Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. The ability of the firm to meet its current liability is measured by:

(A): Selvency ratio

(B): Liquidity ratio

(C): Activity ratio

(D): Profitability ratio

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

kerala-psc

PHARMACIST-GR-II---IMSMEDICAL-EDUCATIONHEALTH-SERVICESCOMPOUNDER---PLANTATION-CORPORATION

166/2016

Show Similar Question And Answers

QA->Limited Liability means that the liability of the members are:....

QA->Economic development that meets the needs of the present without compromising the ability of future generations to meet their own needs is ?....

QA->Economic development that meets the needs of the present without compromising the ability of future generations to meet their own needs is :....

QA->Which country n launched its fifth spy satellite on 28th November 2009 in a bid to boost its ability to independently gather intelligence?....

QA->The flow of electric current is measured in ?....

MCQ->The ability of the firm to meet its current liability is measured by:....

MCQ-> Read the passage given below and answer the following questionsFirms are said to be in perfect competition when the following conditions occur: (1) many firms produce identical products; (2) many buyers are available to buy the product, and many sellers are available to sell the product; (3) sellers and buyers have all relevant information to make rational decisions about the product being bought and sold; and (4) firms can enter and leave the market without any restrictions—in other words, there is free entry and exit into and out of the market.A perfectly competitive firm is known as a price taker, because the pressure of competing firms forces them to accept the

prevailing

equilibrium price in the market. If a firm in a perfectly competitive market raises the price of its product by so much as a penny, it will lose all of its sales to competitors. When a wheat grower, wants to know what the going price of wheat is, he or she has to go to the computer or listen to the radio to check. The market price is determined solely by supply and demand in the entire market and not the individual farmer. Also, a perfectly competitive firm must be a very small player in the overall market, so that it can increase or decrease output without noticeably affecting the overall quantity supplied and price in the market.A perfectly competitive market is a

hypothetical

extreme; however, producers in a number of industries do face many competitor firms selling highly similar goods, in which case they must often act as price takers. Agricultural markets are often used as an example. The same crops grown by different farmers are largely interchangeable. According to the United States Department of Agriculture monthly reports, in 2015, U.S. corn farmers received an average price of $6.00 per bushel and wheat farmers received an average price of $6.00 per bushel. A corn farmer who attempted to sell at $7.00 per bushel, or a wheat grower who attempted to sell for $8.00 per bushel, would not have found any buyers. A perfectly competitive firm will not sell below the equilibrium price either. Why should they when they can sell all they want at the higher price?Source: Principles of Economics, Download for free at http://cnx.org/content/col11613/latest.According to the passage, why is a perfectly competitive firm a price taker?

....

MCQ-> Read the following passage based on an Interview to answer the given questions based on it. Certain words are printed in bold to help you locate them while answering some of the questions.A spate of farmer suicides linked to harassment by recovery agents employed by micro finance institutions (MFLs) in Andhra Pradesh

spurned

the state government to bring in regulation to protect consumer interests. But, while the Bill has brought into sharp focus the need for consumer protection, it tries to micro-manage MFI operations and in the process it could

scuttle

some of the crucial bene ts that MFIs bring to farmers, says the author of Micro nance India, State Of The Sec-for Report 2010. In an interview he points out that prudent regulation can ensure the original goal of the MFIs - social uplift of the poor.

Do you feel the AP Bill to regulate Mils is well thought out? Does it ensure fairness to the borrowers and the long-term health of the sector?

