Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. The purchase of shares and bonds of Indian companies by Foreign Institutional Investors is called

(A): Foreign Direct Investment

(B): Portfolio Investment

(C): NRI Investment

(D): Foreign Indirect Investment

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

SSC CGL 2011 Tier 1 - Shift 2

Show Similar Question And Answers

QA->Who heads the committee constituted by the Government of India, to look into the issue of Minimum Alternate tax (MAT) on Foreign Institutional Investors?....

QA->…………. is the authority empowered to accord Administrative Sanction for the purchase of items of stores exceeding Rs.10000 but below Rs.20000, other than those included in Appendix II of the Store purchase Rules:....

QA->As per the procurement guidelines what method of purchase should be adopted when a Grama Panchayat intends to purchase electrical goods for Rs.20000?....

QA->Which country has one of the highest percentages of companies where fraud, in particular corruption and bribery, was detected, according to a new survey of large local and multinational companies across industries worldwide?....

QA->RBI hasgiven banks the right to issue masala bonds in foreign markets, also known as....

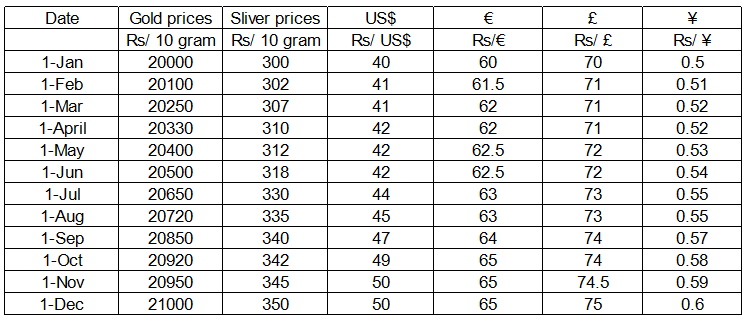

MCQ-> answer questions based on the following information:In the beginning of the year 2010, Mr. Sanyal had the option to invest Rs. 800000 in one or more of the following assets – gold, silver, US bonds, EU bonds, UK bonds and Japanese bonds. In order to invest in US bonds, one must first convert his investible fund into US Dollars at the ongoing exchange rate. Similarly, if one wants to invest in EU bonds or UK bonds or Japanese bonds one must first convert his investible fund into Euro, British Pounds and Japanese Yen respectively at the ongoing exchange rates. Transactions were allowed only in the beginning of every month. Bullion prices and exchange rates were fixed at the beginning of every month and remained unchanged throughout the month. Refer to the table titled “Bullion Prices and Exchange Rates in 2010" for the relevant data.

Bullion Prices and Exchange Rates in 2010

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

....

MCQ-> People are continually enticed by such "hot" performance, even if it lasts for brief periods. Because of this susceptibility, brokers or analysts who have had one or two stocks move up sharply, or technicians who call one turn correctly, are believed to have established a credible record and can readily find market followings. Likewise, an advisory service that is right for a brief time can beat its drums loudly. Elaine Garzarelli gained near immortality when she purportedly "called" the 1987 crash. Although, as the market strategist for Shearson Lehman, her forecast was never published in a research report, nor indeed communicated to its clients, she still received widespread recognition and publicity for this call, which was made in a short TV interview on CNBC. Still, her remark on CNBC that the Dow could drop sharply from its then 5300 level rocked an already nervous market on July 23, 1996. What had been a 40-point gain for the Dow turned into a 40-point loss, a good deal of which was attributed to her comments.The truth is, market-letter writers have been wrong in their judgments far more often than they would like to remember. However, advisors understand that the public considers short-term results meaningful when they are, more often than not, simply chance. Those in the public eye usually gain large numbers of new subscribers for being right by random luck. Which brings us to another important probability error that falls under the broad rubric of representativeness. Amos Tversky and Daniel Kahneman call this one the "law of small numbers.". The statistically valid "law of large numbers" states that large samples will usually be highly representative of the population from which they are drawn; for example, public opinion polls are fairly accurate because they draw on large and representative groups. The smaller the sample used, however (or the shorter the record), the more likely the findings are chance rather than meaningful. Yet the Tversky and Kahneman study showed that typical psychological or educational experimenters gamble their research theories on samples so small that the results have a very high probability of being chance. This is the same as gambling on the single good call of an advisor. The psychologists and educators are far too confident in the significance of results based on a few observations or a short period of time, even though they are trained in statistical techniques and are aware of the dangers.Note how readily people over generalize the meaning of a small number of supporting facts. Limited statistical evidence seems to satisfy our intuition no matter how inadequate the depiction of reality. Sometimes the evidence we accept runs to the absurd. A good example of the major overemphasis on small numbers is the almost blind faith investors place in governmental economic releases on employment, industrial production, the consumer price index, the money supply, the leading economic indicators, etc. These statistics frequently trigger major stock- and bond-market reactions, particularly if the news is bad. Flash statistics, more times than not, are near worthless. Initial economic and Fed figures are revised significantly for weeks or months after their release, as new and "better" information flows in. Thus, an increase in the money supply can turn into a decrease, or a large drop in the leading indicators can change to a moderate increase. These revisions occur with such regularity you would think that investors, particularly pros, would treat them with the skepticism they deserve. Alas, the real world refuses to follow the textbooks. Experience notwithstanding, investors treat as gospel all authoritative-sounding releases that they think pinpoint the development of important trends. An example of how instant news threw investors into a tailspin occurred in July of 1996. Preliminary statistics indicated the economy was beginning to gain steam. The flash figures showed that GDP (gross domestic product) would rise at a 3% rate in the next several quarters, a rate higher than expected. Many people, convinced by these statistics that rising interest rates were imminent, bailed out of the stock market that month. To the end of that year, the GDP growth figures had been revised down significantly (unofficially, a minimum of a dozen times, and officially at least twice). The market rocketed ahead to new highs to August l997, but a lot of investors had retreated to the sidelines on the preliminary bad news. The advice of a world champion chess player when asked how to avoid making a bad move. His answer: "Sit on your hands”. But professional investors don't sit on their hands; they dance on tiptoe, ready to flit after the least particle of information as if it were a strongly documented trend. The law of small numbers, in such cases, results in decisions sometimes bordering on the inane. Tversky and Kahneman‘s findings, which have been repeatedly confirmed, are particularly important to our understanding of some stock market errors and lead to another rule that investors should follow.Which statement does not reflect the true essence of the passage? I. Tversky and Kahneman understood that small representative groups bias the research theories to generalize results that can be categorized as meaningful result and people simplify the real impact of passable portray of reality by small number of supporting facts. II. Governmental economic releases on macroeconomic indicators fetch blind faith from investors who appropriately discount these announcements which are ideally reflected in the stock and bond market prices. III. Investors take into consideration myopic gain and make it meaningful investment choice and fail to see it as a chance of occurrence. IV. lrrational overreaction to key regulators expressions is same as intuitive statistician stumbling disastrously when unable to sustain spectacular performance.....

