Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in -current-affairs-2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. Which one of the following will lead to understatement of net profit?

(A): Amortization of fictitious assets

(B): Treating capital expenditure as revenue expenditure

(C): Treating revenue expenditure as capital expenditure

(D): Creation of general reserve

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->As per Co-operative societies rule ‘Net profit’ means net profit as certified by :....

QA->A farmer has 50 kg wheat in hand, part of which he sells at 8% profit and the rest at 18% profit. He gains 14% altogether. What is the quantity of wheat sold by him at 18% profit?....

QA->The violence in the plant _____ Maruti’s net profit by 41%....

QA->As per the section 33 of the Co-operative Societies Act, 1912 the first 25% of the net profit earned during any year should be transferred to?....

QA->“One vision, One identity, One Community” is the motto of which of the following organizations?....

MCQ-> Questions are based on a set of conditions. In answering some of the questions, it may be useful to draw a rough diagram. Choose the response that most accurately and completely answers each question. Seven bands were scheduled to perform during the week long music festival at XLRI. The festival began on a Monday evening and ended on the Sunday evening. Each day only one band performed. Each band performed only once. The organizing committee had the task of scheduling the performances of the seven bands - Cactus, Axis, Enigma, Boom, Fish, Dhoom and Bodhi Tree. The festival schedule followed the following conditions: the performance of Bodhi. Tree, the home band of XLRI, did not precede the performance of any other band. Among the visiting bands three were rock bands and the other three were fusion bands. All three bands of the same genre were not allowed to perform consecutively. Boom, which was a rock band, refused to perform immediately before or after Fish. Meet, who was a lead vocalist with a rock band, refused to perform after Angelina. Angelina, the only female lead vocalist in the music fest besides Bony, was with the band Enigma. Angelina refused to perform after Thursday citing personal reasons. Ali, who was the lead vocalist of a rock band, was not with the band Dhoom, and did not perform on Saturday. Sid, the lead vocalist of the rock band Cactus, could perform only on Monday. Rupam, the only male among the lead vocalists of the fusion bands, was with Fish and performed on Wednesday. None of the bands performed in absence of their lead vocalist.All of the following statements can be true except:

....

MCQ->Which one of the following will lead to understatement of net profit?....

MCQ-> Read the following passage based on an Interview to answer the given questions based on it. Certain words are printed in bold to help you locate them while answering some of the questions.A spate of farmer suicides linked to harassment by recovery agents employed by micro finance institutions (MFLs) in Andhra Pradesh

spurned

the state government to bring in regulation to protect consumer interests. But, while the Bill has brought into sharp focus the need for consumer protection, it tries to micro-manage MFI operations and in the process it could

scuttle

some of the crucial bene ts that MFIs bring to farmers, says the author of Micro nance India, State Of The Sec-for Report 2010. In an interview he points out that prudent regulation can ensure the original goal of the MFIs - social uplift of the poor.

Do you feel the AP Bill to regulate Mils is well thought out? Does it ensure fairness to the borrowers and the long-term health of the sector?

The AP Bill has brought into sharp focus the need for customer protection in four critical areas. First is pricing. Second is lender's liability whether the lender can give too much loan without assessing the customer's ability to pay. Third is the structure of loan repayment - whether you can ask money on a weekly basis from people who don't produce weekly incomes. Fourth is the practices that attend to how you deal with defaults. But the Act should have looked at the positive bene ts that institutions could bring in, and where they need to be regulated in the interests of the customers. It should have brought only those features in. Say, you want the recovery practices to be consistent with what the customers can really

manage

. If the customer is aggrieved and complains that somebody is harassing him, then those complaints should be investigated by the District Rural Development Authority. Instead what the Bill says is that MF1s cannot go to the customer's premises to ask for recovery and that all transactions will be done in the Panchayat of ce. With great dif culty, MFIs brought services to the door of people. It is such a relief for the customers not to be spending time out going to banks or Panchayat of ces, which could be 10 km away in some cases. A facility which has brought some relief to people is being shut. Moreover, you are practically telling the MFI where it should do business and how it should do it.

Social responsibilities were inbuilt when the MIrls were rst conceived. If kills go for profit with loose regulations, how are they different from moneylenders?

Even among moneylenders there are very good people who take care of the customer's circumstance, and there are really bad ones. A large number of the MF1s are good and there are some who are coercive because of the kind of prices and processes they have adopted. But Moneylenders never got this organised. They did not have such a large footprint. An MFI brought in organisation, it mobilized the equity, it brought in commercial funding. It invested in systems. It appointed a large number of people. But some of them

exacted

a much higher price than they should have. They wanted to break even very fast and greed did take over in some cases.

Are the for-profit 'Ms the only ones harassing people for recoveries?

Some not-for-profit out ts have also adopted the same kind of recovery methods. That may be because you have to show that you are very ef cient in your recovery methods and that your portfolio is of a very high quality if you want to get commercial funding from a bank. In fact, among for-profits there are many who have sensible recovery practices. Some have fortnightly recovery, some have monthly recovery. So we have differing practices. We just describe a few dominant ones and assume every for-profit MFI operates like that. How can you introduce regulations to ensure social upliftment in a sector that is moving towards for-profit models? I am not really concerned whether someone wants to make a profit or not The bottom-line for me is customer protection. The rst area is fair practices. Are you telling your customers how the loan is structured ? Are you being transparent about your performance? There should also be a lender's liability attached to what you do. Suppose you lend excessively to a customer without assessing their ability to service the loan, you have to take the hit. Then there's the question of limiting returns. You can say that an MFI cannot have a return on assets more than X, a return on equity of more than Y. Then suppose there is a privately promoted MFI, there should be a regulation to ensure the MFI cannot access equity markets till a certain amount of time. MFIs went to markets perhaps because of the need to grow too big too fast. The government thought they were making profit off the poor, and that's an indirect reason why they decided to clamp down on MF1s. If you say an MFI won't go to capital market, then it will keep political compulsions under rein.Which of the following best explains "structure of loan repayment" in this context of the rst question asked to the author ?....

