Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Question Answer Bank

1. Which is the unit raised to protect the naval assets?

Answer: Sagar Prahari Bal

Previous Question

Next Question

Add Tags

Report Error

Reply

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->Which is the unit raised to protect the naval assets?....

QA->Name of a new force which will be created by the Indian Navy to protect Naval bases and border the coastline areas?....

QA->Which Naval submarine caught fired and sunk at Naval Dockyard in Colaba, Mumbai ?....

QA->BCG Vaccination is given to protect against:....

QA->National energy protect day....

MCQ-> Read the following passage carefully and answer the questions based on it. Some words have been printed in bold to help you locate them while answering some of the questions.Notwithstanding the fact that the share of household savings to GDS is showing decline, still this segment is the significant contributor to GDS with 70% share. Indian households are among the most frugal in the world However,

commensurate

capital formation has not been taking place as a lion's share of household savings are being parked in physical assets compared to financial assets. The pattern of disposition of saving is an important factor in determining how the saved amount is utilized for productive purposes. The proportion of household saving in financial assets determines the channelisation of saving for investment in other sectors of the economy. However, the volume of investment of saving in physical assets determines the productivity and generation of income in that sector itself. Post-Independence era has witnessed a significant shift in deployment of household savings especially the share of financial assets increased from 26.39% in 1950 to 54.05% in 1990 may be on account of increased bank branch network across the country coupled with improved awareness of investors on various financial / banking products. However, contrast to common expectations, the share of financial assets in total household savings has come down from 54.05% to 50.21% especially in post reform period i.e. 1990 to 2010 despite providing easy access and availability of banking facilities compared to earlier years. The increased share of physical assets over financial assets (around 4%) during the last two decades is a cause of concern requires focused attention to arrest the trend. Traditionally, the Indians are risk-averse and prefer to invest surplus funds in physical assets such as Gold, Silver and lands. Nevertheless, considerable share of savings also owing to financial assets, which includes, Currency, Bank Deposits, Claims on Government,

Contractual

Savings, Equities The composition of household financial savings shows that the bank deposits (44%) continue to remain the major contributor along with the rise in the Contractual Savings, Claims on Government and Currency. Though there was gradual decline in currency holdings by the households i.e. 13.79% in 1970s to 9.30% in 2007, still the present currency holding level with households appears to be on high side compared to other countries. The primary reasons for higher currency holdings could be absence of banking facilities in majority villages (5.70 lakh villages)as well as hoarding of unaccounted money in the form of cash to circumvent tax laws. Though, cash is treated as financial asset, in reality, a major portion of currency is blocked and become unproductive. Bank deposits seemed to be the preferred choice mainly on account of its inbuilt features such as Safety, Security and Liquidity. Traditionally, the Household sector has been playing a leading role in the landscape of bank deposits followed by the Government sector. However, the last two decades has witnessed significant shift in ownership of Bank deposits. While there was improvement in Corporate and Government sectors' share by 8.30% and 7.20% respectively during the period 1999 to 2009, household sector lost a share of 13.30% in the post reform period. In the post independence era, Indian financial system was characterized by poor infrastructure and low level of financial deepening. Savings in physical assets constituted the largest portion of the savings compared to the financial assets in the initial years of the planning periods. While rural households were keen on acquiring farm assets, the portfolio of urban households constituted consumer durables, gold, jewellery and house property.Despite the fact that the household savings have been gradually moving from physical assets to financial assets over the years, still 49.79% of household savings are wrapped in unproductive physical assets, which is a cause of concern as the share of physical assets to total savings are very high in the recent years compared to emerging economies. This trend needs to be arrested as scarce funds are being diverted into unproductive segments. Of course, investment in Real estate sector can be treated as productive provided construction activity is commenced within reasonable time, but it is regrettably note that many investors just buy and hold it for speculation leading to unproductive investments. India has probably the largest fascination with gold than any other country in the world with a share of 9.50% of the world's total gold holdings. The World Gold Council believes that they are over 18000 tonnes of gold holding in the country. More impressive is the fact that current demand from India alone consumes 25% of the world's annual gold output. Large amount of capital is blocked in gold which resides in bank lockers and remain unproductive. Indian economy would grow faster if the capital markets could attract more of the nation's savings and channel them into more productive areas, especially infrastructure. If the Indian market can develop and evolve into a more mature financial system, which persuades the middle class to put more of its money into equities, the potential is

mind-boggling.

