Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in

Multiple Choice Question in 049

Multiple Choice Question in 2016

Multiple Choice Question in -current-affairs-2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. NaCl has which kind of bonds?

(A): nonpolar bonds

(B): polar covalent bonds

(C): Metallic bonds

(D): ionic bonds

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

SSC CHSL 20 Jan 2017 Morning Shift

Show Similar Question And Answers

QA->NewDevelopment Bank of the BRICS countries is set to issue its first which country currency denominated bonds?....

QA->Orbital interaction between the sigma bonds of a substituent group and a neighboring pi orbital is known as :....

QA->Bonds issued without any rate of interest is called:....

QA->What is the maximum number of hydrogen bonds in a H2O molecule?....

QA->RBI hasgiven banks the right to issue masala bonds in foreign markets, also known as....

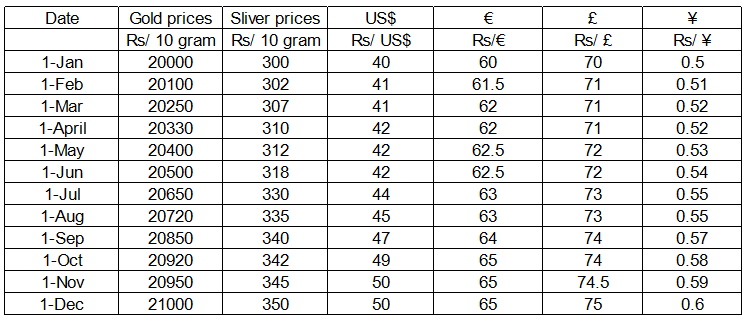

MCQ-> answer questions based on the following information:In the beginning of the year 2010, Mr. Sanyal had the option to invest Rs. 800000 in one or more of the following assets – gold, silver, US bonds, EU bonds, UK bonds and Japanese bonds. In order to invest in US bonds, one must first convert his investible fund into US Dollars at the ongoing exchange rate. Similarly, if one wants to invest in EU bonds or UK bonds or Japanese bonds one must first convert his investible fund into Euro, British Pounds and Japanese Yen respectively at the ongoing exchange rates. Transactions were allowed only in the beginning of every month. Bullion prices and exchange rates were fixed at the beginning of every month and remained unchanged throughout the month. Refer to the table titled “Bullion Prices and Exchange Rates in 2010" for the relevant data.

Bullion Prices and Exchange Rates in 2010

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

....

MCQ-> Answer the questions based on the information given below: Madhubala Devi, who works as a domestic help, received Rs. 2500 as Deepawali bonus from her employer. With that money she is contemplating purchase of one or more among 5 available government bonds - A, B, C, D and E. To purchase a bond Madhubala Devi will have to pay the price of the bond. If she owns a bond she receives a stipulated amount of money every year (which is termed as the coupon payment) till the maturity of the bond. At the maturity of the bond she also receives the face value of the bond. Price of a bond is given by: $$P=[\sum_{t=1}^T\frac{C}{(1+r)^{t}}]+\frac{F}{(1+r)^{t}}$$ where C is coupon payment on the bond. which is the amount of money the holder of the bond receives annually; F is the face value of the bond, which is the amount of money the holder of the bond receives when the bond matures (over and above the coupon payment for the year of maturity); T is the number of years in which the bond matures; R = 0.25, which means the market rate of interest is 25%. Among the 5 bonds the bond A and another two bonds mature in 2 years, one of the bonds matures in 3 years, and the bond D matures in 5 years. The coupon payments on bonds A, E, B, D and C are in arithmetic progression, such that the coupon payment on bond A is twice the common difference, and the coupon payment on bond B is half the price of bond A. The face value of bond B is twice the face value of bond E, but the price of bond B is 75% more than the price of bond E. The price of bond C is more than Rs. 1800 and its face value is same as the price of bond A. The face value of bond A is Rs. 1000. Bond D has the largest face value among the five bonds.The face value of bond E must be

....

