Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. toeveryones expectations he sanctioned an additional plant in

(A): any

(B): mean

(C): short

(D): no

(E): less

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->Who is the author of “Great Expectations”?....

QA->Who is the author of Great Expectations?....

QA->The World Bank has sanctioned 250 million dollar loan for which project, aiming at reinforcing flood control measures and reconstruction of flood affected infrastructure in Jammu and Kashmir?....

QA->The maximum period of leave that may be sanctioned to an officer for taking up employment abroad or within India is limited to:....

QA->The strength of a service or part of a service sanctioned as a separate unit is called:....

MCQ-> Analyse the following passage and provide appropriate answers for the through that follow. "Whatever actions are done by an individual in different embodiments, Is] he reaps the fruit of those actions in those very bodies or embodiments (in future existences)". A belief in karma entails, among other things, a focus on long run consequences, i.e., a long term orientation. Such an orientation implies that people who believe in karma may be more honest with themselves in general and in setting expectations in particular--a hypothesis we examine here. This research is based on three simple premises. First, because lower expectations often lead to greater satisfaction, individuals in general, and especially those who are sensitive to the gap between performance and expectations, have the incentive to and actually do "strategically" lower their expectations. Second, individuals with a long term orientation are likely to be less inclined to lower expectations in the hope of temporarily feeling better. Third, long term orientation and the tendency to lower expectations are at least partially driven by cultural factors. In India, belief in karma, with its emphasis on a longer term orientation, will therefore to some extent counteract the tendency to lower expectations. The empirical results support our logic; those who believe more strongly in karma are less influenced by disconfirmation sensitivity and therefore have higher expectations. Consumers make choices based on expectations of how alternative options will perform (i.e., expected utility). Expectations about the quality of a product also play a central role in subsequent satisfaction. These expectations may be based on a number of factors including the quality of a typical brand in a category, advertised quality, and disconfirmation sensitivity. Recent evidence suggests that consumers, who are more disconfirmation sensitive (i.e., consumers who are more satisfied when products perform better than expected or more dissatisfied when products perform worse than expected) have lower expectations. However, there is little research concerning the role of culture-specific variables in expectation formation, particularly how they relate to the impact of disconfirmation sensitivity on consumer expectations."Future existences" in the first paragraph can refer to: 1. Human life, 5 years afterwards 2. Next birth in human form 3. Next birth in any embodiment Which of the following statement(s) is correct?....

MCQ-> In each question below is given a statement followed by two "Expectations" numbered I and II. An Expectation is something which can either be an objective or prospect or desired outcome or hope behind the action /statement. You have to consider the statement and the following Expectations and decide which of the Expectations is implicit in the statement. Give answer a:if only Expectation I is implicit. Give answer b: if only Expectation II is implicit. Give answer c: if either Expectation I or II Expectation II is implicit. Give answer d: if neither Expectation I nor Expectation II is implicit. Give answer e: if both Expectations I and II are implicit.Statement : A promotional campaign - For healthy children encourage them to play in the playgrounds rather than video games at home. Expectations : I. Health of atleast some children would improve following this campaign. II. Most of the parents would not buy video games for their children after this promotional campaign.....

MCQ->toeveryones expectations he sanctioned an additional plant in....

