1.

Answer the questions based on the following information.

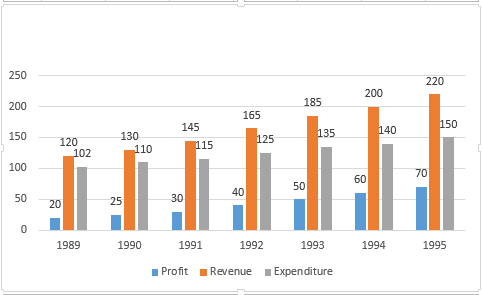

In which year was the growth in expenditure maximum as compared to the previous year?

In which year was the growth in expenditure maximum as compared to the previous year?

Write Comment

Comments

- By: anil on 05 May 2019 02.33 am

Show Similar Question And Answers

in year 1991 = near to 4

in year 1992 = above 8

in year 1993 = 8%

in year 1994 = lower than 4

in year 1995 = above 7 but lower than 8

Hence highest percentage increase is in year 1992