Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Multiple Choice Question in 100/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Question Answer Bank

1. Who became the first India female cricketer to be signed by an overseas Twenty20 league (Big Bash League)?

Answer: Harmanpreet Kaur.

Previous Question

Next Question

Add Tags

Report Error

Reply

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->Who became the first India female cricketer to be signed by an overseas Twenty20 league (Big Bash League)?....

QA->Which cricketer won the "South Africa Cricketer of the Year-2013" and "Test Cricketer of the Year-2013" awards?....

QA->Which cricketer has been declared ICC Cricketer of the Year -2014 as well as the ICC Test cricketer of the Year-2014?....

QA->Which team won the Champions League Twenty20 2012 title held in South Africa?....

QA->Which team won the Champions League Twenty20 title-2013?....

MCQ-> Read the following passages carefully and answer the questions given at the end of each passage.PASSAGE 3Typically women participate in the labour force at a very high rate in poor rural countries. The participation rate then falls as countries industrialise and move into the middle income class. Finally, if the country grows richer still, more families have the resources for higher education for women and from there they often enter the labour force in large numbers. Usually, economic growth goes hand in hand with emancipation of women. Among rich countries according to a 2015 study, female labour force participation ranges from nearly 80 percent in Switzerland to 70 percent in Germany and less than 60 Percent in the United States and Japan. Only 68 Percent of Canadian omen participated in the workforce in 1990; two decades later that increased to 74 Percent largely due to reforms including tax cuts for second earners and new childcare services. In Netherlands the female labour participation rate doubled since 1980 to 74 Percent as a result of expanded parental leave policies and the spread of flexible, part time working arrangements. In a 2014 survey of 143 emerging countries, the World Bank found that 90 Percent have at least one law that limits the economic opportunities available to women. These laws include bans or limitations on women owning property, opening a bank account, signing a contract, entering a courtroom, travelling alone, driving or controlling family finances. Such restrictions are particularly prevalent in the Middle East and South Asia with the world’s lowest female labour force participation, 26 and 35 percent respectively. According to date available with the International Labour Organisation (ILO), between 2004 and 2011, when the Indian economy grew at a healthy average of about 7 percent, there was a decline in female participation in the country’s labour force from over 35 percent to 25 percent. India also posted the lowest rate of female participation in the workforce among BRIC countries. India’s performance in female workforce participation stood at 27 percent, significantly behind China (64 percent), Brazil (59 percent), Russian Federation (57 percent), and South Africa (45 percent). The number of working women in India had climbed between 2000 and 2005, increasing from 34 percent to 37 percent, but since then the rate of women in the workforce has to fallen to 27 percent as of 2014, said the report citing data from the World Bank. The gap between male and female workforce participation in urban areas in 2011 stood at 40 percent, compared to rural areas where the gap was about 30 percent. However, in certain sectors like financial services, Indian women lead the charge. While only one in 10 Indian companies are led by women, more than half of them are in the financial sector. Today, women head both the top public and private banks in India. Another example is India’s aviation sector, 11.7 percent of India’s 5,100 pilots are women, versus 3 percent worldwide. But these successes only represent a small of women in the country. India does poorly in comparison to its neighbours despite a more robust economic growth. In comparison to India, women in Bangladesh have increased their participation in the labour market, which is due to the growth of the ready- made garment sector and a push to rural female employment. In 2015, women comprised of 43 percent of the labour force in Bangladesh. The rate has also increased in Pakistan, albeit from a very low starting point, while participation has remained relatively stable in Sri Lanka. Myanmar with 79 percent and Malaysia with 49 percent are also way ahead of India. Lack of access to higher education, fewer job opportunities, the lack of flexibility in working conditions, as well as domestic duties are cited as factors behind the low rates. Marriage significantly reduced the probability of women working by about 8 percent in rural areas and more than twice as much in urban areas, said an Assocham report. ILO attributes this to three factors: increasing educational enrolment, improvement in earning of male workers that discourage women’s economic participation, and lack of employment opportunities at certain levels of skills and qualifications discouraging women to seek work. The hurdles to working women often involve a combination of written laws and cultural norms. Cultures don’t change overnight but laws can. The IMF says that even a small step such as countries granting women the right to open a bank account can lead to substantial increase in female labour force participation over the next seven years. According to the United Nations Economic and Social Commission for Asia and the Pacific (ESCAP), even a 10 percent increase in women participating in the workforce can boost gross domestic product (GDP) by 0.3 percent. The OECD recently estimated that eliminating the gender gap would lead to an overall increase in GDP of 12 percent in its member nations between 2015 and 2030. The GDP gains would peak close to 20 percent in both Japan and South Korea and more than 20 percent in Italy. A similar analysis by Booz and Company showed that closing gender gap in emerging countries could yield even larger gains in GDP by 2020, ranging from a 34 percent gain in Egypt to 27 percent in India and 9 percent in Brazil. According to the above passage, though there are many reasons for low female labour force participation, the most important focus of the passage is on

...

