Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in -current-affairs-2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. Improve the bracketed part of the sentence. The driver gave (advice) at the court during the murder trial.

(A): evidence

(B): proof

(C): witness

(D): no improvement

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

SSC CHSL 25 Jan 2017 Afternoon Shift

Show Similar Question And Answers

QA->Pakistani microbiologist who was serving a life sentence in an Ajmer jail in connection with a 1992 murder case has been released recently after he was granted bail by the Supreme Court of India on humanitarian grounds. Name that microbiologist?....

QA->The person who prosecutors alleged worked as a Nazi guard at the Sobibor death camp, accused of helping to murder nearly 28,000 Jews at this camp, went on trial in country court in Munich, southern Germany on November 30, 2009?....

QA->For the first time, the Supreme Court issued contempt notice to a sitting high court judge, for levelling allegations against former judges of the Supreme Court and sitting judges of Madras High Court. Who is that sitting high court judge?....

QA->Prosecutors in the genocide trial of a former Khmer Rouge prison chief demanded a 40-year jail sentence recently for a man they described as responsible for snuffing out innocent lives and spreading terror across Cambodia. Name of that Jail Chief?....

QA->The former French president who has been found guilty of corruption and sentenced to a two year suspended prison sentence after a long-running criminal trial which concluded on 15 December 2011?....

MCQ->Improve the bracketed part of the sentence. The driver gave (advice) at the court during the murder trial.....

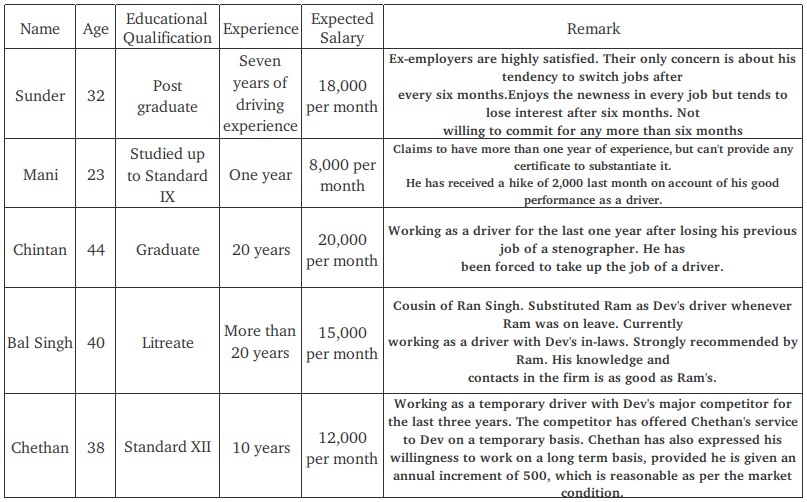

MCQ-> on the basis of the information given in the following case.Dev Anand, CEO of a construction company, recently escaped a potentially fatal accident. Dev had failed to notice a red light while driving his car and attending to his phone calls. His well-wishers advised him to get a suitable replacement for the previous driver Ram Singh, who had resigned three months back. Ram Singh was not just a driver, but also a trusted lieutenant for Dev Anand for the last five years. Ram used to interact with other drivers and gathered critical information that helped Dev in successfully bidding for different contracts. His inputs also helped Dev to identify some dishonest employees, and to retain crucial employees who were considering attractive offers from his competitors. Some of the senior employees did not like the informal influence of Ram and made it difficult for him to continue in the firm. Dev provided him an alternative job with one of his relatives. During the last three months Dev has considered different candidates for the post. The backgrounds of the candidates are given in the table below.

Dev is primarily looking for a stable and trustworthy driver, who can be a suitable replacement for Ram. His family members do not want Dev to appoint a young driver, as most of them are inexperienced. Dev’s driver is an employee of the firm and hence the appointment has to be routed through the HR manager of the firm. The HR manager prefers to maintain parity among all employees of the firm. He also needs to ensure that the selection of a new driver does not lead to discontent among the senior employees of the firm. From his perspective, and taking into account the family’s concerns, Mr. Dev would like to have

....