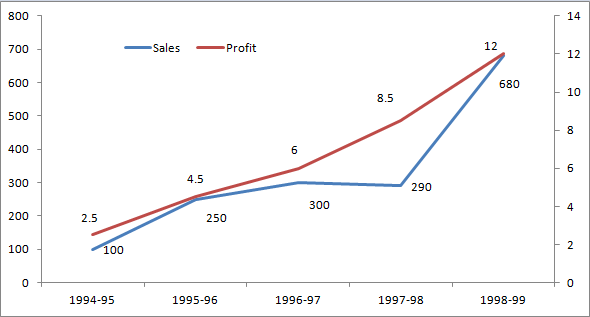

MCQ-> These questions are based on the situation given below: The figure below presents sales and net profit, in Rs. Crores, of IVP Ltd for the five years from 1994-95 to 1998-99. During this period, the sales increased from Rs.100 Crores to Rs. 680 Crores. Correspondingly, the net profit increased from Rs. 2.5 Crores to Rs. 12 Crores. Net profit is defined as the excess of sales over total costs.

The highest percentage of growth in sales, relative to the previous year, occurred in

....

MCQ-> Directions: Read the following passage carefully and answer the questions given below it. Certain words/phrases have been printed in bold to help you locate them while answering some of the questions. When times are hard, doomsayers are aplenty. The problem is that if you listen to them too carefully, you tend to overlook the most obvious signs of change. 2011 was a bad year. Can 2012 be any worse? Doomsday forecasts are the easiest to make these days. So let's try a contrarian's forecast instead. Let's start with the global economy. We have seen a steady flow of good news from the US. The employment situation seems to be improving rapidly and consumer sentiment, reflected in retail expenditures on discretionary items like electronics and clothes, has picked up. If these trends sustain, the US might post better growth numbers for 2012 than the 1.5 - 1.8 percent being forecast currently. Japan is likely to pull out of a recession in 2012 as post-earthquake reconstruction efforts gather momentum and the fiscal stimulus announced in 2011 begin to pay off. The consensus estimate for growth in Japan is a respectable 2 percent for 2012. The "hard landing' scenario for China remains and will remain a myth. Growth might decelerate further from the 9 percent that is expected to clock in 2011 but is unlikely to drop below 8 - 8.5 percent in 2012. Europe is certainly in a spot of trouble. It is perhaps already in recession and for 2012 it is likely to post mildly negative growth. The risk of implosion has dwindled over the last few months- peripheral economies like Greece, Italy and Spain have new governments in place and have made progress towards genuine economic reform. Even with some these positive factors in place, we have to accept the fact that global growth in 2012 will be tepid. But there is a flipside to this. Softer growth means lower demand for commodities, and this is likely to drive a correction in commodity prices. Lower commodity inflation will enable emerging market central banks to reverse their monetary stance. China, for instance, has already reversed its stance and have pared its reserve ratio twice. The RBI also seems poised for a reversal in its rate cycle as headline inflation seems well one its way to its target of 7 percent for March 2012. That said, oil might be an exception to the general trend in commodities. Rising geopolitical tensions, particularly the continuing face-off between Iran and the US, might lead to a spurt in prices. It might make sense for our oil companies to hedge this risk instead of buying oil in the spot market. As inflation fears abate, and emerging market central banks begin to cut rates, two things could happen. Lower commodity inflation would mean lower interest rates and better credit availability. This could set the floor to growth and slowly reverse the business cycle within these economies. Second, as the fear of untamed, runaway inflation in these economies abates, the global investor's comfort levels with their markets will increase. Which of the emerging markets will outperform and who will leave behind? In an environment in which global growth is likely to be weak, economies like India that have a powerful domestic consumption dynamic should lead; those dependent on exports should, prima facie, fall behind. Specifically for India, a fall in the exchange rate could not have come at a better time. It will help Indian exporters gain market share even if global trade remains depressed. More importantly, it could lead to massive import substitution that favours domestic producers.Let’s now focus on India and start with a caveat. It is important not to confuse a short run cyclical dip with a permanent derating of its long-term structural potential. The arithmetic is simple. Our growth rate can be in the range of 7-10 percent depending on policy action. Ten percent if we get everything right, 7 percent if we get it all wrong. Which policies and reforms are critical to taking us to our 10 percent potential? In judging this, let’s again be careful. Let’s not go by the laundry list of reforms that FIIs like to wave: The increase in foreign equity limits in foreign shareholding, greater voting rights for institutional shareholders in banks, FDI in retail, etc. These can have an impact only at the margin. We need not bend over backwards to appease the FIIs through these reforms they will invest in our markets when momentum picks up and will be the first to exit when the momentum flags, reforms or not. The reforms that we need are the ones that can actually raise our sustainable longterm growth rate. These have to come in areas like better targeting of subsidies, making projects in infrastructure viable so that they draw capital, raising the productivity of agriculture, improving healthcare and education, bringing the parallel economy under the tax net, implementing fundamental reforms in taxation like GST and the direct tax code and finally easing the myriad rules and regulations that make doing business in India such a nightmare. A number of these things do not require new legislation and can be done through executive order.Which of the following is not true according to the passage?

....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions The highest percentage of growth in sales, relative to the previous year, occurred in

The highest percentage of growth in sales, relative to the previous year, occurred in