MCQ-> Read the following passage carefully and answer the questions given at the end.Passage 4Public sector banks (PSBs) are pulling back on credit disbursement to lower rated companies, as they keep a closer watch on using their own scarce capital and the banking regulator heightens its scrutiny on loans being sanctioned. Bankers say the Reserve Bank of India has started strictly monitoring how banks are utilizing their capital. Any big-ticket loan to lower rated companies is being questioned. Almost all large public sector banks that reported their first quarter results so far have showed a contraction in credit disbursal on a year-to-date basis, as most banks have shifted to a strategy of lending largely to government-owned "Navratna" companies and highly rated private sector companies. On a sequential basis too, banks have grown their loan book at an anaemic rate.To be sure, in the first quarter, loan demand is not quite robust. However, in the first quarter last year, banks had healthier loan growth on a sequential basis than this year. The country's largest lender State Bank of India grew its loan book at only 1.21% quarter-on-quarter. Meanwhile, Bank of Baroda and Punjab National Bank shrank their loan book by 1.97% and 0.66% respectively in the first quarter on a sequential basis.Last year, State Bank of India had seen sequential loan growth of 3.37%, while Bank of Baroda had seen a smaller contraction of 0.22%. Punjab National Bank had seen a growth of 0.46% in loan book between the January-March and April-June quarters last year. On a year-to-date basis, SBI's credit growth fell more than 2%, Bank of Baroda's credit growth contracted 4.71% and Bank of India's credit growth shrank about 3%. SBI chief Arundhati Bhattacharya said the bank's year-to-date credit growth fell as the bank focused on ‘A’ rated customers. About 90% of the loans in the quarter were given to high-rated companies. "Part of this was a conscious decision and part of it is because we actually did not get good fresh proposals in the quarter," Bhattacharya said.According to bankers, while part of the credit contraction is due to the economic slowdown, capital constraints and reluctance to take on excessive risk has also played a role. "Most of the PSU banks are facing pressure on capital adequacy. It is challenging to maintain 9% core capital adequacy. The pressure on monitoring capital adequacy and maintaining capital buffer is so strict that you cannot grow aggressively," said Rupa Rege Nitsure, chief economist at Bank of Baroda.Nitsure said capital conservation pressures will substantially cut down "irrational expansion of loans" in some smaller banks, which used to grow at a rate much higher than the industry average. The companies coming to banks, in turn, will have to make themselves more creditworthy for banks to lend. "The conservation of capital is going to inculcate a lot of discipline in both banks and borrowers," she said.For every loan that a bank disburses, some amount of money is required to be set aside as provision. Lower the credit rating of the company, riskier the loan is perceived to be. Thus, the bank is required to set aside more capital for a lower rated company than what it otherwise would do for a higher rated client. New international accounting norms, known as Basel III norms, require banks to maintain higher capital and higher liquidity. They also require a bank to set aside "buffer" capital to meet contingencies. As per the norms, a bank's total capital adequacy ratio should be 12% at any time, in which tier-I, or the core capital, should be at 9%. Capital adequacy is calculated by dividing total capital by risk-weighted assets. If the loans have been given to lower rated companies, risk weight goes up and capital adequacy falls.According to bankers, all loan decisions are now being assessed on the basis of the capital that needs to be set aside as provision against the loan and as a result, loans to lower rated companies are being avoided. According to a senior banker with a public sector bank, the capital adequacy situation is so precarious in some banks that if the risk weight increases a few basis points, the proposal gets cancelled. The banker did not wish to be named. One basis point is one hundredth of a percentage point. Bankers add that the Reserve Bank of India has also started strictly monitoring how banks are utilising their capital. Any big-ticket loan to lower rated companies is being questioned.In this scenario, banks are looking for safe bets, even if it means that profitability is being compromised. "About 25% of our loans this quarter was given to Navratna companies, who pay at base rate. This resulted in contraction of our net interest margin (NIM)," said Bank of India chairperson V.R. Iyer, while discussing the bank's first quarter results with the media. Bank of India's NIM, or the difference between yields on advances and cost of deposits, a key gauge of profitability, fell in the first quarter to 2.45% from 3.07% a year ago, as the bank focused on lending to highly rated customers.Analysts, however, say the strategy being followed by banks is short-sighted. "A high rated client will take loans at base rate and will not give any fee income to a bank. A bank will never be profitable that way. Besides, there are only so many PSU companies to chase. All banks cannot be chasing them all at a time. Fact is, the banks are badly hit by NPA and are afraid to lend now to big projects. They need capital, true, but they have become risk-averse," said a senior analyst with a local brokerage who did not wish to be named.Various estimates suggest that Indian banks would require more than Rs. 2 trillion of additional capital to have this kind of capital adequacy ratio by 2019. The central government, which owns the majority share of these banks, has been cutting down on its commitment to recapitalize the banks. In 2013-14, the government infused Rs. 14,000 crore in its banks. However, in 2014-15, the government will infuse just Rs. 11,200 crore.Which of the following statements is correct according to the passage?

