1. A Grade I officer who retired from service on 31-3-2009 wants to accept a commercial employment as 1-05-2012, sanction is to be obtained from:-

Answer: No sanction is required.

Tags

Show Similar Question And Answers

Powered By:Omega Web Solutions

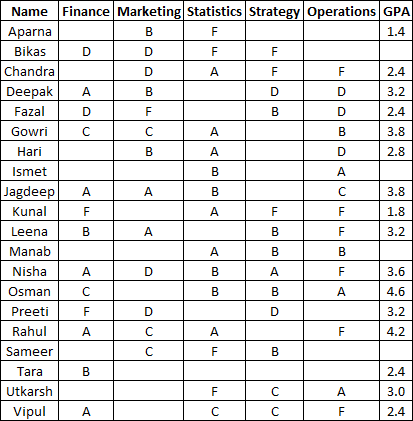

Powered By:Omega Web Solutions In the grading system, A, B, C, D, and F grades fetch 6, 4, 3, 2, and 0 grade points respectively. The Grade Point Average (GPA) is the arithmetic mean of the grade points obtained in the five subjects. For example Nisha’s GPA is (6 + 2 + 4 + 6 + 0) / 5 = 3.6. Some additional facts are also known about the students’ grades. These are(i) Vipul obtained the same grade in Marketing as Aparna obtained in Finance and Strategy.(ii) Fazal obtained the same grade in Strategy as Utkarsh did in Marketing.(iii) Tara received the same grade in exactly three courses.What grade did Preeti obtain in Statistics?

In the grading system, A, B, C, D, and F grades fetch 6, 4, 3, 2, and 0 grade points respectively. The Grade Point Average (GPA) is the arithmetic mean of the grade points obtained in the five subjects. For example Nisha’s GPA is (6 + 2 + 4 + 6 + 0) / 5 = 3.6. Some additional facts are also known about the students’ grades. These are(i) Vipul obtained the same grade in Marketing as Aparna obtained in Finance and Strategy.(ii) Fazal obtained the same grade in Strategy as Utkarsh did in Marketing.(iii) Tara received the same grade in exactly three courses.What grade did Preeti obtain in Statistics?