1. A shopkeeper allows a discount of 12.5 % on the marked price of a certain article and makes a profit of 20 %. If the article costs the shopkeeper 210, then the marked price of the article will be

Write Comment

Comments

- By: anil on 05 May 2019 01.53 amC.P. = 210 Profit = $$frac{20}{100}$$ * 210 = 42 => S.P. = 210+42 = 252 Let M.P. = $$x$$ Discount % = 12.5% => $$frac{x-252}{x}$$ * 100 = 12.5 => $$7x$$ = 2016 => $$x$$ = 2016/7 = 288

Show Similar Question And Answers

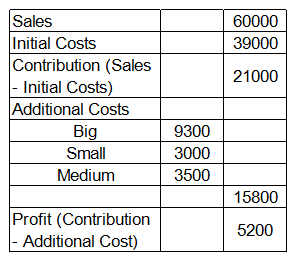

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below:

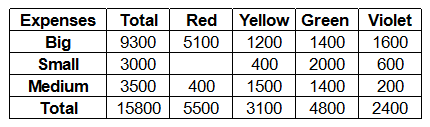

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below: Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below:

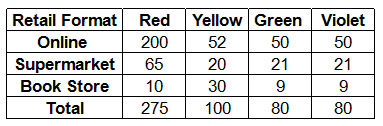

Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below: Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....

Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....