Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. A material may fail if

(A): maximum principal stress exceeds the direct stress σ0

(B): maximum strain exceeds

(C): maximum shear stress exceeds

(D): total strain energy exceeds

(E): all the above.

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->If P1 can fail 50% of the times and P2, 40% of the times, P can fail -----------of the times.....

QA->If a material; placed in a magnetic field is thrown out of it; then how is the material?....

QA->If a material, placed in a magnetic field is thrown out of it, then how is the material?....

QA->Atal Behari Vajpayee becomes PrimeMinister on May 16 and resigns on May 28....

QA->India’s second (May 11) and third (May 13) nuclear explosion at Pokhran.....

MCQ-> Read the following passage carefully and answer the questions given below it. Certain words/phrases have been printed in bold tohelp you locate them while answering some of the questions. During the last few years, a lot of hype has been heaped on the BRICS (Brazil, Russia, India, China, and South Africa). With their large populations and rapid growth, these countries, so the argument goes, will soon become some of the largest economies in the world and, in the case of China, the largest of all by as early as 2020. But the BRICS, as well as many other emerging-market economieshave recently experienced a sharp economic slowdown. So, is the honeymoon over? Brazil’s GDP grew by only 1% last year, and may not grow by more than 2% this year, with its potential growth barely above 3%. Russia’s economy may grow by barely 2% this year, with potential growth also at around 3%, despite oil prices being around $100 a barrel. India had a couple of years of strong growth recently (11.2% in 2010 and 7.7% in 2011) but slowed to 4% in 2012. China’s economy grew by 10% a year for the last three decades, but slowed to 7.8% last year and risks a hard landing. And South Africa grew by only 2.5% last year and may not grow faster than 2% this year. Many other previously fast-growing emerging-market economies – for example, Turkey, Argentina, Poland, Hungary, and many in Central and Eastern Europe are experiencing a similar slowdown. So, what is ailing the BRICS and other emerging markets? First, most emerging-market economies were overheating in 2010-2011, with growth above potential and inflation rising and exceeding targets. Many of them thus tightened monetary policy in 2011, with consequences for growth in 2012 that have carried over into this year. Second, the idea that emerging-market economies could fully decouple from economic weakness in advanced economies was