The AP Bill has brought into sharp focus the need for customer protection in four critical areas. First is pricing. Second is lender's liability whether the lender can give too much loan without assessing the customer's ability to pay. Third is the structure of loan repayment - whether you can ask money on a weekly basis from people who don't produce weekly incomes. Fourth is the practices that attend to how you deal with defaults. But the Act should have looked at the positive bene ts that institutions could bring in, and where they need to be regulated in the interests of the customers. It should have brought only those features in. Say, you want the recovery practices to be consistent with what the customers can really

manage

. If the customer is aggrieved and complains that somebody is harassing him, then those complaints should be investigated by the District Rural Development Authority. Instead what the Bill says is that MF1s cannot go to the customer's premises to ask for recovery and that all transactions will be done in the Panchayat of ce. With great dif culty, MFIs brought services to the door of people. It is such a relief for the customers not to be spending time out going to banks or Panchayat of ces, which could be 10 km away in some cases. A facility which has brought some relief to people is being shut. Moreover, you are practically telling the MFI where it should do business and how it should do it.

Social responsibilities were inbuilt when the MIrls were rst conceived. If kills go for profit with loose regulations, how are they different from moneylenders?

Even among moneylenders there are very good people who take care of the customer's circumstance, and there are really bad ones. A large number of the MF1s are good and there are some who are coercive because of the kind of prices and processes they have adopted. But Moneylenders never got this organised. They did not have such a large footprint. An MFI brought in organisation, it mobilized the equity, it brought in commercial funding. It invested in systems. It appointed a large number of people. But some of them

exacted

a much higher price than they should have. They wanted to break even very fast and greed did take over in some cases.

Are the for-profit 'Ms the only ones harassing people for recoveries?

Some not-for-profit out ts have also adopted the same kind of recovery methods. That may be because you have to show that you are very ef cient in your recovery methods and that your portfolio is of a very high quality if you want to get commercial funding from a bank. In fact, among for-profits there are many who have sensible recovery practices. Some have fortnightly recovery, some have monthly recovery. So we have differing practices. We just describe a few dominant ones and assume every for-profit MFI operates like that. How can you introduce regulations to ensure social upliftment in a sector that is moving towards for-profit models? I am not really concerned whether someone wants to make a profit or not The bottom-line for me is customer protection. The rst area is fair practices. Are you telling your customers how the loan is structured ? Are you being transparent about your performance? There should also be a lender's liability attached to what you do. Suppose you lend excessively to a customer without assessing their ability to service the loan, you have to take the hit. Then there's the question of limiting returns. You can say that an MFI cannot have a return on assets more than X, a return on equity of more than Y. Then suppose there is a privately promoted MFI, there should be a regulation to ensure the MFI cannot access equity markets till a certain amount of time. MFIs went to markets perhaps because of the need to grow too big too fast. The government thought they were making profit off the poor, and that's an indirect reason why they decided to clamp down on MF1s. If you say an MFI won't go to capital market, then it will keep political compulsions under rein.Which of the following best explains "structure of loan repayment" in this context of the rst question asked to the author ?....

