Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Multiple Choice Question in 100/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Question Answer Bank

1. Whichthree companies formed consortium recently to set up India"s biggest refinery?

Answer: IOCL, BPCLand HPCL

Previous Question

Next Question

Add Tags

Report Error

Reply

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->Whichthree companies formed consortium recently to set up India"s biggest refinery?....

QA->ISRO hassigned an agreement with a consortium of 6 companies led by whom?....

QA->RecentlyIndia’s first Ethanol Bio- refinery set up in which state of India?....

QA->Which country has one of the highest percentages of companies where fraud, in particular corruption and bribery, was detected, according to a new survey of large local and multinational companies across industries worldwide?....

QA->Securities and Exchange Board of India (SEBI) has set up a committee to helpimprove corporate governance of listed companies, the committee, headed by....

MCQ->

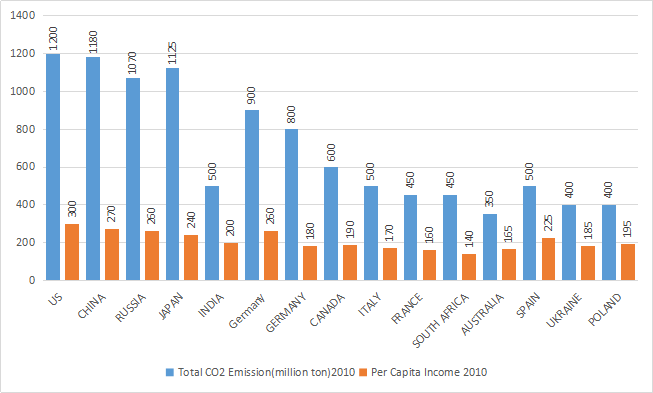

Study the following graph and answer the questions that follow

France, South Africa, Australia, Ukraine and Poland form an energy consortium which declares $$CO_2$$ emission of 350 million ton per annum as standard benchmark. The energy consortium decides to sell their carbon emission savings against the standard benchmark to high carbon emission countries. It is expected that the per capita income of each country of the energy consortium increases by 2%, 2.5% and 3.5% p.a. for the next three years respectively. The ratio of $$CO_2$$ emission to per capita income of the each energy consortium country reduces by 50% and remains constant for the next three years. By selling 0.5 $$CO_2$$ emissions [million ton] the energy consortium earns 1.25 carbon credits, then determine the total carbon credits earned by energy consortium in three years.

...