farfetched

: recession in the eurozone, near-recession in the United Kingdom and Japan in 2011-2012, and slow economic growth in the United States were always likely to affect emerging market performance negatively – via trade, financial links, and investor confidence. For example, the ongoing euro zone downturn has hurt Turkey and emergingmarket economies in Central and Eastern Europe, owing to trade links. Third, most BRICS and a few other emerging markets have moved toward a variant of state capitalism. This implies a slowdown in reforms that increase the private sector’s productivity and economic share, together with a greater economic role for state-owned enterprises (and for state-owned banks in the allocation of credit and savings), as well as resource nationalism, trade protectionism, import substitution industrialization policies, and imposition of capital controls. This approach may have worked at earlier stages of development and when the global financial crisis caused private spending to fall; but it is now distorting economic activity and depressing potential growth. Indeed, China’s slowdown reflects an economic model that is, as former Premier Wen Jiabao put it, “unstable, unbalanced, uncoordinated, and unsustainable,” and that now is adversely affecting growth in emerging Asia and in commodity-exporting emerging markets from Asia to Latin America and Africa. The risk that China will experience a hard landing in the next two years may further hurt many emerging economies. Fourth, the commodity super-cycle that helped Brazil, Russia, South Africa, and many other commodity-exporting emerging markets may be over. Indeed, a boom would be difficult to sustain, given China’s slowdown, higher investment in energysaving technologies, less emphasis on capital-and resource-oriented growth models around the world, and the delayed increase in supply that high prices induced. The fifth, and most recent, factor is the US Federal Reserve’s signals that it might end its policy of quantitative easing earlier than expected, and its hints of an even tual exit from zero interest rates. both of which have caused turbulence in emerging economies’ financial markets. Even before the Fed’s signals, emergingmarket equities and commodities had underperformed this year, owing to China’s slowdown. Since then, emerging-market currencies and fixed-income securities (government and corporate bonds) have taken a hit. The era of cheap or zerointerest money that led to a wall of liquidity chasing high yields and assets equities, bonds, currencies, and commodities – in emerging markets is drawing to a close. Finally, while many emerging-market economies tend to run current-account surpluses, a growing number of them – including Turkey, South Africa, Brazil, and India – are running deficits. And these deficits are now being financed in riskier ways: more debt than equity; more short-term debt than longterm debt; more foreign-currency debt than local-currency debt; and more financing from fickle cross-border interbank flows. These countries share other weaknesses as well: excessive fiscal deficits, abovetarget inflation, and stability risk (reflected not only in the recent political turmoil in Brazil and Turkey, but also in South Africa’s labour strife and India’s political and electoral uncertainties). The need to finance the external deficit and to avoid excessive depreciation (and even higher inflation) calls for raising policy rates or keeping them on hold at high levels. But monetary tightening would weaken already-slow growth. Thus, emerging economies with large twin deficits and other macroeconomic fragilities may experience further downward pressure on their financial markets and growth rates. These factors explain why growth in most BRICS and many other emerging markets has slowed sharply. Some factors are cyclical, but others – state capitalism, the risk of a hard landing in China, the end of the commodity supercycle -are more structural. Thus, many emerging markets’ growth rates in the next decade may be lower than in the last – as may the outsize returns that investors realised from these economies’ financial assets (currencies, equities. bonds, and commodities). Of course, some of the better-managed emerging-market economies will continue to experitnce rapid growth and asset outperformance. But many of the BRICS, along with some other emerging economies, may hit a thick wall, with growth and financial markets taking a serious beating.Which of the following statement(s) is/are true as per the given information in the passage ? A. Brazil’s GDP grew by only 1% last year, and is expected to grow by approximately 2% this year. B. China’s economy grew by 10% a year for the last three decades but slowed to 7.8% last year. C. BRICS is a group of nations — Barzil, Russia, India China and South Africa.....

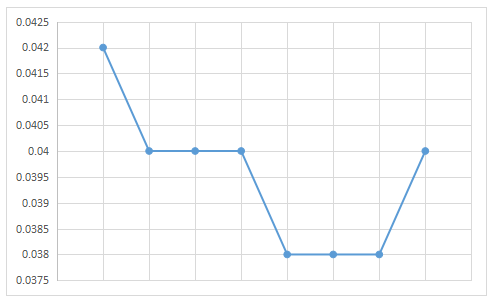

MCQ->The estimated material cost given in the table titled “Variable Cost Estimates of Mulchand Textiles” included the cost of material that gets spoiled in the production process. Mr. Sharma decomposed the estimated material cost into material spoilage cost and material usage cost, but he lost the data when his computer crashed. When he saw the following line diagram, here called that he measured the estimate of material spoilage cost per square feet of output on the y - axis and monthly output on the x - axis.

Estimated material usage cost per square feet of output.....

MCQ-> Read the following passage carefully and answer the questions given.Do you ever feel there’s is a greater being inside of you bursting to get out? It is the voice that encourages you to really make something of your life. When you act congruently with that voice, it’s like your are a whole new person. You are bold and courageous. You are strong. You are unstoppable. But, then reality sets in, and soon those moments are history. It is not hard to put youself temporarily into an emotionally motivated state. Just listen to that motivational song for that matter. However, this motivation does not stay forever. Your great ideas seem impractical. How many times have you been temporarily inspired with a idea like, “I want to start my own business.” And then a week later it’s forgotten? You come up with inspiring ideas when you are motivated. But you fail to maintain that motivation through the action phase.The problem we ask ourselves is, why does this happen? You can listen to hundereds of motivational speakers and experience an emotional yo-yo effect, but it does not fast. The problem is that as we are intellectually guided, we try to find logic in emotional motivation and as we fail to find logic

