1. Who hasbeen appointed as the CEO of largest life insurance companies in the worldReliance Nippon Life Insurance with effect from October 3, 2016?

Answer: Ashish Vohra

Tags

Show Similar Question And Answers

Powered By:Omega Web Solutions

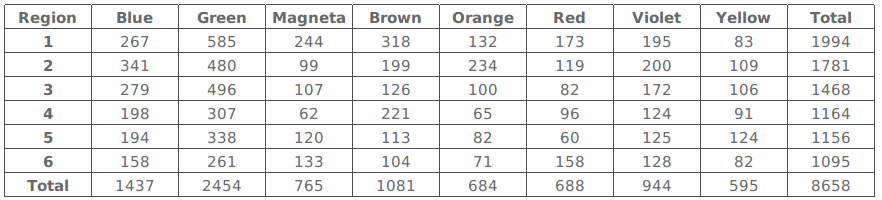

Powered By:Omega Web Solutions Table 2

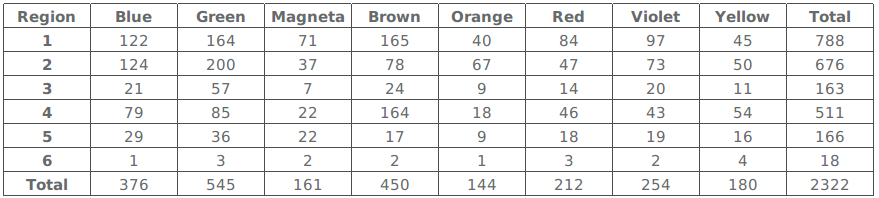

Table 2 Table 3

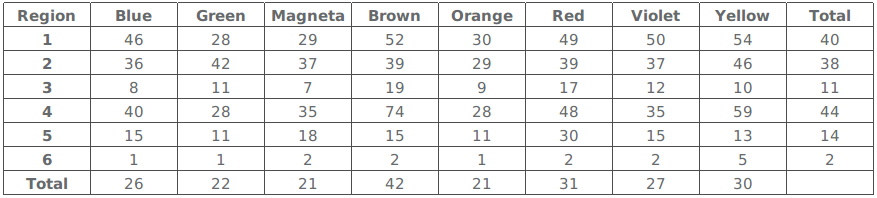

Table 3 Table 4

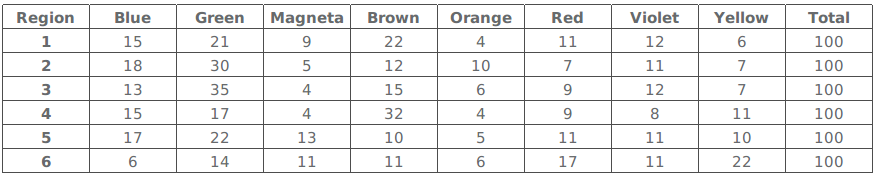

Table 4 Table 5

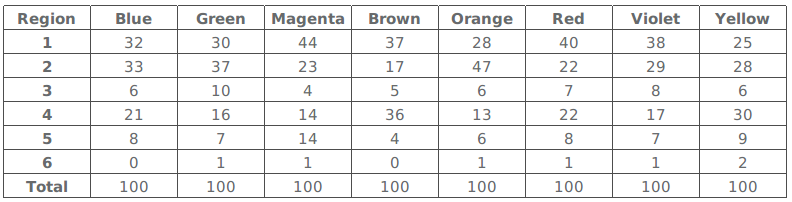

Table 5 Which region-colour combination accounts for the highest percentage of sales to stock?

Which region-colour combination accounts for the highest percentage of sales to stock?