Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in 2016

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Multiple Choice Questions

1. To reduce costs, we should replace our current system by much efficient one.

(A): through more efficient

(B): efficiently by

(C): with a more efficient

(D): for better efficiency

(E): No correction required

Previous Question

Show Answer

Next Question

Add Tags

Report Error

Show Marks

Write Comment

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

IBPS Clerk 27-Nov-2011 SZ 2nd

Show Similar Question And Answers

QA->A shopkeeper wants to get 20% gain on an article after allowing a discount of 15%. If the article costs him Rs.153, what price should be mark on the article?....

QA->… is a copper containing respiratory pigment occurring in arthropods and molluses. It is much less efficient as oxygen carrier?....

QA->A transformer has a turn ration of 1:If the current in the primary has a peak value of 5A, then the current in the secondary will be :....

QA->How much the time gap between two sessions of the Parliament should not exceed?....

QA->A vendor bought 3 chocolates for 1 rupee. For how much per chocolate should he sell, to gain a profit of 50% ?....

MCQ-> Read the passage carefully and answer the questions given at the end of each passage:Turning the business involved more than segmenting and pulling out of retail. It also meant maximizing every strength we had in order to boost our profit margins. In re-examining the direct model, we realized that inventory management was not just core strength; it could be an incredible opportunity for us, and one that had not yet been discovered by any of our competitors. In Version 1.0 the direct model, we eliminated the reseller, thereby eliminating the mark-up and the cost of maintaining a store. In Version 1.1, we went one step further to reduce inventory inefficiencies. Traditionally, a long chain of partners was involved in getting a product to the customer. Let’s say you have a factory building a PC we’ll call model #4000. The system is then sent to the distributor, which sends it to the warehouse, which sends it to the dealer, who eventually pushes it on to the consumer by advertising, “I’ve got model #4000. Come and buy it.” If the consumer says, “But I want model #8000,” the dealer replies, “Sorry, I only have model #4000.” Meanwhile, the factory keeps building model #4000s and pushing the inventory into the channel. The result is a glut of model #4000s that nobody wants. Inevitably, someone ends up with too much inventory, and you see big price corrections. The retailer can’t sell it at the suggested retail price, so the manufacturer loses money on price protection (a practice common in our industry of compensating dealers for reductions in suggested selling price). Companies with long, multi-step distribution systems will often fill their distribution channels with products in an attempt to clear out older targets. This dangerous and inefficient practice is called “channel stuffing”. Worst of all, the customer ends up paying for it by purchasing systems that are already out of date Because we were building directly to fill our customers’ orders, we didn’t have finished goods inventory devaluing on a daily basis. Because we aligned our suppliers to deliver components as we used them, we were able to minimize raw material inventory. Reductions in component costs could be passed on to our customers quickly, which made them happier and improved our competitive advantage. It also allowed us to deliver the latest technology to our customers faster than our competitors. The direct model turns conventional manufacturing inside out. Conventional manufacturing, because your plant can’t keep going. But if you don’t know what you need to build because of dramatic changes in demand, you run the risk of ending up with terrific amounts of excess and obsolete inventory. That is not the goal. The concept behind the direct model has nothing to do with stockpiling and everything to do with information. The quality of your information is inversely proportional to the amount of assets required, in this case excess inventory. With less information about customer needs, you need massive amounts of inventory. So, if you have great information – that is, you know exactly what people want and how much - you need that much less inventory. Less inventory, of course, corresponds to less inventory depreciation. In the computer industry, component prices are always falling as suppliers introduce faster chips, bigger disk drives and modems with ever-greater bandwidth. Let’s say that Dell has six days of inventory. Compare that to an indirect competitor who has twenty-five days of inventory with another thirty in their distribution channel. That’s a difference of forty-nine days, and in forty-nine days, the cost of materials will decline about 6 percent. Then there’s the threat of getting stuck with obsolete inventory if you’re caught in a transition to a next- generation product, as we were with those memory chip in 1989. As the product approaches the end of its life, the manufacturer has to worry about whether it has too much in the channel and whether a competitor will dump products, destroying profit margins for everyone. This is a perpetual problem in the computer industry, but with the direct model, we have virtually eliminated it. We know when our customers are ready to move on technologically, and we can get out of the market before its most precarious time. We don’t have to subsidize our losses by charging higher prices for other products. And ultimately, our customer wins. Optimal inventory management really starts with the design process. You want to design the product so that the entire product supply chain, as well as the manufacturing process, is oriented not just for speed but for what we call velocity. Speed means being fast in the first place. Velocity means squeezing time out of every step in the process. Inventory velocity has become a passion for us. To achieve maximum velocity, you have to design your products in a way that covers the largest part of the market with the fewest number of parts. For example, you don’t need nine different disk drives when you can serve 98 percent of the market with only four. We also learned to take into account the variability of the lost cost and high cost components. Systems were reconfigured to allow for a greater variety of low-cost parts and a limited variety of expensive parts. The goal was to decrease the number of components to manage, which increased the velocity, which decreased the risk of inventory depreciation, which increased the overall health of our business system. We were also able to reduce inventory well below the levels anyone thought possible by constantly challenging and surprising ourselves with the result. We had our internal skeptics when we first started pushing for ever-lower levels of inventory. I remember the head of our procurement group telling me that this was like “flying low to the ground 300 knots.” He was worried that we wouldn’t see the trees.In 1993, we had $2.9 billion in sales and $220 million in inventory. Four years later, we posted $12.3 billion in sales and had inventory of $33 million. We’re now down to six days of inventory and we’re starting to measure it in hours instead of days. Once you reduce your inventory while maintaining your growth rate, a significant amount of risk comes from the transition from one generation of product to the next. Without traditional stockpiles of inventory, it is critical to precisely time the discontinuance of the older product line with the ramp-up in customer demand for the newer one. Since we were introducing new products all the time, it became imperative to avoid the huge drag effect from mistakes made during transitions. E&O; – short for “excess and obsolete” - became taboo at Dell. We would debate about whether our E&O; was 30 or 50 cent per PC. Since anything less than $20 per PC is not bad, when you’re down in the cents range, you’re approaching stellar performance.Find out the TRUE statement:

