s spouse, who was a housewife? Maybe talking it through could lead to some positive course of action. Rajinder’s boss?Would Bigmart understand? Could Rajinder really disclose the conflict without fear? Uncle Balwant? Should Rajinder really disclose the situation and ask for advise? He wanted a solution that would make all satkeholders happy.Who is the best person for Rajinder to talk to?

....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Estimated material usage cost per square feet of output.....

Estimated material usage cost per square feet of output.....