Which of the following statement (s) is/are correct in the context of the given passage? I. The GDS percentage to GDP has shown considerable improvement from 10% in 1950 to 33.7% in 2010, which is one of the highest globally. II. The saving rate however shows an increasing trend, marginal decline is observed under tic use hold sector. III. The share of financial assets in total household savings have come down from 54.05% to 21% especially in post reform era....

MCQ-> Read the following passage carefully and answer the questions given below it. Certain words/phrases have been printed in bold to help you locate them while answering some of the questions. The past quarter of a century has seen several bursts of selling by the world’s governments, mostly but not always in benign market conditions. Those in the OECD, a rich-country club, divested plenty of stuff in the 20 years before the global financial crisis. The first privatisation wave, which built up from the mid-1980s and peaked in 2000, was largely European. The drive to cut state intervention under Margaret Thatcher in Britain soon spread to the continent. The movement gathered pace after 1991, when eastern Europe put thousands of rusting state-owned enterprises (SOEs) on the block. A second wave came in the mid-2000s, as European economies sought to cash in on buoyant markets. But activity in OECD countries slowed sharply as the financial crisis began. In fact, it reversed. Bailouts of failing banks and companies have contributed to a dramatic increase in government purchases of corporate equity during the past five years. A more lasting fea ture is the expansion of the state capitalism practised by China and other emerging economic powers. Governments have actually bought more equity than they have sold in most years since 2007, though sales far exceeded purchases in 2013. Today privatisation is once again “alive and well”, says William Megginson of the Michael Price College of Business at the University of Oklahoma. According to a global tally he recently completed, 2012 was the third-best year ever, and preliminary evidence suggests that 2013 may have been better. However, the geography of sell-offs has changed, with emerging markets now to the fore. China, for instance, has been selling minority stakes in banking, energy, engineering and broadcasting; Brazil is selling airports to help finance a $20 billion investment programme. Eleven of the 20 largest IPOs between 2005 and 2013 were sales of minority stakes by SOEs, mostly in developing countries. By contrast, state-owned assets are now “the forgotten side of the balance-sheet” in many advanced economies, says Dag Detter, managing partner of Whetstone Solutions, an adviser to governments on asset restructuring. They shouldn’t be. Governments of OECD countries still oversee vast piles of assets, from banks and utilities to buildings, land and the riches beneath (see table). Selling some of these holdings could work wonders: reduce debt, finance infrastructure, boost economic efficiency. But governments often barely grasp the value locked up in them. The picture is clearest for companies or company-like entities held by central governments. According to data compiled by the OECD and published on its website, its 34 member countries had 2,111 fully or majority-owned SOEs, with 5.9m employees, at the end of 2012. Their combined value (allowing for some but not all pension-fund liabilities) is estimated at $2.2 trillion, roughly the same size as the global hedge-fund industry. Most are in network industries such as telecoms, electricity and transport. In addition, many countries have large minority stakes in listed firms. Those in which they hold a stake of between 10% and 50% have a combined market value of $890 billion and employ 2.9m people. The data are far from perfect. The quality of reporting varies widely, as do definitions of what counts as a state-owned company: most include only centralgovernment holdings. If all assets held at sub-national level, such as local water companies, were included, the total value could be more than $4 trillion. Reckons Hans Christiansen, an OECD economist. Moreover, his team has had to extrapolate because some QECD members, including America and Japan, provide patchy data. America is apparently so queasy about discussions of public ownership of -commercial assets that the Treasury takes no part in the OECD’s working group on the issue, even though it has vast holdings, from Amtrak and the 520,000-employee Postal Service to power generators and airports. The club’s efforts to calculate the value that SOEs add to, or subtract from, economies were abandoned after several countries, including America, refused to co-operate. Privatisation has begun picking up again recently in the OECD for a variety of reasons. Britain’s Conservative-led coalition is fbcused on (some would say obsessed with) reducing the public debt-to-GDP ratio. Having recently sold the Royal Mail through a public offering, it is hoping to offload other assets, including its stake in URENCO, a uranium enricher, and its student-loan portfolio. From January 8th, under a new Treasury scheme, members of the public and businesses will be allowed to buy government land and buildings on the open market. A website will shortly be set up to help potential buyers see which bits of the government’s /..337 billion-worth of holdings ($527 billion at today’s rate, accounting for 40% of developable sites round Britain) might be surplus. The government, said the chief treasury secretary, Danny Alexander, “should not act as some kind of compulsive hoarder”. Japan has different reasons to revive sell-offs, such as to finance reconstruction after its devastating earthquake and tsunami in 2011. Eyes are once again turning to Japan Post, a giant postal-to-financial-services conglomerate whose oftpostponed partial sale could at last happen in 2015 and raise (Yen) 4 trillion ($40 billion) or more. Australia wants to sell financial, postal and aviation assets to offset the fall in revenues caused by the commodities slowdown. In almost all the countries of Europe, privatisation is likely “to surprise on the upside” as long as markets continue to mend, reckons Mr Megginson. Mr Christiansen expects to see three main areas of activity in coming years. First will be the resumption of partial sell-offs in industries such as telecoms, transport and utilities. Many residual stakes in partly privatised firms could be sold down further. France, for instance, still has hefty stakes in GDF SUEZ, Renault, Thales and Orange. The government of Francois Hollande may be ideologically opposed to privatisation, but it is hoping to reduce industrial stakes to raise funds for livelier sectors, such as broadband and health. The second area of growth should be in eastern Europe, where hundreds of large firms, including manufacturers, remain in state hands. Poland will sell down its stakes in listed firms to make up for an expected reduction in EU structural funds. And the third area is the reprivatisation of financial institutions rescued during the crisis. This process is under way: the largest privatisation in 2012 was the $18 billion offering of America’s residual stake in AIG, an insurance company.Which of the following statements is not true in the context of the given passage ?