....

MCQ-> Read carefully the four passages that follow and answer the questions given at the end of each passage:PASSAGE I The most important task is revitalizing the institution of independent directors. The independent directors of a company should be faithful fiduciaries protecting, the long-term interests of shareholders while ensuring fairness to employees, investor, customer, regulators, the government of the land and society. Unfortunately, very often, directors are chosen based of friendship and, sadly, pliability. Today, unfortunately, in the majority of cases, independence is only true on paper.The need of the hour is to strengthen the independence of the board. We have to put in place stringent standards for the independence of directors. The board should adopt global standards for director-independence, and should disclose how each independent director meets these standards. It is desirable to have a comprehensive report showing the names of the company employees of fellow board members who are related to each director on the board. This report should accompany the annual report of all listed companies. Another important step is to regularly assess the board members for performance. The assessment should focus on issues like competence, preparation, participation and contribution. Ideally, this evaluation should be performed by a third party. Underperforming directors should be allowed to leave at the end of their term in a gentle manner so that they do not lose face. Rather than being the rubber stamp of a company’s management policies, the board should become a true active partner of the management. For this, independent directors should be trained in their in their in roles and responsibilities. Independent directors should be trained on the business model and risk model of the company, on the governance practices, and the responsibilities of various committees of the board of the company. The board members should interact frequently with executives to understand operational issues. As part of the board meeting agenda, the independent directors should have a meeting among themselves without the management being present. The independent board members should periodically review the performance of the company’s CEO, the internal directors and the senior management. This has to be based on clearly defined objective criteria, and these criteria should be known to the CEO and other executive directors well before the start of the evolution period. Moreover, there should be a clearly laid down procedure for communicating the board’s review to the CEO and his/her team of executive directors. Managerial remuneration should be based on such reviews. Additionally, senior management compensation should be determined by the board in a manner that is fair to all stakeholders. We have to look at three important criteria in deciding managerial remuneration-fairness accountability and transparency. Fairness of compensation is determined by how employees and investors react to the compensation of the CEO. Accountability is enhanced by splitting the total compensation into a small fixed component and a large variable component. In other words, the CEO, other executive directors and the senior management should rise or fall with the fortunes of the company. The variable component should be linked to achieving the long-term objectives of the firm. Senior management compensation should be reviewed by the compensation committee of the board consisting of only the independent directors. This should be approved by the shareholders. It is important that no member of the internal management has a say in the compensation of the CEO, the internal board members or the senior management. The SEBI regulations and the CII code of conduct have been very helpful in enhancing the level of accountability of independent directors. The independent directors should decide voluntarily how they want to contribute to the company. Their performance should decide voluntarily how they want to contribute to the company. Their performance should be appraised through a peer evaluation process. Ideally, the compensation committee should decide on the compensation of each independent director based on such a performance appraisal. Auditing is another major area that needs reforms for effective corporate governance. An audit is the Independent examination of financial transactions of any entity to provide assurance to shareholder and other stakeholders that the financial statements are free of material misstatement. Auditors are qualified professionals appointed by the shareholders to report on the reliability of financial statements prepared by the management. Financial markets look to the auditor’s report for an independent opinion on the financial and risk situation of a company. We have to separate such auditing form other services. For a truly independent opinion, the auditing firm should not provide services that are perceived to be materially in conflict with the role of the auditor. These include investigations, consulting