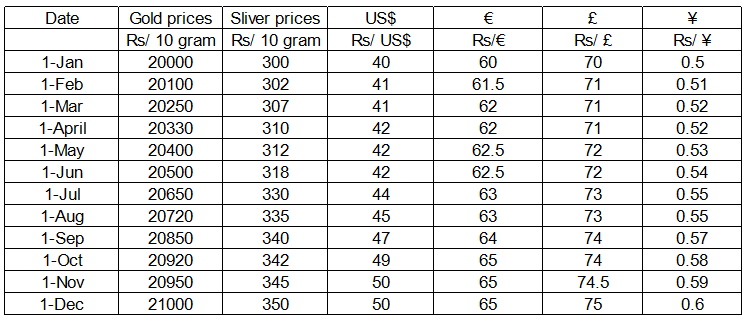

1. Mr. Sanyal adopted the following investment strategy. On lst January 2010 he invested half of his investible fund in gold and the other half he kept in fixed deposit of an Indian bank that offered 25% interest per annum. At the beginning of every quarter he liquefied his assets to create his investible fund for that quarter. Every quarter he invested half of his fund in the bullion that gave maximum return in the previous quarter and the other half in the foreign bond that gave maximum return in the previous quarter. However, if in any quarter none of the foreign bonds gave a better return than the fixed deposit of his Indian bank, he invested half of his investible fund in the fixed deposit for the next quarter. On 31st December 2010 Mr. Sanyal liquefied his assets and realized that all of the following options are true except:

Show Similar Question And Answers

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?