...

MCQ-> In the following questions, read the following passage carefully and answer the questions given below it. Certain words/phrases are given in bold to help you locate them while answering some of the questions. Over the past few days alone. the China’s central bank has pumped extra cash into the financial system and cut interest rates. The aim is to free more cash for banks to lend and provide a boost for banks seeking to improve the return on their assets. The official data though, suggested that bad loans make up only 1.4% of their balance sheets. How to explain the discrepancy? One possible answer is that bad loans are a tagging indicator i.e. it is only after the economy has struggled for while that borrowers began to suffer. Looked at this way, China is trying to anticipate problems keeping its banks in good health by susteining economic growth of nearly 7% year on year. Another more worrying possibility is that bad loans are worse than official data indicate. This does not look to be the cause for China’s biggest banks, which are managed conservatively and largely focus on the county’s biggest value and quality borrowers. But there is mounting evidence that when it comes to smaller banks, especially those yet to list on the stock market, bad loans piling up. That is important because unlisted lenders account for just over a third of the Chinese banking sector, making them as big as Japan’s entire banking industry. Although, non-performing loans have edged up slowly, the increase in specialmention loans (a category that includes those overdue but not yet classified as impaired loans.) has been much bigger. Special-mention loans are about 2% at most of China’s big listed banks, suggesting that such loans must be much higher at their smaller, unlisted peers. Many of these loans are simple bad debts which banks have not yet admitted to. Another troubling fact is that fifteen years ago, the government created asset-management companies (often referred to as badbanks) to take on the non-performing loans of the lenders. After the initial transfer these companies had little to pay. But, last year, Cinda, the biggest of the bad banks, bought nearly 150 billion Yuan ($24 billion) of distressed assets last year, two-thirds more than in 2013. These assets would have raised the banks badloans ratio by a few tenths of a percentage point. Although such numbers do not seem very alarming, experts who reviewed last year’s results for 158 banks, of which only 20 are listed found that “shadow loans”, loans recorded as investments which may be a disguise for bad loans have grown to as much as 5.7 billion Yuan, or 5 of the industry’s assets. These are heavily concentrated on the balance sheets of smaller-unlisted banks, and at the very least, all this points to a need for recapitalisation of small banks.Choose the word which is most nearly the same in meaning to the word ‘TAGGING’ given in bold as used in the passage....