advice, sub contraction of operational activities normally undertaken by the management, due diligence on potential acquisitions or investments, advice on deal structuring, designing/implementing IT systems, bookkeeping, valuations and executive recruitment. Any departure from this practice should be approved by the audit committee in advance. Further, information on any such exceptions must be disclosed in the company’s quarterly and annual reports. To ensure the integrity of the audit team, it is desirable to rotate auditor partners. The lead audit partner and the audit partner responsible for reviewing a company’s audit must be rotated at least once every three to five years. This eliminates the possibility of the lead auditor and the company management getting into the kind of close, cozy relationship that results in lower objectivity in audit opinions. Further, a registered auditor should not audit a chief accounting office was associated with the auditing firm. It is best that members of the audit teams are prohibited from taking up employment in the audited corporations for at least a year after they have stopped being members of the audit team.A competent audit committee is essential to effectively oversee the financial accounting and reporting process. Hence, each member of the audit committee must be ‘financially literate’, further, at least one member of the audit committee, preferably the chairman, should be a financial expert-a person who has an understanding of financial statements and accounting rules, and has experience in auditing. The audit committee should establish procedures for the treatment of complaints received through anonymous submission by employees and whistleblowers. These complaints may be regarding questionable accounting or auditing issues, any harassment to an employee or any unethical practice in the company. The whistleblowers must be protected. Any related-party transaction should require prior approval by the audit committee, the full board and the shareholders if it is material. Related parties are those that are able to control or exercise significant influence. These include; parent- subsidiary relationships; entities under common control; individuals who, through ownership, have significant influence over the enterprise and close members of their families; and dey management personnel.Accounting standards provide a framework for preparation and presentation of financial statements and assist auditors in forming an opinion on the financial statements. However, today, accounting standards are issued by bodies comprising primarily of accountants. Therefore, accounting standards do not always keep pace with changes in the business environment. Hence, the accounting standards-setting body should include members drawn from the industry, the profession and regulatory bodies. This body should be independently funded. Currently, an independent oversight of the accounting profession does not exist. Hence, an independent body should be constituted to oversee the functioning of auditors for Independence, the quality of audit and professional competence. This body should comprise a "majority of non- practicing accountants to ensure independent oversight. To avoid any bias, the chairman of this body should not have practiced as an accountant during the preceding five years. Auditors of all public companies must register with this body. It should enforce compliance with the laws by auditors and should mandate that auditors must maintain audit working papers for at least seven years.To ensure the materiality of information, the CEO and CFO of the company should certify annual and quarterly reports. They should certify that the information in the reports fairly presents the financial condition and results of operations of the company, and that all material facts have been disclosed. Further, CEOs and CFOs should certify that they have established internal controls to ensure that all information relating to the operations of the company is freely available to the auditors and the audit committee. They should also certify that they have evaluated the effectiveness of these controls within ninety days prior to the report. False certifications by the CEO and CFO should be subject to significant criminal penalties (fines and imprisonment, if willful and knowing). If a company is required to restate its reports due to material non-compliance with the laws, the CEO and CFO must face severe punishment including loss of job and forfeiting bonuses or equity-based compensation received during the twelve months following the filing.The problem with the independent directors has been that: I. Their selection has been based upon their compatibility with the company management II. There has been lack of proper training and development to improve their skill set III. Their independent views have often come in conflict with the views of company management. This has hindered the company’s decision-making process IV. Stringent standards for independent directors have been lacking....

