1.

Study the following graph carefully and answer the questions given below it :

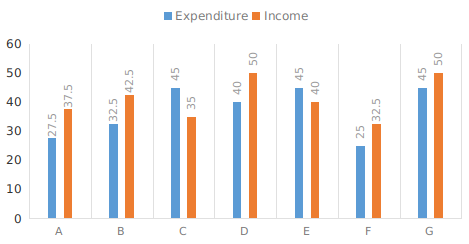

Account of income and expenditure (in crores) of seven companies in the year 2007 Approximately what is the percentage of profit/loss that Companies C and D had together ?

Approximately what is the percentage of profit/loss that Companies C and D had together ?

Write Comment

Comments

- By: anil on 05 May 2019 01.27 amTotal incomes of companies C & D = 35 + 50 = 85 cr Total expenditures of companies C & D = 45 + 40 = 85 cr Since, both are same, => There is no profit or loss.

Show Similar Question And Answers

Profit = Income – Expenditure;

Loss = Expenditure –Income;

Profit %= profit/expenditure*100(latex)

Loss%= Loss/expenditure*100(latex)What is the approximate average profit (in Rs. thousand) of the company in the years 2007,2009 and 2010?

Profit = Income – Expenditure;

Loss = Expenditure –Income;

Profit %= profit/expenditure*100(latex)

Loss%= Loss/expenditure*100(latex)What is the approximate average profit (in Rs. thousand) of the company in the years 2007,2009 and 2010?