Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in -current-affairs-2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. Statements : No price is a rate. All rates are expenses. Conclusions : I. No expense is a price. II All prices being expenses is a possibility.

(A): If neither conclusion I nor conclusion II follows

(B): If either conclusion I or conclusion II follows

(C): If only conclusion II follows

(D): If only conclusion I follows

(E): If both conclusion I and conclusion II follow

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->…………….means the annual financial statements and other statements prescribed under Rule 65 of Kerala Panchayat Raj (Accounts) Rules, 2011?....

QA->In which city has Congress opened a State Bank of Tomatoes, as a novel way of protesting about the abnormal price increase in tomato prices ?....

QA->The economic condition in which the rate at which the general level of prices for goods and services is rising and subsequently; purchasing power is falling is called?....

QA->Statements of affairs method is called or known as _____ method.....

QA->Consider a Program Graph (PG) with statements as nodes and control as edges. Which of the following is not true for any PG?....

MCQ->

Read the passage given below and answer the questions that follow:-

Brazil is a top exporter of every commodity that has seen dizzying price surges - iron ore, soybeans, sugar - producing a golden age for economic growth Foreign money-flows into Brazilian stocks and bonds climbed heavenward, up more than tenfold, from $5 billion a year in early 2007 to more than $50 billion in the twelve months through March 2011.The flood of foreign money buying up Brazilian assets has made the currency one of the most expensive in the world, and Brazil one of the most costly, overhyped economies. Almost every major emerging- market currency has strengthened against the dollar over the last decade, but the Brazilian Real is on a path alone, way above the pack, having doubled in value against the dollar.Economists have all kinds of fancy ways to measure the real value of a currency, but when a country is pricing itself this far out of the competition, you can feel it on the ground. In early 2011 the major Rio paper, 0 Globo, ran a story on prices showing that croissants are more expensive than they are in Paris, haircuts cost more than they do in London, bike rentals are more expensive than in Amsterdam, and movie tickets sell for higher prices than in Madrid. A rule of the road: if the local prices in an emerging market country feel expensive even to a visitor from a rich nation, that country is probably not a breakout nation.There is no better example of how absurd it is to lump all the big emerging markets together than the frequent pairing of Brazil and China. Those who make this comparison are referring only to the fact that they are the biggest players in their home regions, not to the way the economies actually run. Brazil is the world‘s leading exporter of many raw materials, and China is the leading importer; that makes them major trade partners - China surpassed the United States as Brazil's leading trade partner in 2009 f but it also makes them opposites in almost every important economic respect: Brazil is the un-China, with interest rates that are too high, and a currency that is too expensive. It spends too little on roads and too much on welfare, and as a result has a very un-China-like growth record.It may not be entirely fair to compare economic growth in Brazil with that of its Asian counterparts, because Brazil has a per capita income of $12,000, more than two times China's and nearly ten times India's. But even taking into account the fact that it is harder for rich nations to grow quickly, Brazil's growth has been disappointing. Since the early 19805 the Brazilian growth rate has oscillated around an average of 2.5 percent, spiking only in concert with increased prices for Brazil's key commodity exports. While China has been criticized for pursuing "growth at any cost," Brazil has sought to secure "stability at any cost." Brazil's caution stems from its history of financial crises, in which overspending produced debt, humiliating defaults, and embarrassing devaluations, culminating in a disaster that is still recent enough to be fresh in every Brazilian adult's memory: the hyperinflation that started in the early 19805 and peaked in 1994, at the vertiginous annual rate of 2,100 percent.Wages were pegged to inflation but were increased at varying intervals in different industries, 50 workers never really knew whether they were making good money or not. As soon as they were paid, they literally ran to the store with cash to buy food, and they could afford little else, causing non-essential industries to start to die. Hyperinflation finally came under control in l995, but it left a problem of regular behind. Brazil has battled inflation ever since by maintaining one of the highest interest rates in the emerging world. Those high rates have attracted a surge of foreign money, which is partly why the Brazilian Real is so expensive relative to comparable currencies.There is a growing recognition that China faces serious "imbalances" that could derail its long economic boom. Obsessed until recently with high growth, China has been pushing too hard to keep its currency too cheap (to help its export industries compete), encouraging excessively high savings and keeping interest rates rock bottom to fund heavy spending on roads and ports. China is only now beginning to consider a shift in spending priorities to create social programs that protect its people from the vicissitudes of old age and unemployment.Brazil’s economy is just as badly out of balance, though in opposite ways. While China has introduced reforms relentlessly for three decades, opening itself up to the world even at the risk of domestic instability, Brazil has pushed reforms only in the most dire circumstances, for example, privatizing state companies when the government budget is near collapse. Fearful of foreign shocks, Brazil is still one of the most closed economies in the emerging world - total imports and exports account for only 15 percent of GDP - despite its status as the world's leading exporter of sugar, orange juice, coffee, poultry, and beef.To pay for its big government, Brazil has jacked up taxes and now has a tax burden that equals 38 percent of GDP, the highest in the emerging world, and very similar to the tax burden in developed European welfare states, such as Norway and France. This heavy load of personal and corporate tax on a relatively poor country means that businesses don’t have the money to invest in new technology or training, which in turn means that industry is not getting more efficient. Between 1986 and 2008 Brazil’s productivity grew at an annual rate of :about 0.2 percent, compared to 4 percent in China. Over the same period, productivity grew in India at close to 3 percent and in South Korea and Thailand at close to 2 percent. According to the passage, the major concern facing the Brazil economy is:

....

MCQ->Statements : No price is a rate. All rates are expenses. Conclusions : I. No expense is a price. II All prices being expenses is a possibility.....

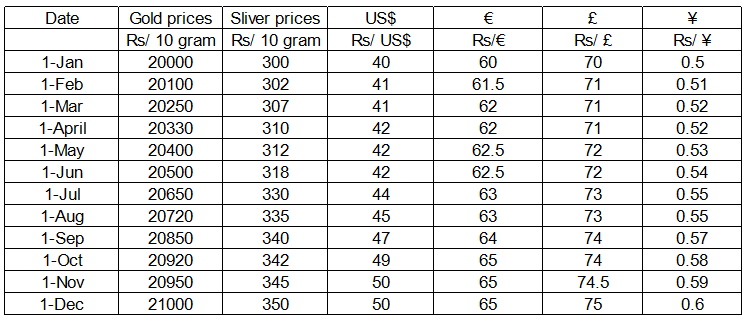

MCQ-> answer questions based on the following information:In the beginning of the year 2010, Mr. Sanyal had the option to invest Rs. 800000 in one or more of the following assets – gold, silver, US bonds, EU bonds, UK bonds and Japanese bonds. In order to invest in US bonds, one must first convert his investible fund into US Dollars at the ongoing exchange rate. Similarly, if one wants to invest in EU bonds or UK bonds or Japanese bonds one must first convert his investible fund into Euro, British Pounds and Japanese Yen respectively at the ongoing exchange rates. Transactions were allowed only in the beginning of every month. Bullion prices and exchange rates were fixed at the beginning of every month and remained unchanged throughout the month. Refer to the table titled “Bullion Prices and Exchange Rates in 2010" for the relevant data.

Bullion Prices and Exchange Rates in 2010

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

....