MCQ-> Read the following passage carefully and answer the question given below it. Certain words have been printed in bold to help you locate them while answering some of the questions.Agriculture has always been celebrated as the primary sector in India. Thanks to the Green Revolution, India is now self-sufficient in food production. Indian agriculture has been making technological advancement as well. Does that mean everything is looking bright for Indian agriculture ? A superficial analysis of the above points would tempt one to say yes, but the truth is far from it. The reality is that Indian farmers have to face extreme poverty and financial crisis, which is driving them to suicides. What are the grave adversities that drive the farmers to commit suicide, at a time when Indian economy is supposed to be gearing up to take on the world ?Indian agriculture is predominantly dependent on nature. Irrigation facilities that are currently available, do not cover the entire cultivable land. If the farmers are at the mercy of monsoons for timely water for their crops, they are at the mercy of the government for alternative irrigation facilities. Any failure of nature, directly affects the fortunes of the farmers. Secondly, Indian agriculture is largely an unorganized sector, there is no systematic planning in cultivation, farmers work on lands of uneconomical sizes, institutional finances are not available and minimum purchase prices of the government do not in reality reach the poorest farmer. Added to this, the cost of agricultural inputs have been steadily rising over the years, farmers’ margins of profits have been narrowing because the price rise in inputs is not complemented by an increase in the purchase price of the agricultural produce. Even today, in several parts of the country, agriculture is a seasonal occupation. In many districts, farmers get only one crop per year and for the remaining part of the year, they find it difficult to make both ends meet.The farmers normally resort to borrowing from money lenders, in the absence of institutionalized finance. Where institutional finance is available, the ordinary farmer does not have a chance of availing it because of the “procedures” involved in disbursing the finance. This calls for removing the elaborate formalities for obtaining the loans. The institutional finance, where available is mostly availed by the medium or large land owners, the small farmers do not even have the awareness of the existence of such facilities. The money lender is the only source of finance to the farmers. Should the crops fail, the farmers fall into a debt trap and crop failures piled up over the years give them no other option than ending their lives.Another disturbing trend has been observed where farmers commit suicide or deliberately kill a family member in order to avail relief and benefits announced by the government to support the families of those who have committed suicide so that their families could at least benefit from the Government’s relief programmes. What then needs to be done to prevent this sad state of affairs ? There cannot be one single solution to end the woes of farmers.Temporary measures through monetary relief would not be the solution. The governmental efforts should be targeted at improving the entire structure of the small wherein the relief is not given on a drought to drought basis, rather they are taught to overcome their difficulties through their own skills and capabilities. Social responsibility also goes a long way to help the farmers. General public, NGOs, Corporate and other organizations too can play a part in helping farmers by adopting drought affected villages and families and helping them to rehabilitate.The nation has to realize that farmers’ suicides are not minor issues happening in remote parts of a few states, it is a reflection of the true state of the basis of our economy.What does the author mean by “procedures” when he says that ‘farmers do not get a chance of availing institutional finance because of procedures involved in it’ ?

....