eventually phases out

. I used to get frustrated when my emotional motivation fizzled out after a while. Eventually, I realised that being guided by intellect, was not such a bad thing after all. I just had to learn to use my mind as an effective motivational tool. I figured that if I was not feeling motivated to go after a particular goal, may be there was a logical reason for it. I noted that when I had strong intellectual reasons for doing something. I usually did not have trouble taking action.But when my mind thinks a goal is wrong on some level. I usually feel blocked. I eventually realised that this was my mind’s way of telling me the goal was a mistake to begin with. Sometimes a goal seem to make sense on one level but when you look further upstream, it becomes clear that the goal is ill advised. Suppose you work in sales, and you get a goal to increase your income by 20% by becoming a more effective salesperson. That seems like a reasonable and intelligent goal. But may be you are surprised to find yourself encountering all sorts of internal blocks when you try to pursue it. You should feel motivated, but you just don’t. The problem may be that on a deeper level your mind knows you don’t want to be working in sales at all. You really want to be a musician. Matter how hard you push yourself in sales career, it will always be a motivational dead end.Further when you set goals, that are too small and too

timid

, you suffer a perpetual lack of motivation. You just need to summon the courage to acknowledge your true desires. Then you will have to deal with the self-doubt and fear that’s been making you think too small. Ironically, the real key to motivation is to set the goals that scare you. You are letting fears, excuses and limiting beliefs hold you back. Your subconscious mind knows you are strong, so it won’t provide any motivational fuel until. You step up, face your fears, and acknowledge your hearts desire. Once you finally decide to face your tears and drop the excuses, then you will find your motivation turning on full blast.What does the author want to convey when he says, “When you look further upstream, it becomes clear that the goal is ill advised.”?

....

MCQ-> Read the following passage carefully and answer the questions given below it. Certain words have been printed in bold to help you locate them while answering some of the question. Political

ploys

initially hailed as master-strokes often end up as flops. The Rs. 60,000 crore farm loan waiver announced in the budget writes off 100% of overdues of small and marginal farmers holding upto two hectares, and 25% of overdues of larger farmers. While India has enjoyed 8%-9% GDP growth for the past few years, the boom has bypassed many rural areas and farmer distress and suicides have made newspaper headlines. Various attempts to provide relief (employment guarantee scheme, public distribution system) have made little impact, thanks. to huge leakages from the government’s lousy delivery systems. So, many economists think the loan waiver is a worthwhile alternative to provide relief. However the poorest rural folk are landless labourers, who get neither farm loans nor waivers. Half of the small and marginal farmers get no loans from banks and depend entirely on money-lenders, and will not benefit. Besides, rural India is full of the family holdings rather than individual holdings and family holdings will typically be much larger than two hectares even for dirt-poor farmers, who will, therefore, be denied the 100% waiver. It will thus fail in both economic and political objectives. IRDP loans to the rural poor in the 1980s demonstrated that crooked bank officials demand bribes amounting to one-third the intended benefits. Very few of the intended beneficiaries who

merited

relief received it. After the last farm loan waiver will Similarly slow down fresh loans to deserving farmers. While overdues to cooperatives may be higher, economist Surjit Shalla says less than 5% of farmer loans to banks are overdue i.e. overdues exist for only 2.25 million out of 90 million farmers. If so, then the 95% who have repaid loans will not benefit. They will be angry at being penalised for honesty. The budget thus grossly overestimates the number of beneficiaries, It also underestimates the negative effects of the waiver-encouraging willful default in the future and discouraging fresh bank lending for some years. nstead of trying to reach the needy, through a