MCQ-> Read passage carefully. Answer the questions by selecting the most appropriate option (with reference to the passage). PASSAGE 4While majoring in computer science isn't a requirement to participate in the Second Machine Age, what skills do liberal arts graduates specifically possess to contribute to this brave new world? Another major oversight in the debate has been the failure to appreciate that a good liberal arts education teaches many skills that are not only valuable to the general world of business, but are in fact vital to innovating the next wave of breakthrough tech-driven products and services. Many defenses of the value of a liberal arts education have been launched, of course, with the emphasis being on the acquisition of fundamental thinking and communication skills, such as critical thinking, logical argumentation, and good communication skills. One aspect of liberal arts education that has been strangely neglected in the discussion is the fact that the humanities and social sciences are devoted to the study of human nature and the nature of our communities and larger societies. Students who pursue degrees in the liberal arts disciplines tend to be particularly motivated to investigate what makes us human: how we behave and why we behave as we do. They're driven to explore how our families and our public institutions-such as our schools and legal systems-operate, and could operate better, and how governments and economies work, or as is so often the case, are plagued by dysfunction. These students learn a great deal from their particular courses of study and apply that knowledge to today's issues, the leading problems to be tackled, and various approaches for analyzing and addressing those problems. The greatest opportunities for innovation in the emerging era are in applying evolving technological capabilities to finding better ways to solve human problems like social dysfunction and political corruption; finding ways to better educate children; helping people live healthier and happier lives by altering harmful behaviors; improving our working conditions; discovering better ways to tackle poverty; Improving healthcare and making it more affordable; making our governments more accountable, from the local level up to that of global affairs; and finding optimal ways to incorporate intelligent, nimble machines into our work lives so that we are empowered to do more of the work that we do best, and to let the machines do the rest. Workers with a solid liberal arts education have a strong foundation to build on in pursuing these goals. One of the most immediate needs in technology innovation is to invest products and services with more human qualities. with more sensitivity to human needs and desires. Companies and entrepreneurs that want to succeed today and in the future must learn to consider in all aspects of their product and service creation how they can make use of the new technologies to make them more humane. Still, many other liberal arts disciplines also have much to provide the world of technological innovation. The study of psychology, for example, can help people build products that are more attuned to our emotions and ways of thinking. Experience in Anthropology can additionally help companies understand cultural and individual behavioural factors that should be considered in developing products and in marketing them. As technology allows for more machine intelligence and our lives become increasingly populated by the Internet of things and as the gathering of data about our lives and analysis of it allows for more discoveries about our behaviour, consideration of how new products and services can be crafted for the optimal enhancement of our lives and the nature of our communities, workplaces and governments will be of vital importance. Those products and services developed with the keeneSt sense of how they' can serve our human needs and complement our human talents will have a distinct competitive advantage. Much of the criticism of the liberal arts is based on the false assumption that liberal arts students lack rigor in comparison to those participating in the STEM disciplines and that they are 'soft' and unscientific whereas those who study STEM fields learn the scientific method. In fact the liberal arts teach many methods of rigorous inquiry and analysis, such as close observation and interviewing in ways that hard science adherents don't always appreciate. Many fields have long incorporated the scientific method and other types of data driven scientific inquiry and problem solving. Sociologists have developed sophisticated mathematical models of societal networks. Historians gather voluminous data on centuries-old household expenses, marriage and divorce rates, and the world trade, and use data to conduct statistical analyses, identifying trends and contributing factors to the phenomena they are studying. Linguists have developed high-tech models of the evolution of language, and they've made crucial contributions to the development of one of the technologies behind the rapid advance of automation- natural language processing, whereby computers are able to communicate with the, accuracy and personality of Siri and Alexa. It's also important to debunk the fallacy that liberal arts students who don't study these quantitative analytical methods have no 'hard' or relevant skills. This gets us back to the arguments about the fundamental ways of thinking, inquiring, problem solving and communicating that a liberal arts education teaches.What is the central theme of the passage?

....

