Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Multiple Choice Question in 100/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Question Answer Bank

1. Normal respiratory rates in adults is about :

Answer: 17/min

Previous Question

Next Question

Add Tags

Report Error

Reply

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->Normal respiratory rates in adults is about :....

QA->Parliament has passed a bill which has provision that allows trying of juveniles between the ages of 16 and 18 years as adults for heinous offences. What is the name of that bill?....

QA->Name the bill passed on 7 May 2015 by the Lok Sabha which paves the way for children in the 16-18 age group to be tried as adults if they commit heinous crimes?....

QA->Heart beats in adults is ?....

QA->An abnormality in Adults due to the hypersecretion of Somatotrophin?....

MCQ->Study the given information carefully and answer the given question. Following are the observations of an experiment on 'sleep and memory' conducted on 18 healthy young adults (ages 18 to 25) and 18 healthy older adults (ages 61 to 81). A. The recall after 8 hours of sleep in younger adults was 65% more than that in the older adults. B. Night-sleep had higher negative impact on all of the participants as compared to that of daysleep of equal duration. C. If a given set' of words is memorised immediately before going to sleep, its recall after waking up was found to be better in younger adults than in the older adults. Which of the following can be concluded from the given findings of the research ? I. As per the experiment, there is some correlation between sleep and memory. II. The part of brain involved in memory is more active during the day as compared to that during the night. III. A sleep of more than 8 hours can improve the memory in older adults. IV. Memorising something immediately after waking up from an 8-hour long sleep will yield better results than memorising before sleep....

MCQ-> Rearrange the following six sentences (A). (B), (C), (D), (E) and (F) in the proper sequence to form a meaningful paragraph; then answer the questions given below them. (A) As a consequence, even if it is plausible that ambient air pollution plays a role for the onset and increasing frequency of respiratory allergy, it is not easy to prove this conclusively. (B) Another factor clouding the issue is that laboratory evaluations do not reflect what happens during natural exposure when atmospheric pollution mixtures are inhaled. (C) Interpretation of studies are confounded by the effect of cigarette smoke, exposure to indoor pollutants and to outdoors and indoors allergens. (D) However, despite evidence of a correlation between the increasing frequency of respiratory allergy and the increasing trend in air pollution, the link and interaction is still speculative. (E) Allergic respiratory diseases such as hay fever and bronchial asthma have indeed become more common in the last decades in all industrialized countries and the reasons for this increase are still debated. (F) Several studies have shown the adverse effects of ambient air pollution on respiratory health.Which of the following should be the LAST sentence after rearrangement ?

...

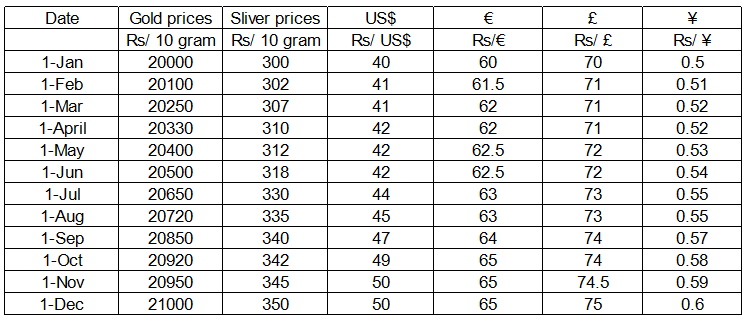

MCQ-> answer questions based on the following information:In the beginning of the year 2010, Mr. Sanyal had the option to invest Rs. 800000 in one or more of the following assets – gold, silver, US bonds, EU bonds, UK bonds and Japanese bonds. In order to invest in US bonds, one must first convert his investible fund into US Dollars at the ongoing exchange rate. Similarly, if one wants to invest in EU bonds or UK bonds or Japanese bonds one must first convert his investible fund into Euro, British Pounds and Japanese Yen respectively at the ongoing exchange rates. Transactions were allowed only in the beginning of every month. Bullion prices and exchange rates were fixed at the beginning of every month and remained unchanged throughout the month. Refer to the table titled “Bullion Prices and Exchange Rates in 2010" for the relevant data.

Bullion Prices and Exchange Rates in 2010

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

...

MCQ->Three pipes A, B and C are connected to a tank. These pipes can fill the tank separately in 5 hours, 10 hours and 15 hours respectively. When all the three pipes were opened simultaneously, it was observed that pipes A and B were supplying water at 3/4th of their normal rates for the first hour after which they supplied water at the normal rate. Pipe C supplied water at 2/3rd of its normal rate for first 2 hours, after which it supplied at its normal rate. In how much time, tank would be filled....