MCQ->In this section,each passage consists of 6 sentences.The first and sixth sentences are given in the beginning as S1 and S6.The middle four sentences in each are removed and jumbled up.These are labelled P,Q,R,S.You are required to find out the proper order of the sentences and mark accordingly on the answer sheet S1:At the roadside a driver will be asked to blow through a small glass tube into a plastic bag S6:The driver will be asked to go to the police station P:And if the color change did not reach the line the driver cannot be punished under the new law. Q:Inside the tube are chemically treated crystals which change color if the driver has alcohol on his brreath R:But if the color change did reach the line,then the test has proved positive S:If the color change goes beyond a certainline marked on the tube then this indicates the driver is probably over the specified limit The proper sequence should be....

MCQ-> Read carefully the four passages that follow and answer the questions given at the end of each passage:PASSAGE I The most important task is revitalizing the institution of independent directors. The independent directors of a company should be faithful fiduciaries protecting, the long-term interests of shareholders while ensuring fairness to employees, investor, customer, regulators, the government of the land and society. Unfortunately, very often, directors are chosen based of friendship and, sadly, pliability. Today, unfortunately, in the majority of cases, independence is only true on paper.The need of the hour is to strengthen the independence of the board. We have to put in place stringent standards for the independence of directors. The board should adopt global standards for director-independence, and should disclose how each independent director meets these standards. It is desirable to have a comprehensive report showing the names of the company employees of fellow board members who are related to each director on the board. This report should accompany the annual report of all listed companies. Another important step is to regularly assess the board members for performance. The assessment should focus on issues like competence, preparation, participation and contribution. Ideally, this evaluation should be performed by a third party. Underperforming directors should be allowed to leave at the end of their term in a gentle manner so that they do not lose face. Rather than being the rubber stamp of a company’s management policies, the board should become a true active partner of the management. For this, independent directors should be trained in their in their in roles and responsibilities. Independent directors should be trained on the business model and risk model of the company, on the governance practices, and the responsibilities of various committees of the board of the company. The board members should interact frequently with executives to understand operational issues. As part of the board meeting agenda, the independent directors should have a meeting among themselves without the management being present. The independent board members should periodically review the performance of the company’s CEO, the internal directors and the senior management. This has to be based on clearly defined objective criteria, and these criteria should be known to the CEO and other executive directors well before the start of the evolution period. Moreover, there should be a clearly laid down procedure for communicating the board’s review to the CEO and his/her team of executive directors. Managerial remuneration should be based on such reviews. Additionally, senior management compensation should be determined by the board in a manner that is fair to all stakeholders. We have to look at three important criteria in deciding managerial remuneration-fairness accountability and transparency. Fairness of compensation is determined by how employees and investors react to the compensation of the CEO. Accountability is enhanced by splitting the total compensation into a small fixed component and a large variable component. In other words, the CEO, other executive directors and the senior management should rise or fall with the fortunes of the company. The variable component should be linked to achieving the long-term objectives of the firm. Senior management compensation should be reviewed by the compensation committee of the board consisting of only the independent directors. This should be approved by the shareholders. It is important that no member of the internal management has a say in the compensation of the CEO, the internal board members or the senior management. The SEBI regulations and the CII code of conduct have been very helpful in enhancing the level of accountability of independent directors. The independent directors should decide voluntarily how they want to contribute to the company. Their performance should decide voluntarily how they want to contribute to the company. Their performance should be appraised through a peer evaluation process. Ideally, the compensation committee should decide on the compensation of each independent director based on such a performance appraisal. Auditing is another major area that needs reforms for effective corporate governance. An audit is the Independent examination of financial transactions of any entity to provide assurance to shareholder and other stakeholders that the financial statements are free of material misstatement. Auditors are qualified professionals appointed by the shareholders to report on the reliability of financial statements prepared by the management. Financial markets look to the auditor’s report for an independent opinion on the financial and risk situation of a company. We have to separate such auditing form other services. For a truly independent opinion, the auditing firm should not provide services that are perceived to be materially in conflict with the role of the auditor. These include investigations, consulting advice, sub contraction of operational activities normally undertaken by the management, due diligence on potential acquisitions or investments, advice on deal structuring, designing/implementing IT systems, bookkeeping, valuations and executive recruitment. Any departure from this practice should be approved by the audit committee in advance. Further, information on any such exceptions must be disclosed in the company’s quarterly and annual reports. To ensure the integrity of the audit team, it is desirable to rotate auditor partners. The lead audit partner and the audit partner responsible for reviewing a company’s audit must be rotated at least once every three to five years. This eliminates the possibility of the lead auditor and the company management getting into the kind of close, cozy relationship that results in lower objectivity in audit opinions. Further, a registered auditor should not audit a chief accounting office was associated with the auditing firm. It is best that members of the audit teams are prohibited from taking up employment in the audited corporations for at least a year after they have stopped being members of the audit team.A competent audit committee is essential to effectively oversee the financial accounting and reporting process. Hence, each member of the audit committee must be ‘financially literate’, further, at least one member of the audit committee, preferably the chairman, should be a financial expert-a person who has an understanding of financial statements and accounting rules, and has experience in auditing. The audit committee should establish procedures for the treatment of complaints received through anonymous submission by employees and whistleblowers. These complaints may be regarding questionable accounting or auditing issues, any harassment to an employee or any unethical practice in the company. The whistleblowers must be protected. Any related-party transaction should require prior approval by the audit committee, the full board and the shareholders if it is material. Related parties are those that are able to control or exercise significant influence. These include; parent- subsidiary relationships; entities under common control; individuals who, through ownership, have significant influence over the enterprise and close members of their families; and dey management personnel.Accounting standards provide a framework for preparation and presentation of financial statements and assist auditors in forming an opinion on the financial statements. However, today, accounting standards are issued by bodies comprising primarily of accountants. Therefore, accounting standards do not always keep pace with changes in the business environment. Hence, the accounting standards-setting body should include members drawn from the industry, the profession and regulatory bodies. This body should be independently funded. Currently, an independent oversight of the accounting profession does not exist. Hence, an independent body should be constituted to oversee the functioning of auditors for Independence, the quality of audit and professional competence. This body should comprise a "majority of non- practicing accountants to ensure independent oversight. To avoid any bias, the chairman of this body should not have practiced as an accountant during the preceding five years. Auditors of all public companies must register with this body. It should enforce compliance with the laws by auditors and should mandate that auditors must maintain audit working papers for at least seven years.To ensure the materiality of information, the CEO and CFO of the company should certify annual and quarterly reports. They should certify that the information in the reports fairly presents the financial condition and results of operations of the company, and that all material facts have been disclosed. Further, CEOs and CFOs should certify that they have established internal controls to ensure that all information relating to the operations of the company is freely available to the auditors and the audit committee. They should also certify that they have evaluated the effectiveness of these controls within ninety days prior to the report. False certifications by the CEO and CFO should be subject to significant criminal penalties (fines and imprisonment, if willful and knowing). If a company is required to restate its reports due to material non-compliance with the laws, the CEO and CFO must face severe punishment including loss of job and forfeiting bonuses or equity-based compensation received during the twelve months following the filing.The problem with the independent directors has been that: I. Their selection has been based upon their compatibility with the company management II. There has been lack of proper training and development to improve their skill set III. Their independent views have often come in conflict with the views of company management. This has hindered the company’s decision-making process IV. Stringent standards for independent directors have been lacking....

