1. Which country’s central bank bought 200 metric tons of gold from the International Monetary Fund last month, in the first major move by a major central bank to diversify its foreign-exchange reserves?

Answer: India.

Tags

Show Similar Question And Answers

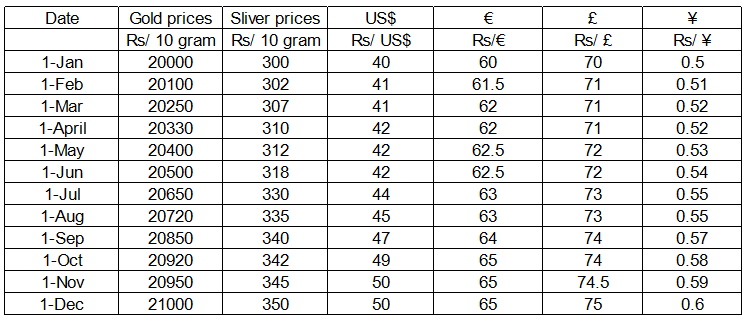

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?