plethora

of leaky schemes we should transfer cash directly to the needy using new technology like biometric smart cards, which are now being used in many countries, and mobile phones bank accounts. Then benefits can go directly to phone accounts operable only by those with biometric cards, ending the massive leakages of current schemes. The political benefits of the loan waiver have also been exaggerated since if only a small fraction of farm families benefit, and many of these have to pay bribes to get the actual benefit, will the waiver really be a massive vote- winner? Members of joint families will feel

aggrieved

that, despite having less than one hectare per head, their family holding is too large. Lo qualify for the 100% waiver. Alliance ministers, of central or state governments, give away freebies in their last budgets, hoping to win electoral regards, Yet, four-fifth of all

incumbent

governments are voted out. This shows that beneficiaries of favours are not notably grateful, while those not so favoured may feel aggrieved, and vote for the opposition. That seems to be why election budgets constantly fail to win elections in India and the loan waiver will not change that pattern.Why do economists feel that loan waivers will benefit farmers in distress?

....

MCQ-> Read carefully the four passages that follow and answer the questions given at the end of each passage:PASSAGE I The most important task is revitalizing the institution of independent directors. The independent directors of a company should be faithful fiduciaries protecting, the long-term interests of shareholders while ensuring fairness to employees, investor, customer, regulators, the government of the land and society. Unfortunately, very often, directors are chosen based of friendship and, sadly, pliability. Today, unfortunately, in the majority of cases, independence is only true on paper.The need of the hour is to strengthen the independence of the board. We have to put in place stringent standards for the independence of directors. The board should adopt global standards for director-independence, and should disclose how each independent director meets these standards. It is desirable to have a comprehensive report showing the names of the company employees of fellow board members who are related to each director on the board. This report should accompany the annual report of all listed companies. Another important step is to regularly assess the board members for performance. The assessment should focus on issues like competence, preparation, participation and contribution. Ideally, this evaluation should be performed by a third party. Underperforming directors should be allowed to leave at the end of their term in a gentle manner so that they do not lose face. Rather than being the rubber stamp of a company’s management policies, the board should become a true active partner of the management. For this, independent directors should be trained in their in their in roles and responsibilities. Independent directors should be trained on the business model and risk model of the company, on the governance practices, and the responsibilities of various committees of the board of the company. The board members should interact frequently with executives to understand operational issues. As part of the board meeting agenda, the independent directors should have a meeting among themselves without the management being present. The independent board members should periodically review the performance of the company’s CEO, the internal directors and the senior management. This has to be based on clearly defined objective criteria, and these criteria should be known to the CEO and other executive directors well before the start of the evolution period. Moreover, there should be a clearly laid down procedure for communicating the board’s review to the CEO and his/her team of executive directors. Managerial remuneration should be based on such reviews. Additionally, senior management compensation should be determined by the board in a manner that is fair to all stakeholders. We have to look at three important criteria in deciding managerial remuneration-fairness accountability and transparency. Fairness of compensation is determined by how employees and investors react to the compensation of the CEO. Accountability is enhanced by splitting the total compensation into a small fixed component and a large variable component. In other words, the CEO, other executive directors and the senior management should rise or fall with the fortunes of the company. The variable component should be linked to achieving the long-term objectives of the firm. Senior management compensation should be reviewed by the compensation committee of the board consisting of only the independent directors. This should be approved by the shareholders. It is important that no member of the internal management has a say in the compensation of the CEO, the internal board members or the senior management. The SEBI regulations and the CII code of conduct have been very helpful in enhancing the level of accountability of independent directors. The independent directors should decide voluntarily how they want to contribute to the company. Their performance should decide voluntarily how they want to contribute to the company. Their performance should be appraised through a peer evaluation process. Ideally, the compensation committee should decide on the compensation of each independent director based on such a performance appraisal. Auditing is another major area that needs reforms for effective corporate governance. An audit is the Independent examination of financial transactions of any entity to provide assurance to shareholder and other stakeholders that the financial statements