MCQ-> Crinoline and croquet are out. As yet, no political activists have thrown themselves in front of the royal horse on Derby Day. Even so, some historians can spot the parallels. It is a time of rapid technological change. It is a period when the dominance of the world’s superpower is coming under threat. It is an epoch when prosperity masks underlying economic strain. And, crucially, it is a time when policy-makers are confident that all is for the best in the best of all possible worlds. Welcome to the Edwardian Summer of the second age of globalisation. Spare a moment to take stock of what’s been happening in the past few months. Let’s start with the oil price, which has rocketed to more than $65 a barrel, more than double its level 18 months ago. The accepted wisdom is that we shouldn’t worry our little heads about that, because the incentives are there for business to build new production and refining capacity, which will effortlessly bring demand and supply back into balance and bring crude prices back to $25 a barrel. As Tommy Cooper used to say, ‘just like that’. Then there is the result of the French referendum on the European Constitution, seen as thick-headed luddites railing vainly against the modern world. What the French needed to realise, the argument went, was that there was no alternative to the reforms that would make the country more flexible, more competitive, more dynamic. Just the sort of reforms that allowed Gate Gourmet to sack hundreds of its staff at Heathrow after the sort of ultimatum that used to be handed out by Victorian mill owners. An alternative way of looking at the French “non” is that our neighbours translate “flexibility” as “you’re fired”. Finally, take a squint at the United States. Just like Britain a century ago, a period of unquestioned superiority is drawing to a close. China is still a long way from matching America’s wealth, but it is growing at a stupendous rate and economic strength brings geo-political clout. Already, there is evidence of a new scramble for Africa as Washington and Beijing compete for oil stocks. Moreover, beneath the surface of the US economy, all is not well. Growth looks healthy enough, but the competition from China and elsewhere has meant the world’s biggest economy now imports far more than it exports. The US is living beyond its means, but in this time of studied complacency a current account deficit worth 6 percent of gross domestic product is seen as a sign of strength, not weakness. In this new Edwardian summer, comfort is taken from the fact that dearer oil has not had the savage inflationary consequences of 1973-74, when a fourfold increase in the cost of crude brought an abrupt end to a postwar boom that had gone on uninterrupted for a quarter of a century. True, the cost of living has been affected by higher transport costs, but we are talking of inflation at b)3 per cent and not 27 per cent. Yet the idea that higher oil prices are of little consequence is fanciful. If people are paying more to fill up their cars it leaves them with less to spend on everything else, but there is a reluctance to consume less. In the 1970s unions were strong and able to negotiate large, compensatory pay deals that served to intensify inflationary pressure. In 2005, that avenue is pretty much closed off, but the abolition of all the controls on credit that existed in the 1970s means that households are invited to borrow more rather than consume less. The knock-on effects of higher oil prices are thus felt in different ways – through high levels of indebtedness, in inflated asset prices, and in balance of payments deficits.There are those who point out, rightly, that modern industrial capitalism has proved mightily resilient these past 250 years, and that a sign of the enduring strength of the system has been the way it apparently shrugged off everything – a stock market crash, 9/11, rising oil prices – that have been thrown at it in the half decade since the millennium. Even so, there are at least three reasons for concern. First, we have been here before. In terms of political economy, the first era of globalisation mirrored our own. There was a belief in unfettered capital flows, in free trade, and in the power of the market. It was a time of massive income inequality and unprecedented migration. Eventually, though, there was a backlash, manifested in a struggle between free traders and protectionists, and in rising labour militancy. Second, the world is traditionally at its most fragile at times when the global balance of power is in flux. By the end of the nineteenth century, Britain’s role as the hegemonic power was being challenged by the rise of the United States, Germany, and Japan while the Ottoman and Hapsburg empires were clearly in rapid decline. Looking ahead from 2005, it is clear that over the next two or three decades, both China and India – which together account for half the world’s population – will flex their muscles. Finally, there is the question of what rising oil prices tell us. The emergence of China and India means global demand for crude is likely to remain high at a time when experts say production is about to top out. If supply constraints start to bite, any declines in the price are likely to be short-term cyclical affairs punctuating a long upward trend.By the expression ‘Edwardian Summer’, the author refers to a period in which there is

....

MCQ-> Read the following passage and provide appropriate answers for the questionsThere is an essential and irreducible ‘duality’ in the normative conceptualization of an individual person. We can see the person in terms of his or her ‘agency’, recognizing and respecting his or her ability to form goals, commitments, values, etc., and we can also see the person in terms of his or her ‘well-being’. This dichotomy is lost in a model of exclusively self- interested motivation, in which a person’s agency must be entirely geared to his or her own well-being. But once that straitjacket of self-interested motivation is removed, it becomes possible to recognize the indisputable fact that the person’s agency can well be geared to considerations not covered - or at least not fully covered - by his or her own well-being. Agency may be seen as important (not just instrumentally for the pursuit of well-being, but also intrinsically), but that still leaves open the question as to how that agency is to be evaluated and appraised. Even though the use of one’s agency is a matter for oneself to judge, the need for careful assessment of aims, objective, allegiances, etc., and the conception of the good, may be important and exacting. To recognize the distinction between the ‘agency aspect’ and the ‘well-being aspect’ of a person does not require us to take the view that the person’s success as an agent must be independent, or completely separable from, his or her success in terms of well-being. A person may well feel happier and better off as a result of achieving what he or she wanted to achieve - perhaps for his or her family, or community, or class, or party, or some other cause. Also it is quite possible that a person’s well-being will go down as a result of frustration if there is some failure to achieve what he or she wanted to achieve as an agent, even though those achievements are not directly concerned with his or her well-being. There is really no sound basis for demanding that the agency aspect and the well-being aspect of a person should be independent of each other, and it is, I suppose, even possible that every change in one will affect the other as well. However, the point at issue is not the plausibility of their independence, but the sustainability and relevance of the distinction. The fact that two variables may be so related that one cannot change without the other, does not imply that they are the same variable, or that they will have the same values, or that the value of one can be obtained from the other on basis of some simple transformation. The importance of an agency achievement does not rest entirely on the enhancement of well-being that it may indirectly cause. The agency achievement and well-being achievement, both of which have some distinct importance, may be casually linked with each other, but this fact does not compromise the specific importance of either. In so far as utility - based welfare calculations concentrate only on the well- being of the person, ignoring the agency aspect, or actually fails to distinguish between the agency aspect and well-being aspect altogether, something of real importance is lost.According to the ideas in the passage, the following are not true expect:

....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?