Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. Balance sheet shows:

(A): Dynamic financial position

(B): Fund flow position

(C): Static financial position

(D): None of these

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->Balance sheet shows:....

QA->An accounting system which presents the Balance sheet into two parts is called:....

QA->The horizontal and vertical lines on a work sheet are called?....

QA->How a draft is written or type written in on sheet leaving margin?....

QA->Area of A0 trimmed size drawing sheet is :....

MCQ->Ten new television shows appeared during the month of September. Five of the shows were sitcoms, three were hour-long dramas, and two were news-magazine shows. By January, only seven of these new shows were still on the air. Five of the shows that remained were sitcoms.....

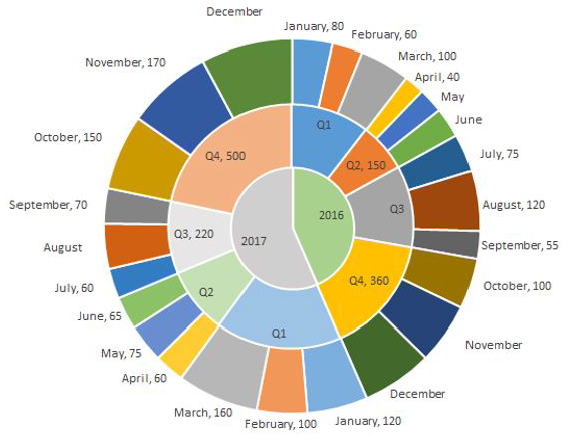

MCQ-> The multi-layered pie-chart below shows the sales of LED television sets for a big retail electronics outlet during 2016 and 2017. The outer layer shows the monthly sales during this period, with each label showing the month followed by sales figure of that month. For some months, the sales figures are not given in the chart. The middle-layer shows quarterwise aggregate sales figures (in some cases, aggregate quarter-wise sales numbers are not given next to the quarter). The innermost layer shows annual sales. It is known that the sales figures during the three months of the second quarter (April, May, June) of 2016 form an arithmetic progression, as do the three monthly sales figures in the fourth quarter (October, November, December) of that year.

What is the percentage increase in sales in December 2017 as compared to the sales in December 2016?

....

MCQ->Assertion (A) : Balance of payment always balance. Reason (R) : Debit (payments) must always equal credits (receipts) in balance of payment account.....

MCQ-> Crinoline and croquet are out. As yet, no political activists have thrown themselves in front of the royal horse on Derby Day. Even so, some historians can spot the parallels. It is a time of rapid technological change. It is a period when the dominance of the world’s superpower is coming under threat. It is an epoch when prosperity masks underlying economic strain. And, crucially, it is a time when policy-makers are confident that all is for the best in the best of all possible worlds. Welcome to the Edwardian Summer of the second age of globalisation. Spare a moment to take stock of what’s been happening in the past few months. Let’s start with the oil price, which has rocketed to more than $65 a barrel, more than double its level 18 months ago. The accepted wisdom is that we shouldn’t worry our little heads about that, because the incentives are there for business to build new production and refining capacity, which will effortlessly bring demand and supply back into balance and bring crude prices back to $25 a barrel. As Tommy Cooper used to say, ‘just like that’. Then there is the result of the French referendum on the European Constitution, seen as thick-headed luddites railing vainly against the modern world. What the French needed to realise, the argument went, was that there was no alternative to the reforms that would make the country more flexible, more competitive, more dynamic. Just the sort of reforms that allowed Gate Gourmet to sack hundreds of its staff at Heathrow after the sort of ultimatum that used to be handed out by Victorian mill owners. An alternative way of looking at the French “non” is that our neighbours translate “flexibility” as “you’re fired”. Finally, take a squint at the United States. Just like Britain a century ago, a period of unquestioned superiority is drawing to a close. China is still a long way from matching America’s wealth, but it is growing at a stupendous rate and economic strength brings geo-political clout. Already, there is evidence of a new scramble for Africa as Washington and Beijing compete for oil stocks. Moreover, beneath the surface of the US economy, all is not well. Growth looks healthy enough, but the competition from China and elsewhere has meant the world’s biggest economy now imports far more than it exports. The US is living beyond its means, but in this time of studied complacency a current account deficit worth 6 percent of gross domestic product is seen as a sign of strength, not weakness. In this new Edwardian summer, comfort is taken from the fact that dearer oil has not had the savage inflationary consequences of 1973-74, when a fourfold increase in the cost of crude brought an abrupt end to a postwar boom that had gone on uninterrupted for a quarter of a century. True, the cost of living has been affected by higher transport costs, but we are talking of inflation at b)3 per cent and not 27 per cent. Yet the idea that higher oil prices are of little consequence is fanciful. If people are paying more to fill up their cars it leaves them with less to spend on everything else, but there is a reluctance to consume less. In the 1970s unions were strong and able to negotiate large, compensatory pay deals that served to intensify inflationary pressure. In 2005, that avenue is pretty much closed off, but the abolition of all the controls on credit that existed in the 1970s means that households are invited to borrow more rather than consume less. The knock-on effects of higher oil prices are thus felt in different ways – through high levels of indebtedness, in inflated asset prices, and in balance of payments deficits.There are those who point out, rightly, that modern industrial capitalism has proved mightily resilient these past 250 years, and that a sign of the enduring strength of the system has been the way it apparently shrugged off everything – a stock market crash, 9/11, rising oil prices – that have been thrown at it in the half decade since the millennium. Even so, there are at least three reasons for concern. First, we have been here before. In terms of political economy, the first era of globalisation mirrored our own. There was a belief in unfettered capital flows, in free trade, and in the power of the market. It was a time of massive income inequality and unprecedented migration. Eventually, though, there was a backlash, manifested in a struggle between free traders and protectionists, and in rising labour militancy. Second, the world is traditionally at its most fragile at times when the global balance of power is in flux. By the end of the nineteenth century, Britain’s role as the hegemonic power was being challenged by the rise of the United States, Germany, and Japan while the Ottoman and Hapsburg empires were clearly in rapid decline. Looking ahead from 2005, it is clear that over the next two or three decades, both China and India – which together account for half the world’s population – will flex their muscles. Finally, there is the question of what rising oil prices tell us. The emergence of China and India means global demand for crude is likely to remain high at a time when experts say production is about to top out. If supply constraints start to bite, any declines in the price are likely to be short-term cyclical affairs punctuating a long upward trend.By the expression ‘Edwardian Summer’, the author refers to a period in which there is

....

MCQ->Exports and imports, a swelling favourable balance of trade, investments and bank-balances, are not an index or a balance sheet of national prosperity. Till the beginning of the Second World War, English exports were noticeably greater than what they are today. And yet England has greater national prosperity today than it ever had. Because the income of average Englishmen, working as field and factory labourers, clerks, policemen, petty shopkeepers and shop assistants, domestic workers and other low-paid workers, has gone up. The passage best supports the statement that:....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions What is the percentage increase in sales in December 2017 as compared to the sales in December 2016?

What is the percentage increase in sales in December 2017 as compared to the sales in December 2016?