MCQ-> I think that it would be wrong to ask whether 50 years of India's Independence are an achievement or a failure. It would be better to see things as evolving. It's not an either-or question. My idea of the history of India is slightly contrary to the Indian idea.India is a country that, in the north, outside Rajasthan, was ravaged and intellectually destroyed to a large extent by the invasions that began in about AD 1000 by forces and religions that India had no means of understanding.The invasions are in all the schoolbooks. But I don't think that people understand that every invasion, every war, every campaign, was accompanied by slaughter, a slaughter always of the most talented people in the country. So these wars, apart from everything else led to a tremendous intellectual depletion of the country.I think that in the British period, and in the 50 years after the British period, there has been a kind of regrouping or recovery, a very slow revival of energy and intellect. This isn't an idea that goes with the vision of the grandeur of old India and all that sort of rubbish. That idea is a great simplification and it occurs because it is intellectually, philosophically easier for Indians to manage.What they cannot manage, and what they have not yet come to terms with, is that ravaging of all the north of India by various conquerors. That was ruined not by the act of nature, but by the hand of man. It is so painful that few Indians have begun to deal with it. It is much easier to deal with British imperialism. That is a familiar topic, in India and Britain. What is much less familiar is the ravaging of India before the British.What happened from AD 1000 onwards, really, is such a wound that it is almost impossible to face. Certain wounds are so bad that they can't be written about. You deal with that kind of pain by hiding from it. You retreat from reality. I do not think, for example, that the Incas of Peru or the native people of Mexico have ever got over their defeat by the Spaniards. In both places the head was cut off. I think the pre-British ravaging of India was as bad as that.In the place of knowledge of history, you have various fantasies about the village republic and the Old Glory. There is one big fantasy that Indians have always found solace in: about India having the capacity for absorbing its conquerors. This is not so. India was laid low by its conquerors.I feel the past 150 years have been years of every kind of growth. I see the British period and what has continued after that as one period. In that time, there has been a very slow intellectual recruitment. I think every Indian should make the pilgrimage to the site of the capital of the Vijayanagar empire, just to see what the invasion of India led to. They will see a totally destroyed town. Religious wars are like that. People who see that might understand what the centuries of slaughter and plunder meant. War isn't a game. When you lost that kind of war, your town was destroyed, the people who built the towns were destroyed. You are left with a headless population.That's where modern India starts from. The Vijayanagar capital was destroyed in 1565. It is only now that the surrounding region has begun to revive. A great chance has been given to India to start up again, and I feel it has started up again. The questions about whether 50 years of India since Independence have been a failure or an achievement are not the questions to ask. In fact, I think India is developing quite marvelously, people thought — even Mr Nehru thought — that development and new institutions in a place like Bihar, for instance, would immediately lead to beauty. But it doesn't happen like that. When a country as ravaged as India, with all its layers of cruelty, begins to extend justice to people lower down, it's a very messy business. It's not beautiful, it's extremely messy. And that's what you have now, all these small politicians with small reputations and small parties. But this is part of growth, this is part of development. You must remember that these people, and the people they represent, have never had rights before.When the oppressed have the power to assert themselves, they will behave badly. It will need a couple of generations of security, and knowledge of institutions, and the knowledge that you can trust institutions — it will take at least a couple of generations before people in that situation begin to behave well. People in India have known only tyranny. The very idea of liberty is a new idea. The rulers were tyrants. The tyrants were foreigners. And they were proud of being foreign. There's a story that anybody could run and pull a bell and the emperor would appear at his window and give justice. This is a child's idea of history — the slave's idea of the ruler's mercy. When the people at the bottom discover that they hold justice in their own hands, the earth moves a little. You have to expect these earth movements in India. It will be like this for a hundred years. But it is the only way. It's painful and messy and primitive and petty, but it’s better that it should begin. It has to begin. If we were to rule people according to what we think fit, that takes us back to the past when people had no voices. With self-awareness all else follows. People begin to make new demands on their leaders, their fellows, on themselves.They ask for more in everything. They have a higher idea of human possibilities. They are not content with what they did before or what their fathers did before. They want to move. That is marvellous. That is as it should be. I think that within every kind of disorder now in India there is a larger positive movement. But the future will be fairly chaotic. Politics will have to be at the level of the people now. People like Nehru were colonial — style politicians. They were to a large extent created and protected by the colonial order. They did not begin with the people. Politicians now have to begin with the people. They cannot be too far above the level of the people. They are very much part of the people. It is important that self-criticism does not stop. The mind has to work, the mind has to be active, there has to be an exercise of the mind. I think it's almost a definition of a living country that it looks at itself, analyses itself at all times. Only countries that have ceased to live can say it's all wonderful.The central thrust of the passage is that

....