are free of material misstatement. Auditors are qualified professionals appointed by the shareholders to report on the reliability of financial statements prepared by the management. Financial markets look to the auditor’s report for an independent opinion on the financial and risk situation of a company. We have to separate such auditing form other services. For a truly independent opinion, the auditing firm should not provide services that are perceived to be materially in conflict with the role of the auditor. These include investigations, consulting advice, sub contraction of operational activities normally undertaken by the management, due diligence on potential acquisitions or investments, advice on deal structuring, designing/implementing IT systems, bookkeeping, valuations and executive recruitment. Any departure from this practice should be approved by the audit committee in advance. Further, information on any such exceptions must be disclosed in the company’s quarterly and annual reports. To ensure the integrity of the audit team, it is desirable to rotate auditor partners. The lead audit partner and the audit partner responsible for reviewing a company’s audit must be rotated at least once every three to five years. This eliminates the possibility of the lead auditor and the company management getting into the kind of close, cozy relationship that results in lower objectivity in audit opinions. Further, a registered auditor should not audit a chief accounting office was associated with the auditing firm. It is best that members of the audit teams are prohibited from taking up employment in the audited corporations for at least a year after they have stopped being members of the audit team.A competent audit committee is essential to effectively oversee the financial accounting and reporting process. Hence, each member of the audit committee must be ‘financially literate’, further, at least one member of the audit committee, preferably the chairman, should be a financial expert-a person who has an understanding of financial statements and accounting rules, and has experience in auditing. The audit committee should establish procedures for the treatment of complaints received through anonymous submission by employees and whistleblowers. These complaints may be regarding questionable accounting or auditing issues, any harassment to an employee or any unethical practice in the company. The whistleblowers must be protected. Any related-party transaction should require prior approval by the audit committee, the full board and the shareholders if it is material. Related parties are those that are able to control or exercise significant influence. These include; parent- subsidiary relationships; entities under common control; individuals who, through ownership, have significant influence over the enterprise and close members of their families; and dey management personnel.Accounting standards provide a framework for preparation and presentation of financial statements and assist auditors in forming an opinion on the financial statements. However, today, accounting standards are issued by bodies comprising primarily of accountants. Therefore, accounting standards do not always keep pace with changes in the business environment. Hence, the accounting standards-setting body should include members drawn from the industry, the profession and regulatory bodies. This body should be independently funded. Currently, an independent oversight of the accounting profession does not exist. Hence, an independent body should be constituted to oversee the functioning of auditors for Independence, the quality of audit and professional competence. This body should comprise a "majority of non- practicing accountants to ensure independent oversight. To avoid any bias, the chairman of this body should not have practiced as an accountant during the preceding five years. Auditors of all public companies must register with this body. It should enforce compliance with the laws by auditors and should mandate that auditors must maintain audit working papers for at least seven years.To ensure the materiality of information, the CEO and CFO of the company should certify annual and quarterly reports. They should certify that the information in the reports fairly presents the financial condition and results of operations of the company, and that all material facts have been disclosed. Further, CEOs and CFOs should certify that they have established internal controls to ensure that all information relating to the operations of the company is freely available to the auditors and the audit committee. They should also certify that they have evaluated the effectiveness of these controls within ninety days prior to the report. False certifications by the CEO and CFO should be subject to significant criminal penalties (fines and imprisonment, if willful and knowing). If a company is required to restate its reports due to material non-compliance with the laws, the CEO and CFO must face severe punishment including loss of job and forfeiting bonuses or equity-based compensation received during the twelve months following the filing.The problem with the independent directors has been that: I. Their selection has been based upon their compatibility with the company management II. There has been lack of proper training and development to improve their skill set III. Their independent views have often come in conflict with the views of company management. This has hindered the company’s decision-making process IV. Stringent standards for independent directors have been lacking....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Estimated material usage cost per square feet of output.....

Estimated material usage cost per square feet of output.....