MCQ->

Read the passage carefully and answer the questions given

. . . “Everybody pretty much agrees that the relationship between elephants and people has dramatically changed,” [says psychologist Gay] Bradshaw. . . . “Where for centuries humans and elephants lived in relatively peaceful coexistence, there is now hostility and violence. Now, I use the term ‘violence’ because of the intentionality associated with it, both in the aggression of humans and, at times, the recently observed behavior of elephants.” . . .Typically, elephant researchers have cited, as a cause of aggression, the high levels of testosterone in newly matured male elephants or the competition for land and resources between elephants and humans. But. . . Bradshaw and several colleagues argue. . . that today’s elephant populations are suffering from a form of chronic stress, a kind of species-wide trauma. Decades of poaching and culling and habitat loss, they claim, have so disrupted the intricate web of familial and societal relations by which young elephants have traditionally been raised in the wild, and by which established elephant herds are governed, that what we are now witnessing is nothing less than a precipitous collapse of elephant culture. . . .Elephants, when left to their own devices, are profoundly social creatures. . . . Young elephants are raised within an extended, multitiered network of doting female caregivers that includes the birth mother, grandmothers, aunts and friends. These relations are maintained over a life span as long as 70 years. Studies of established herds have shown that young elephants stay within 15 feet of their mothers for nearly all of their first eight years of life, after which young females are socialized into the matriarchal network, while young males go off for a time into an all-male social group before coming back into the fold as mature adults. . . .This fabric of elephant society, Bradshaw and her colleagues [demonstrate], ha[s] effectively been frayed by years of habitat loss and poaching, along with systematic culling by government agencies to control elephant numbers and translocations of herds to different habitats. . . . As a result of such social upheaval, calves are now being born to and raised by ever younger and inexperienced mothers. Young orphaned elephants, meanwhile, that have witnessed the death of a parent at the hands of poachers are coming of age in the absence of the support system that defines traditional elephant life. “The loss of elephant elders,” [says] Bradshaw . . . "and the traumatic experience of witnessing the massacres of their family, impairs normal brain and behavior development in young elephants.”What Bradshaw and her colleagues describe would seem to be an extreme form of anthropocentric conjecture if the evidence that they’ve compiled from various elephant researchers. . . weren’t so compelling. The elephants of decimated herds, especially orphans who’ve watched the death of their parents and elders from poaching and culling, exhibit behavior typically associated with post-traumatic stress disorder and other trauma-related disorders in humans: abnormal startle response, unpredictable asocial behavior, inattentive mothering and hyperaggression. . . .[According to Bradshaw], “Elephants are suffering and behaving in the same ways that we recognize in ourselves as a result of violence. . . . Except perhaps for a few specific features, brain organization and early development of elephants and humans are extremely similar.”Which of the following statements best expresses the overall argument of this passage?

...

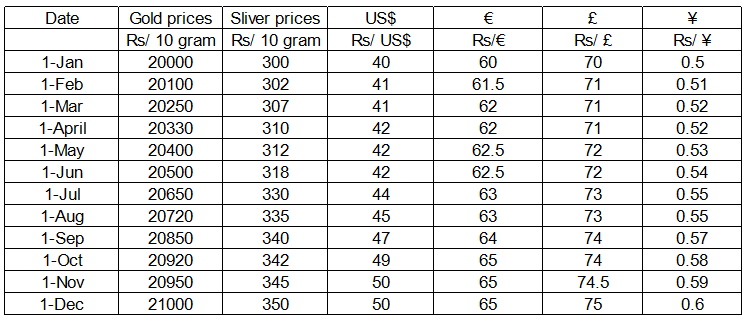

MCQ-> answer questions based on the following information:In the beginning of the year 2010, Mr. Sanyal had the option to invest Rs. 800000 in one or more of the following assets – gold, silver, US bonds, EU bonds, UK bonds and Japanese bonds. In order to invest in US bonds, one must first convert his investible fund into US Dollars at the ongoing exchange rate. Similarly, if one wants to invest in EU bonds or UK bonds or Japanese bonds one must first convert his investible fund into Euro, British Pounds and Japanese Yen respectively at the ongoing exchange rates. Transactions were allowed only in the beginning of every month. Bullion prices and exchange rates were fixed at the beginning of every month and remained unchanged throughout the month. Refer to the table titled “Bullion Prices and Exchange Rates in 2010" for the relevant data.

Bullion Prices and Exchange Rates in 2010

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

...

×

×

Type The Issue

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?