MCQ-> Read the following passage carefully and answer the questions given below it. Certain words/phrases have been printed in bold tohelp you locate them while answering some of the questions. During the last few years, a lot of hype has been heaped on the BRICS (Brazil, Russia, India, China, and South Africa). With their large populations and rapid growth, these countries, so the argument goes, will soon become some of the largest economies in the world and, in the case of China, the largest of all by as early as 2020. But the BRICS, as well as many other emerging-market economieshave recently experienced a sharp economic slowdown. So, is the honeymoon over? Brazil’s GDP grew by only 1% last year, and may not grow by more than 2% this year, with its potential growth barely above 3%. Russia’s economy may grow by barely 2% this year, with potential growth also at around 3%, despite oil prices being around $100 a barrel. India had a couple of years of strong growth recently (11.2% in 2010 and 7.7% in 2011) but slowed to 4% in 2012. China’s economy grew by 10% a year for the last three decades, but slowed to 7.8% last year and risks a hard landing. And South Africa grew by only 2.5% last year and may not grow faster than 2% this year. Many other previously fast-growing emerging-market economies – for example, Turkey, Argentina, Poland, Hungary, and many in Central and Eastern Europe are experiencing a similar slowdown. So, what is ailing the BRICS and other emerging markets? First, most emerging-market economies were overheating in 2010-2011, with growth above potential and inflation rising and exceeding targets. Many of them thus tightened monetary policy in 2011, with consequences for growth in 2012 that have carried over into this year. Second, the idea that emerging-market economies could fully decouple from economic weakness in advanced economies was

farfetched

: recession in the eurozone, near-recession in the United Kingdom and Japan in 2011-2012, and slow economic growth in the United States were always likely to affect emerging market performance negatively – via trade, financial links, and investor confidence. For example, the ongoing euro zone downturn has hurt Turkey and emergingmarket economies in Central and Eastern Europe, owing to trade links. Third, most BRICS and a few other emerging markets have moved toward a variant of state capitalism. This implies a slowdown in reforms that increase the private sector’s productivity and economic share, together with a greater economic role for state-owned enterprises (and for state-owned banks in the allocation of credit and savings), as well as resource nationalism, trade protectionism, import substitution industrialization policies, and imposition of capital controls. This approach may have worked at earlier stages of development and when the global financial crisis caused private spending to fall; but it is now distorting economic activity and depressing potential growth. Indeed, China’s slowdown reflects an economic model that is, as former Premier Wen Jiabao put it, “unstable, unbalanced, uncoordinated, and unsustainable,” and that now is adversely affecting growth in emerging Asia and in commodity-exporting emerging markets from Asia to Latin America and Africa. The risk that China will experience a hard landing in the next two years may further hurt many emerging economies. Fourth, the commodity super-cycle that helped Brazil, Russia, South Africa, and many other commodity-exporting emerging markets may be over. Indeed, a boom would be difficult to sustain, given China’s slowdown, higher investment in energysaving technologies, less emphasis on capital-and resource-oriented growth models around the world, and the delayed increase in supply that high prices induced. The fifth, and most recent, factor is the US Federal Reserve’s signals that it might end its policy of quantitative easing earlier than expected, and its hints of an even tual exit from zero interest rates. both of which have caused turbulence in emerging economies’ financial markets. Even before the Fed’s signals, emergingmarket equities and commodities had underperformed this year, owing to China’s slowdown. Since then, emerging-market currencies and fixed-income securities (government and corporate bonds) have taken a hit. The era of cheap or zerointerest money that led to a wall of liquidity chasing high yields and assets equities, bonds, currencies, and commodities – in emerging markets is drawing to a close. Finally, while many emerging-market economies tend to run current-account surpluses, a growing number of them – including Turkey, South Africa, Brazil, and India – are running deficits. And these deficits are now being financed in riskier ways: more debt than equity; more short-term debt than longterm debt; more foreign-currency debt than local-currency debt; and more financing from fickle cross-border interbank flows. These countries share other weaknesses as well: excessive fiscal deficits, abovetarget inflation, and stability risk (reflected not only in the recent political turmoil in Brazil and Turkey, but also in South Africa’s labour strife and India’s political and electoral uncertainties). The need to finance the external deficit and to avoid excessive depreciation (and even higher inflation) calls for raising policy rates or keeping them on hold at high levels. But monetary tightening would weaken already-slow growth. Thus, emerging economies with large twin deficits and other macroeconomic fragilities may experience further downward pressure on their financial markets and growth rates. These factors explain why growth in most BRICS and many other emerging markets has slowed sharply. Some factors are cyclical, but others – state capitalism, the risk of a hard landing in China, the end of the commodity supercycle -are more structural. Thus, many emerging markets’ growth rates in the next decade may be lower than in the last – as may the outsize returns that investors realised from these economies’ financial assets (currencies, equities. bonds, and commodities). Of course, some of the better-managed emerging-market economies will continue to experitnce rapid growth and asset outperformance. But many of the BRICS, along with some other emerging economies, may hit a thick wall, with growth and financial markets taking a serious beating.Which of the following statement(s) is/are true as per the given information in the passage ? A. Brazil’s GDP grew by only 1% last year, and is expected to grow by approximately 2% this year. B. China’s economy grew by 10% a year for the last three decades but slowed to 7.8% last year. C. BRICS is a group of nations — Barzil, Russia, India China and South Africa.....

MCQ->NaCl has which kind of bonds?....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?