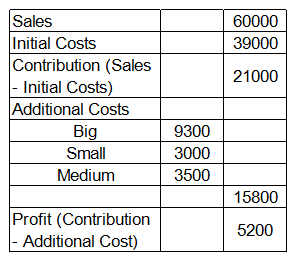

MCQ-> Read the following caselet and choose the best alternative

The BIG and Colourful Company

You are running "BIG and Colourful (BnC)" company that sells books to customers through three retail formats: a. You can buy books from bookstores, b. You can buy books from supermarket, c. You can order books over the Internet (Online). Your manager has an interesting way of classifying expenses: some of the expenses are classified in terms of size: Big, Small and Medium; and others are classified in terms of the colors, Red, Yellow, Green and Violet. The company has a history of categorizing overall costs into initial costs and additional costs. Additional costs are equal to the sum of Big, Small and Medium expenses. There are two types of margins, contribution (sales minus initial costs) and profit (contribution minus additional costs). Given below is the data about sales and costs of BnC:

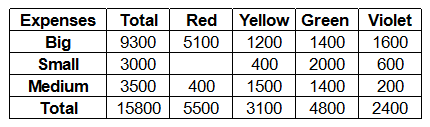

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below:

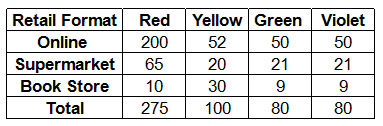

Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below:

Read the following statements: Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2. Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....

MCQ-> Read the following passage carefully and answer the questions given at the end. The second issue I want to address is one that comes up frequently - that Indian banks should aim to become global. Most people who put forward this view have not thought through the costs and benefits analytically; they only see this as an aspiration consistent with India’s growing international profile. In its 1998 report, the Narasimham (II) Committee envisaged a three tier structure for the Indian banking sector: 3 or 4 large banks having an international presence on the top, 8-10 mid-sized banks, with a network of branches throughout the country and engaged in universal banking, in the middle, and local banks and regional rural banks operating in smaller regions forming the bottom layer. However, the Indian banking system has not consolidated in the manner envisioned by the Narasimham Committee. The current structure is that India has 81 scheduled commercial banks of which 26 are public sector banks, 21 are private sector banks and 34 are foreign banks. Even a quick review would reveal that there is no segmentation in the banking structure along the lines of Narasimham II.A natural sequel to this issue of the envisaged structure of the Indian banking system is the Reserve Bank’s position on bank consolidation. Our view on bank consolidation is that the process should be market-driven, based on profitability considerations and brought about through a process of mergers & amalgamations (M&As;). The initiative for this has to come from the boards of the banks concerned which have to make a decision based on a judgment of the synergies involved in the business models and the compatibility of the business cultures. The Reserve Bank’s role in the reorganisation of the banking system will normally be only that of a facilitator.lt should be noted though that bank consolidation through mergers is not always a totally benign option. On the positive side are a higher exposure threshold, international acceptance and recognition, improved risk management and improvement in financials due to economies of scale and scope. This can be achieved both through organic and inorganic growth. On the negative side, experience shows that consolidation would fail if there are no synergies in the business models and there is no compatibility in the business cultures and technology platforms of the merging banks.Having given that broad brush position on bank consolidation let me address two specific questions: (i) can Indian banks aspire to global size?; and (ii) should Indian banks aspire to global size? On the first question, as per the current global league tables based on the size of assets, our largest bank, the State Bank of India (SBI), together with its subsidiaries, comes in at No.74 followed by ICICI Bank at No. I45 and Bank of Baroda at 188. It is, therefore, unlikely that any of our banks will jump into the top ten of the global league even after reasonable consolidation.Then comes the next question of whether Indian banks should become global. Opinion on this is divided. Those who argue that we must go global contend that the issue is not so much the size of our banks in global rankings but of Indian banks having a strong enough, global presence. The main argument is that the increasing global size and influence of Indian corporates warrant a corresponding increase in the global footprint of Indian banks. The opposing view is that Indian banks should look inwards rather than outwards, focus their efforts on financial deepening at home rather than aspiring to global size.It is possible to take a middle path and argue that looking outwards towards increased global presence and looking inwards towards deeper financial penetration are not mutually exclusive; it should be possible to aim for both. With the onset of the global financial crisis, there has definitely been a pause to the rapid expansion overseas of our banks. Nevertheless, notwithstanding the risks involved, it will be opportune for some of our larger banks to be looking out for opportunities for consolidation both organically and inorganically. They should look out more actively in regions which hold out a promise of attractive acquisitions.The surmise, therefore, is that Indian banks should increase their global footprint opportunistically even if they do not get to the top of the league table.Identify the correct statement from the following:

....

×

×

Type The Issue

×

Your Marks

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below:

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below: Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below:

Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below: Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....

Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then....