MCQ-> Read the following passage carefully and answer the questions given below it. Certain words/phrases have been printed in bold tohelp you locate them while answering some of the questions. During the last few years, a lot of hype has been heaped on the BRICS (Brazil, Russia, India, China, and South Africa). With their large populations and rapid growth, these countries, so the argument goes, will soon become some of the largest economies in the world and, in the case of China, the largest of all by as early as 2020. But the BRICS, as well as many other emerging-market economieshave recently experienced a sharp economic slowdown. So, is the honeymoon over? Brazil’s GDP grew by only 1% last year, and may not grow by more than 2% this year, with its potential growth barely above 3%. Russia’s economy may grow by barely 2% this year, with potential growth also at around 3%, despite oil prices being around $100 a barrel. India had a couple of years of strong growth recently (11.2% in 2010 and 7.7% in 2011) but slowed to 4% in 2012. China’s economy grew by 10% a year for the last three decades, but slowed to 7.8% last year and risks a hard landing. And South Africa grew by only 2.5% last year and may not grow faster than 2% this year. Many other previously fast-growing emerging-market economies – for example, Turkey, Argentina, Poland, Hungary, and many in Central and Eastern Europe are experiencing a similar slowdown. So, what is ailing the BRICS and other emerging markets? First, most emerging-market economies were overheating in 2010-2011, with growth above potential and inflation rising and exceeding targets. Many of them thus tightened monetary policy in 2011, with consequences for growth in 2012 that have carried over into this year. Second, the idea that emerging-market economies could fully decouple from economic weakness in advanced economies was

farfetched

: recession in the eurozone, near-recession in the United Kingdom and Japan in 2011-2012, and slow economic growth in the United States were always likely to affect emerging market performance negatively – via trade, financial links, and investor confidence. For example, the ongoing euro zone downturn has hurt Turkey and emergingmarket economies in Central and Eastern Europe, owing to trade links. Third, most BRICS and a few other emerging markets have moved toward a variant of state capitalism. This implies a slowdown in reforms that increase the private sector’s productivity and economic share, together with a greater economic role for state-owned enterprises (and for state-owned banks in the allocation of credit and savings), as well as resource nationalism, trade protectionism, import substitution industrialization policies, and imposition of capital controls. This approach may have worked at earlier stages of development and when the global financial crisis caused private spending to fall; but it is now distorting economic activity and depressing potential growth. Indeed, China’s slowdown reflects an economic model that is, as former Premier Wen Jiabao put it, “unstable, unbalanced, uncoordinated, and unsustainable,” and that now is adversely affecting growth in emerging Asia and in commodity-exporting emerging markets from Asia to Latin America and Africa. The risk that China will experience a hard landing in the next two years may further hurt many emerging economies. Fourth, the commodity super-cycle that helped Brazil, Russia, South Africa, and many other commodity-exporting emerging markets may be over. Indeed, a boom would be difficult to sustain, given China’s slowdown, higher investment in energysaving technologies, less emphasis on capital-and resource-oriented growth models around the world, and the delayed increase in supply that high prices induced. The fifth, and most recent, factor is the US Federal Reserve’s signals that it might end its policy of quantitative easing earlier than expected, and its hints of an even tual exit from zero interest rates. both of which have caused turbulence in emerging economies’ financial markets. Even before the Fed’s signals, emergingmarket equities and commodities had underperformed this year, owing to China’s slowdown. Since then, emerging-market currencies and fixed-income securities (government and corporate bonds) have taken a hit. The era of cheap or zerointerest money that led to a wall of liquidity chasing high yields and assets equities, bonds, currencies, and commodities – in emerging markets is drawing to a close. Finally, while many emerging-market economies tend to run current-account surpluses, a growing number of them – including Turkey, South Africa, Brazil, and India – are running deficits. And these deficits are now being financed in riskier ways: more debt than equity; more short-term debt than longterm debt; more foreign-currency debt than local-currency debt; and more financing from fickle cross-border interbank flows. These countries share other weaknesses as well: excessive fiscal deficits, abovetarget inflation, and stability risk (reflected not only in the recent political turmoil in Brazil and Turkey, but also in South Africa’s labour strife and India’s political and electoral uncertainties). The need to finance the external deficit and to avoid excessive depreciation (and even higher inflation) calls for raising policy rates or keeping them on hold at high levels. But monetary tightening would weaken already-slow growth. Thus, emerging economies with large twin deficits and other macroeconomic fragilities may experience further downward pressure on their financial markets and growth rates. These factors explain why growth in most BRICS and many other emerging markets has slowed sharply. Some factors are cyclical, but others – state capitalism, the risk of a hard landing in China, the end of the commodity supercycle -are more structural. Thus, many emerging markets’ growth rates in the next decade may be lower than in the last – as may the outsize returns that investors realised from these economies’ financial assets (currencies, equities. bonds, and commodities). Of course, some of the better-managed emerging-market economies will continue to experitnce rapid growth and asset outperformance. But many of the BRICS, along with some other emerging economies, may hit a thick wall, with growth and financial markets taking a serious beating.Which of the following statement(s) is/are true as per the given information in the passage ? A. Brazil’s GDP grew by only 1% last year, and is expected to grow by approximately 2% this year. B. China’s economy grew by 10% a year for the last three decades but slowed to 7.8% last year. C. BRICS is a group of nations — Barzil, Russia, India China and South Africa....

×

×

Type The Issue

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?