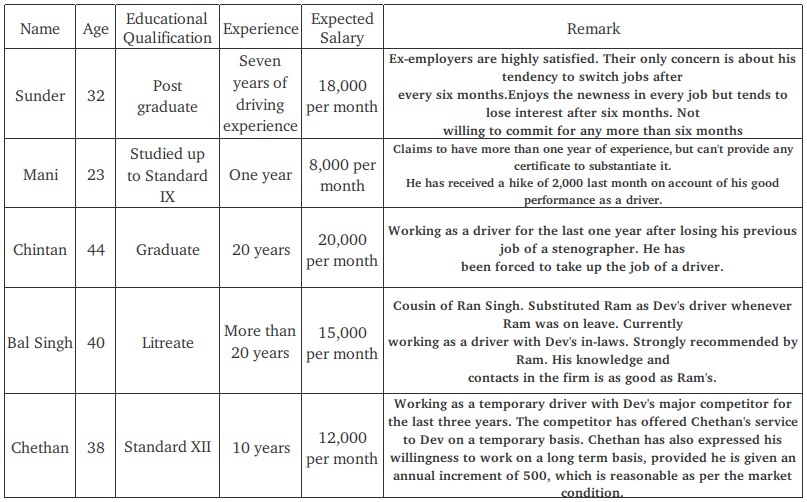

MCQ-> on the basis of the information given in the following case.Dev Anand, CEO of a construction company, recently escaped a potentially fatal accident. Dev had failed to notice a red light while driving his car and attending to his phone calls. His well-wishers advised him to get a suitable replacement for the previous driver Ram Singh, who had resigned three months back. Ram Singh was not just a driver, but also a trusted lieutenant for Dev Anand for the last five years. Ram used to interact with other drivers and gathered critical information that helped Dev in successfully bidding for different contracts. His inputs also helped Dev to identify some dishonest employees, and to retain crucial employees who were considering attractive offers from his competitors. Some of the senior employees did not like the informal influence of Ram and made it difficult for him to continue in the firm. Dev provided him an alternative job with one of his relatives. During the last three months Dev has considered different candidates for the post. The backgrounds of the candidates are given in the table below.

Dev is primarily looking for a stable and trustworthy driver, who can be a suitable replacement for Ram. His family members do not want Dev to appoint a young driver, as most of them are inexperienced. Dev’s driver is an employee of the firm and hence the appointment has to be routed through the HR manager of the firm. The HR manager prefers to maintain parity among all employees of the firm. He also needs to ensure that the selection of a new driver does not lead to discontent among the senior employees of the firm. From his perspective, and taking into account the family’s concerns, Mr. Dev would like to have

....

MCQ-> Read the following instructions and answer the questions. After the discussion at a high level meeting of government officers, the criteria for issuing of import / export licence to eligible business firms for the year 2011-12 were finalized as follows. The firms must – I. Have a Grade – ‘A’ certified unit for any products. II. Not have any legal dispute case against it. III. Possess minimum asset worth Rs. 40 lakhs. IV. Submit an environment clearance certificate issued by the Pollution Control Board (PCB) of the state where the firm is located. V. Deposit the margin money of Rs. 1 lakh. VI. Arrange for three guarantors with their personal identity cards (IDs). However, if the firm satisfies all the above mentioned criteria except: a) Criteria (I), but is a traditional handloom production unit, then the case may be referred to Development Commissioner, Handloom (DCH) of the state. b) Criteria (IV), but is a local employment provider / thread (input) supplier / cloth supplier, the case may be referred to the Director, Department of Industry of the state. c) Criteria (V) but can deposit at least Rs. 50000, the firm will be given import licence only and the case may be referred to the Deputy Director, Department of Industry of the state. Based on the above criteria and information provided on each of the firms in the questions below, you have to decide which course of action should be taken against each firm. Without assuming anything regarding any applicant firm, the decision should be based on the information provided.Mahalaxmi Weaving Center is a traditional handloom production unit. It has property worth more than Rs. 1 crore. It managed to get three guarantors with their personal IDs. No legal case is there against it. There is no problem submitting an environmental clearance, as the same is already issued to it by the State Pollution Control Board. It is also ready to deposit Rs. 1 lakh.

....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Dev is primarily looking for a stable and trustworthy driver, who can be a suitable replacement for Ram. His family members do not want Dev to appoint a young driver, as most of them are inexperienced. Dev’s driver is an employee of the firm and hence the appointment has to be routed through the HR manager of the firm. The HR manager prefers to maintain parity among all employees of the firm. He also needs to ensure that the selection of a new driver does not lead to discontent among the senior employees of the firm.

From his perspective, and taking into account the family’s concerns, Mr. Dev would like to have

Dev is primarily looking for a stable and trustworthy driver, who can be a suitable replacement for Ram. His family members do not want Dev to appoint a young driver, as most of them are inexperienced. Dev’s driver is an employee of the firm and hence the appointment has to be routed through the HR manager of the firm. The HR manager prefers to maintain parity among all employees of the firm. He also needs to ensure that the selection of a new driver does not lead to discontent among the senior employees of the firm.

From his perspective, and taking into account the family’s concerns, Mr. Dev would like to have