MCQ-> I suggest that the essential character of the Trade Cycle and, especially, the regularity of time-sequence and of duration which justifies us in calling it a cycle, is mainly due to the way in which the marginal efficiency of capital fluctuates. The Trade Cycle is best regarded, I think, as being occasioned by a cyclical change in the marginal efficiency of capital, though complicated and often aggravated by associated changes in the other significant short period variables of the economic system.By a cyclical movement we mean that as the system progresses in, e.g. the upward direction, the forces propelling it upwards at first gather force and have a cumulative effect on one another but gradually lose their strength until at a certain point they tend to be replaced by forces operating in the opposite direction; which in turn gather force for a time and accentuate one another, until they too, having reached their maximum development, wane and give place to their opposite. We do not, however, merely mean by a cyclical movement that upward and downward tendencies, once started, do not persist for ever in the same direction but are ultimately reversed. We mean also that there is some recognizable degree of regularity in the time-sequence and duration of the upward and downward movements. There is, however, another characteristic of what we call the Trade Cycle which our explanation must cover if it is to be adequate; namely, the phenomenon of the ‘crisis’ the fact that the substitution of a downward for an upward tendency often takes place suddenly and violently, whereas there is, as a rule, no such sharp turning-point when an upward is substituted for a downward tendency. Any fluctuation in investment not offset by a corresponding change in the propensity to consume will, of course, result in a fluctuation in employment. Since, therefore, the volume of investment is subject to highly complex influences, it is highly improbable that all fluctuations either in investment itself or in the marginal efficiency of capital will be of a cyclical character.We have seen above that the marginal efficiency of capital depends, not only on the existing abundance or scarcity of capital-goods and the current cost of production of capital- goods, but also on current expectations as to the future yield of capital-goods. In the case of durable assets it is, therefore, natural and reasonable that expectations of the future should play a dominant part in determining the scale on which new investment is deemed advisable. But, as we have seen, the basis for such expectations is very precarious. Being based on shifting and unreliable evidence, they are subject to sudden and violent changes. Now, we have been accustomed in explaining the ‘crisis’ to lay stress on the rising tendency of the rate of interest under the influence of the increased demand for money both for trade and speculative purposes. At times this factor may certainly play an aggravating and, occasionally perhaps, an initiating part. But I suggest that a more typical, and often the predominant, explanation of the crisis is, not primarily a rise in the rate of interest, but a sudden collapse in the marginal efficiency of capital. The later stages of the boom are characterized by optimistic expectations as to the future yield of capital goods sufficiently strong to offset their growing abundance and their rising costs of production and, probably, a rise in the rate of interest also. It is of the nature of organized investment markets, under the influence of purchasers largely ignorant of what they are buying and of speculators who are more concerned with forecasting the next shift of market sentiment than with a reasonable estimate of the future yield of capital-assets, that, when disillusion falls upon an over-optimistic and over- bought market, it should fall with sudden and even catastrophic force. Moreover, the dismay and uncertainty as to the future which accompanies a collapse in the marginal efficiency of capital naturally precipitates a sharp increase in liquidity-preference and hence a rise in the rate of interest. Thus the fact that a collapse in the marginal efficiency of capital tends to be associated with a rise in the rate of interest may seriously aggravate the decline in investment. But the essence of the situation is to be found, nevertheless, in the collapse in the marginal efficiency of capital, particularly in the case of those types of capital which have been contributing most to the previous phase of heavy new investment. Liquidity preference, except those manifestations of it which are associated with increasing trade and speculation, does not increase until after the collapse in the marginal efficiency of capital. It is this, indeed, which renders the slump so intractable. Which of the following does not describe the features of cyclical movement?

....

MCQ-> Read the following caselet and choose the best alternative

The BIG and Colourful Company

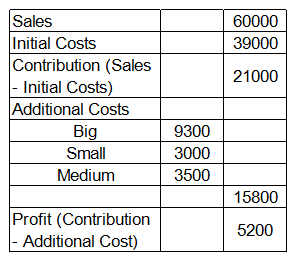

You are running "BIG and Colourful (BnC)" company that sells books to customers through three retail formats: a. You can buy books from bookstores, b. You can buy books from supermarket, c. You can order books over the Internet (Online). Your manager has an interesting way of classifying expenses: some of the expenses are classified in terms of size: Big, Small and Medium; and others are classified in terms of the colors, Red, Yellow, Green and Violet. The company has a history of categorizing overall costs into initial costs and additional costs. Additional costs are equal to the sum of Big, Small and Medium expenses. There are two types of margins, contribution (sales minus initial costs) and profit (contribution minus additional costs). Given below is the data about sales and costs of BnC:

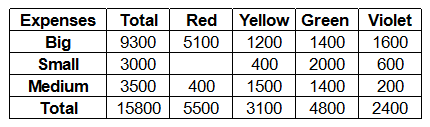

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below:

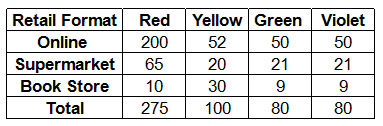

Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below:

Read the following statements: Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2. Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below:

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below: Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below:

Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below: Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....

Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....