MCQ-> Answer the questions based on the information given below: Madhubala Devi, who works as a domestic help, received Rs. 2500 as Deepawali bonus from her employer. With that money she is contemplating purchase of one or more among 5 available government bonds - A, B, C, D and E. To purchase a bond Madhubala Devi will have to pay the price of the bond. If she owns a bond she receives a stipulated amount of money every year (which is termed as the coupon payment) till the maturity of the bond. At the maturity of the bond she also receives the face value of the bond. Price of a bond is given by: $$P=[\sum_{t=1}^T\frac{C}{(1+r)^{t}}]+\frac{F}{(1+r)^{t}}$$ where C is coupon payment on the bond. which is the amount of money the holder of the bond receives annually; F is the face value of the bond, which is the amount of money the holder of the bond receives when the bond matures (over and above the coupon payment for the year of maturity); T is the number of years in which the bond matures; R = 0.25, which means the market rate of interest is 25%. Among the 5 bonds the bond A and another two bonds mature in 2 years, one of the bonds matures in 3 years, and the bond D matures in 5 years. The coupon payments on bonds A, E, B, D and C are in arithmetic progression, such that the coupon payment on bond A is twice the common difference, and the coupon payment on bond B is half the price of bond A. The face value of bond B is twice the face value of bond E, but the price of bond B is 75% more than the price of bond E. The price of bond C is more than Rs. 1800 and its face value is same as the price of bond A. The face value of bond A is Rs. 1000. Bond D has the largest face value among the five bonds.The face value of bond E must be

....

MCQ-> Read the following passage carefully and answer the questions given below it. Certain words/phrases are given in bold to help you locate them while answering some of the questions. Core competencies and focus are now the mantras of corporate strategists in Western economies. But while managers in the West have

dismantled

many conglomerates assembled in the 1960s and 1970s, the large, diversified business group remains the dominant form of enterprise throughout most emerging markets. Some groups operate as holding companies with full ownership in many enterprises, others are collections of publicly traded companies, but all have some degree of central control. As emerging markets open up to global competition, consultants and foreign investors are increasingly pressuring these groups to

conform to

Western practice by scaling back the scope of their business activities. The conglomer-, ate is the dinosaur of organizational design, they argue, too unwieldy and slow to compete in today’s fast-paced markets. Already a number of executives have decided to break up their groups in order to show that they are focusing on only a few core businesses. There are reasons to worry about this trend. Focus is good advice in New York or London, but something important gets lost in translation when that advice is given to groups in emerging markets. Western companies take for granted a range of institutions that support their business activities, but many of these institutions are absent in other regions of the world. Without effective securities regulation and venture capital firms, for example, focused companies may be unable to raise adequate financing; and without strong educational institutions, they will struggle to hire skilled employees. Communicating with customers is difficult when the local infrastructure is poor, and unpredictable government behavior can stymie any operation. Although a focused strategy may enable a company to perform a few activities well, companies in emerging markets must take responsibility for a wide range of functions in order to do business effectively. In the case of product markets, buyers and sellers usually suffer from a severe

dearth

of information for three reasons. First, the communications infrastructure in emerging markets is often underdeveloped. Even as wireless communication spreads throughout the West, vast stretches in countries such as China and India remain without telephones. Power shortages often render the modes of communication that do exist ineffective. The postal service is typically inefficient, slow, or unreliable; and the private sector rarely provides efficient courier services. High rates of illiteracy make it difficult for marketers to communicate effectively with customers. Second, even when information about products does get around, there are no mechanisms to corroborate the claims made by sellers. Independent consumer-information organizations are rare, and government watchdog agencies are of little use. The few analysts who rate products are generally less sophisticated than their counterparts in advanced economies. Third, consumers have no redress mechanisms if a product does not deliver on its promise. Law enforcement is often

capricious

and so slow that few who assign any value to time would resort to it. Unlike in advanced markets, there are few extrajudicial arbitration mechanisms to which one can appeal. As a result of this lack of information, companies in emerging markets face much higher costs in building credible brands than their counterparts in advanced economies. In turn, established brands wield tremendous power. A conglomerate with a reputation for quality products and services can use its group name to enter new businesses, even if those businesses are completely unrelated to its current lines. Groups also have an advantage when they do try to build up a brand because they can spread the cost of maintaining it across multiple lines of business. Such groups then have a greater incentive not to damage brand quality in any one business because they will pay the price in their other businesses as well.Which of the following sentence(s) is/are correct in the context of the given passage ? I. Consultants and foreign investors argue that the conglomerate is the dinosaur of organisational design too unvvieldly and slow to compete in today’s fast-paced markets. II. Core competencies and focus are now the mantras of corporate strategists in western economies. III. Due to lack of information required, companies in emerging markets face much higher costs in building credible brands in comparison to their counterparts in advanced economies.....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.Mr. Sanyal invested his entire fund in gold, US bonds and EU bonds in January 2010. He liquefied his assets on 31st August 2010 and gained 13% on his investments. If instead he had held his assets for an additional month he would have gained l6.25%. Which of the following options is correct?