MCQ-> In the following question, out of the four alternatives, select the alternative which will improve the bracketed part of the sentence. In case no improvement is needed, select "no improvement".In the following question, out of the four alternatives, select the alternative which will improve the bracketed part of the sentence. In case no improvement is needed, select "no improvement". (Higher provision) requirements on these counts as well as other factors will affect the capital position of several banks.....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Dev is primarily looking for a stable and trustworthy driver, who can be a suitable replacement for Ram. His family members do not want Dev to appoint a young driver, as most of them are inexperienced. Dev’s driver is an employee of the firm and hence the appointment has to be routed through the HR manager of the firm. The HR manager prefers to maintain parity among all employees of the firm. He also needs to ensure that the selection of a new driver does not lead to discontent among the senior employees of the firm.

From his perspective, and taking into account the family’s concerns, Mr. Dev would like to have

Dev is primarily looking for a stable and trustworthy driver, who can be a suitable replacement for Ram. His family members do not want Dev to appoint a young driver, as most of them are inexperienced. Dev’s driver is an employee of the firm and hence the appointment has to be routed through the HR manager of the firm. The HR manager prefers to maintain parity among all employees of the firm. He also needs to ensure that the selection of a new driver does not lead to discontent among the senior employees of the firm.

From his perspective, and taking into account the family’s concerns, Mr. Dev would like to have