1. Under pressure from media and suppliers, Ava constituted a cross-functional committee of senior executives to investigate Dev and Sons' allegation against Bhushan. The committee exonerated Bhushan. However, rumors within the organization began to spread that the decision was influenced by nepotism.Which of the following should be the best response from Ava?

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

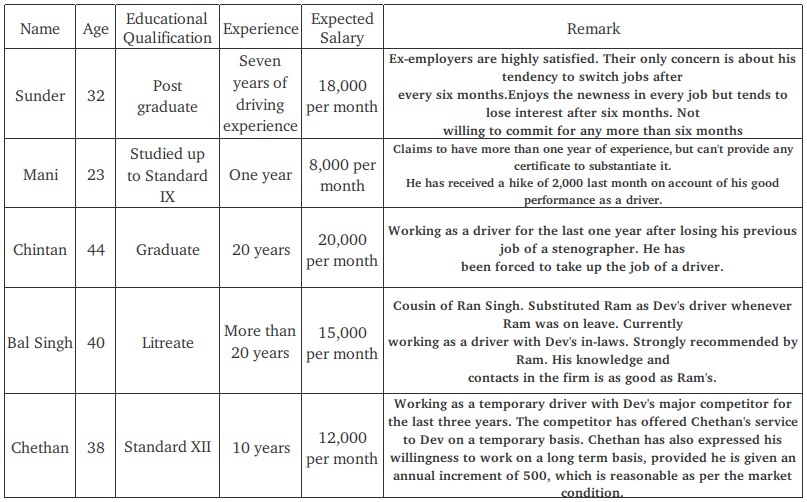

Dev is primarily looking for a stable and trustworthy driver, who can be a suitable replacement for Ram. His family members do not want Dev to appoint a young driver, as most of them are inexperienced. Dev’s driver is an employee of the firm and hence the appointment has to be routed through the HR manager of the firm. The HR manager prefers to maintain parity among all employees of the firm. He also needs to ensure that the selection of a new driver does not lead to discontent among the senior employees of the firm.

From his perspective, and taking into account the family’s concerns, Mr. Dev would like to have

Dev is primarily looking for a stable and trustworthy driver, who can be a suitable replacement for Ram. His family members do not want Dev to appoint a young driver, as most of them are inexperienced. Dev’s driver is an employee of the firm and hence the appointment has to be routed through the HR manager of the firm. The HR manager prefers to maintain parity among all employees of the firm. He also needs to ensure that the selection of a new driver does not lead to discontent among the senior employees of the firm.

From his perspective, and taking into account the family’s concerns, Mr. Dev would like to have