MCQ-> Read the following passage carefully and answer the questions given at the end.Passage 4Public sector banks (PSBs) are pulling back on credit disbursement to lower rated companies, as they keep a closer watch on using their own scarce capital and the banking regulator heightens its scrutiny on loans being sanctioned. Bankers say the Reserve Bank of India has started strictly monitoring how banks are utilizing their capital. Any big-ticket loan to lower rated companies is being questioned. Almost all large public sector banks that reported their first quarter results so far have showed a contraction in credit disbursal on a year-to-date basis, as most banks have shifted to a strategy of lending largely to government-owned "Navratna" companies and highly rated private sector companies. On a sequential basis too, banks have grown their loan book at an anaemic rate.To be sure, in the first quarter, loan demand is not quite robust. However, in the first quarter last year, banks had healthier loan growth on a sequential basis than this year. The country's largest lender State Bank of India grew its loan book at only 1.21% quarter-on-quarter. Meanwhile, Bank of Baroda and Punjab National Bank shrank their loan book by 1.97% and 0.66% respectively in the first quarter on a sequential basis.Last year, State Bank of India had seen sequential loan growth of 3.37%, while Bank of Baroda had seen a smaller contraction of 0.22%. Punjab National Bank had seen a growth of 0.46% in loan book between the January-March and April-June quarters last year. On a year-to-date basis, SBI's credit growth fell more than 2%, Bank of Baroda's credit growth contracted 4.71% and Bank of India's credit growth shrank about 3%. SBI chief Arundhati Bhattacharya said the bank's year-to-date credit growth fell as the bank focused on ‘A’ rated customers. About 90% of the loans in the quarter were given to high-rated companies. "Part of this was a conscious decision and part of it is because we actually did not get good fresh proposals in the quarter," Bhattacharya said.According to bankers, while part of the credit contraction is due to the economic slowdown, capital constraints and reluctance to take on excessive risk has also played a role. "Most of the PSU banks are facing pressure on capital adequacy. It is challenging to maintain 9% core capital adequacy. The pressure on monitoring capital adequacy and maintaining capital buffer is so strict that you cannot grow aggressively," said Rupa Rege Nitsure, chief economist at Bank of Baroda.Nitsure said capital conservation pressures will substantially cut down "irrational expansion of loans" in some smaller banks, which used to grow at a rate much higher than the industry average. The companies coming to banks, in turn, will have to make themselves more creditworthy for banks to lend. "The conservation of capital is going to inculcate a lot of discipline in both banks and borrowers," she said.For every loan that a bank disburses, some amount of money is required to be set aside as provision. Lower the credit rating of the company, riskier the loan is perceived to be. Thus, the bank is required to set aside more capital for a lower rated company than what it otherwise would do for a higher rated client. New international accounting norms, known as Basel III norms, require banks to maintain higher capital and higher liquidity. They also require a bank to set aside "buffer" capital to meet contingencies. As per the norms, a bank's total capital adequacy ratio should be 12% at any time, in which tier-I, or the core capital, should be at 9%. Capital adequacy is calculated by dividing total capital by risk-weighted assets. If the loans have been given to lower rated companies, risk weight goes up and capital adequacy falls.According to bankers, all loan decisions are now being assessed on the basis of the capital that needs to be set aside as provision against the loan and as a result, loans to lower rated companies are being avoided. According to a senior banker with a public sector bank, the capital adequacy situation is so precarious in some banks that if the risk weight increases a few basis points, the proposal gets cancelled. The banker did not wish to be named. One basis point is one hundredth of a percentage point. Bankers add that the Reserve Bank of India has also started strictly monitoring how banks are utilising their capital. Any big-ticket loan to lower rated companies is being questioned.In this scenario, banks are looking for safe bets, even if it means that profitability is being compromised. "About 25% of our loans this quarter was given to Navratna companies, who pay at base rate. This resulted in contraction of our net interest margin (NIM)," said Bank of India chairperson V.R. Iyer, while discussing the bank's first quarter results with the media. Bank of India's NIM, or the difference between yields on advances and cost of deposits, a key gauge of profitability, fell in the first quarter to 2.45% from 3.07% a year ago, as the bank focused on lending to highly rated customers.Analysts, however, say the strategy being followed by banks is short-sighted. "A high rated client will take loans at base rate and will not give any fee income to a bank. A bank will never be profitable that way. Besides, there are only so many PSU companies to chase. All banks cannot be chasing them all at a time. Fact is, the banks are badly hit by NPA and are afraid to lend now to big projects. They need capital, true, but they have become risk-averse," said a senior analyst with a local brokerage who did not wish to be named.Various estimates suggest that Indian banks would require more than Rs. 2 trillion of additional capital to have this kind of capital adequacy ratio by 2019. The central government, which owns the majority share of these banks, has been cutting down on its commitment to recapitalize the banks. In 2013-14, the government infused Rs. 14,000 crore in its banks. However, in 2014-15, the government will infuse just Rs. 11,200 crore.Which of the following statements is correct according to the passage?

...

MCQ->Which three companies formed consortium recently to set up India's biggest refinery?...

MCQ-> Venkat, a stockbroker, invested a part of his money in the stock of four companies --- A, B, C and D. Each of these companies belonged to different industries, viz., Cement, Information Technology (IT), Auto, and Steel, in no particular order. At the time of investment, the price of each stock was Rs.100. Venkat purchased only one stock of each of these companies. He was expecting returns of 20%, 10%, 30%, and 40% from the stock of companies A, B, C and D, respectively. Returns are defined as the change in the value of the stock after one year, expressed as a percentage of the initial value. During the year, two of these companies announced extraordinarily good results. One of these two companies belonged to the Cement or the IT industry, while the other one belonged to either the Steel or the Auto industry. As a result, the returns on the stocks of these two companies were higher than the initially expected returns. For the company belonging to the Cement or the IT industry with extraordinarily good results, the returns were twice that of the initially expected returns. For the company belonging to the Steel or the Auto industry, the returns on announcement of extraordinarily good results were only one and a half times that of the initially expected returns. For the remaining two companies, which did not announce extraordinarily good results, the returns realized during the year were the same as initially expected.What is the minimum average return Venkat would have earned during the year?

...

MCQ-> Read the following passage carefully and answer the questions given below it. Certain words/phrases are given in bold to help you locate them while answering some of the questions. Core competencies and focus are now the mantras of corporate strategists in Western economies. But while managers in the West have

dismantled

many conglomerates assembled in the 1960s and 1970s, the large, diversified business group remains the dominant form of enterprise throughout most emerging markets. Some groups operate as holding companies with full ownership in many enterprises, others are collections of publicly traded companies, but all have some degree of central control. As emerging markets open up to global competition, consultants and foreign investors are increasingly pressuring these groups to

conform to

Western practice by scaling back the scope of their business activities. The conglomer-, ate is the dinosaur of organizational design, they argue, too unwieldy and slow to compete in today’s fast-paced markets. Already a number of executives have decided to break up their groups in order to show that they are focusing on only a few core businesses. There are reasons to worry about this trend. Focus is good advice in New York or London, but something important gets lost in translation when that advice is given to groups in emerging markets. Western companies take for granted a range of institutions that support their business activities, but many of these institutions are absent in other regions of the world. Without effective securities regulation and venture capital firms, for example, focused companies may be unable to raise adequate financing; and without strong educational institutions, they will struggle to hire skilled employees. Communicating with customers is difficult when the local infrastructure is poor, and unpredictable government behavior can stymie any operation. Although a focused strategy may enable a company to perform a few activities well, companies in emerging markets must take responsibility for a wide range of functions in order to do business effectively. In the case of product markets, buyers and sellers usually suffer from a severe

dearth

of information for three reasons. First, the communications infrastructure in emerging markets is often underdeveloped. Even as wireless communication spreads throughout the West, vast stretches in countries such as China and India remain without telephones. Power shortages often render the modes of communication that do exist ineffective. The postal service is typically inefficient, slow, or unreliable; and the private sector rarely provides efficient courier services. High rates of illiteracy make it difficult for marketers to communicate effectively with customers. Second, even when information about products does get around, there are no mechanisms to corroborate the claims made by sellers. Independent consumer-information organizations are rare, and government watchdog agencies are of little use. The few analysts who rate products are generally less sophisticated than their counterparts in advanced economies. Third, consumers have no redress mechanisms if a product does not deliver on its promise. Law enforcement is often

capricious

and so slow that few who assign any value to time would resort to it. Unlike in advanced markets, there are few extrajudicial arbitration mechanisms to which one can appeal. As a result of this lack of information, companies in emerging markets face much higher costs in building credible brands than their counterparts in advanced economies. In turn, established brands wield tremendous power. A conglomerate with a reputation for quality products and services can use its group name to enter new businesses, even if those businesses are completely unrelated to its current lines. Groups also have an advantage when they do try to build up a brand because they can spread the cost of maintaining it across multiple lines of business. Such groups then have a greater incentive not to damage brand quality in any one business because they will pay the price in their other businesses as well.Which of the following sentence(s) is/are correct in the context of the given passage ? I. Consultants and foreign investors argue that the conglomerate is the dinosaur of organisational design too unvvieldly and slow to compete in today’s fast-paced markets. II. Core competencies and focus are now the mantras of corporate strategists in western economies. III. Due to lack of information required, companies in emerging markets face much higher costs in building credible brands in comparison to their counterparts in advanced economies....

×

×

Type The Issue

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions France, South Africa, Australia, Ukraine and Poland form an energy consortium which declares $$CO_2$$ emission of 350 million ton per annum as standard benchmark. The energy consortium decides to sell their carbon emission savings against the standard benchmark to high carbon emission countries. It is expected that the per capita income of each country of the energy consortium increases by 2%, 2.5% and 3.5% p.a. for the next three years respectively. The ratio of $$CO_2$$ emission to per capita income of the each energy consortium country reduces by 50% and remains constant for the next three years. By selling 0.5 $$CO_2$$ emissions [million ton] the energy consortium earns 1.25 carbon credits, then determine the total carbon credits earned by energy consortium in three years.

France, South Africa, Australia, Ukraine and Poland form an energy consortium which declares $$CO_2$$ emission of 350 million ton per annum as standard benchmark. The energy consortium decides to sell their carbon emission savings against the standard benchmark to high carbon emission countries. It is expected that the per capita income of each country of the energy consortium increases by 2%, 2.5% and 3.5% p.a. for the next three years respectively. The ratio of $$CO_2$$ emission to per capita income of the each energy consortium country reduces by 50% and remains constant for the next three years. By selling 0.5 $$CO_2$$ emissions [million ton] the energy consortium earns 1.25 carbon credits, then determine the total carbon credits earned by energy consortium in three years.