...

MCQ-> Read the following passage carefully and answer the questions given at the end. The second issue I want to address is one that comes up frequently - that Indian banks should aim to become global. Most people who put forward this view have not thought through the costs and benefits analytically; they only see this as an aspiration consistent with India’s growing international profile. In its 1998 report, the Narasimham (II) Committee envisaged a three tier structure for the Indian banking sector: 3 or 4 large banks having an international presence on the top, 8-10 mid-sized banks, with a network of branches throughout the country and engaged in universal banking, in the middle, and local banks and regional rural banks operating in smaller regions forming the bottom layer. However, the Indian banking system has not consolidated in the manner envisioned by the Narasimham Committee. The current structure is that India has 81 scheduled commercial banks of which 26 are public sector banks, 21 are private sector banks and 34 are foreign banks. Even a quick review would reveal that there is no segmentation in the banking structure along the lines of Narasimham II.A natural sequel to this issue of the envisaged structure of the Indian banking system is the Reserve Bank’s position on bank consolidation. Our view on bank consolidation is that the process should be market-driven, based on profitability considerations and brought about through a process of mergers & amalgamations (M&As;). The initiative for this has to come from the boards of the banks concerned which have to make a decision based on a judgment of the synergies involved in the business models and the compatibility of the business cultures. The Reserve Bank’s role in the reorganisation of the banking system will normally be only that of a facilitator.lt should be noted though that bank consolidation through mergers is not always a totally benign option. On the positive side are a higher exposure threshold, international acceptance and recognition, improved risk management and improvement in financials due to economies of scale and scope. This can be achieved both through organic and inorganic growth. On the negative side, experience shows that consolidation would fail if there are no synergies in the business models and there is no compatibility in the business cultures and technology platforms of the merging banks.Having given that broad brush position on bank consolidation let me address two specific questions: (i) can Indian banks aspire to global size?; and (ii) should Indian banks aspire to global size? On the first question, as per the current global league tables based on the size of assets, our largest bank, the State Bank of India (SBI), together with its subsidiaries, comes in at No.74 followed by ICICI Bank at No. I45 and Bank of Baroda at 188. It is, therefore, unlikely that any of our banks will jump into the top ten of the global league even after reasonable consolidation.Then comes the next question of whether Indian banks should become global. Opinion on this is divided. Those who argue that we must go global contend that the issue is not so much the size of our banks in global rankings but of Indian banks having a strong enough, global presence. The main argument is that the increasing global size and influence of Indian corporates warrant a corresponding increase in the global footprint of Indian banks. The opposing view is that Indian banks should look inwards rather than outwards, focus their efforts on financial deepening at home rather than aspiring to global size.It is possible to take a middle path and argue that looking outwards towards increased global presence and looking inwards towards deeper financial penetration are not mutually exclusive; it should be possible to aim for both. With the onset of the global financial crisis, there has definitely been a pause to the rapid expansion overseas of our banks. Nevertheless, notwithstanding the risks involved, it will be opportune for some of our larger banks to be looking out for opportunities for consolidation both organically and inorganically. They should look out more actively in regions which hold out a promise of attractive acquisitions.The surmise, therefore, is that Indian banks should increase their global footprint opportunistically even if they do not get to the top of the league table.Identify the correct statement from the following:

...

MCQ-> I think that it would be wrong to ask whether 50 years of India's Independence are an achievement or a failure. It would be better to see things as evolving. It's not an either-or question. My idea of the history of India is slightly contrary to the Indian idea.India is a country that, in the north, outside Rajasthan, was ravaged and intellectually destroyed to a large extent by the invasions that began in about AD 1000 by forces and religions that India had no means of understanding.The invasions are in all the schoolbooks. But I don't think that people understand that every invasion, every war, every campaign, was accompanied by slaughter, a slaughter always of the most talented people in the country. So these wars, apart from everything else led to a tremendous intellectual depletion of the country.I think that in the British period, and in the 50 years after the British period, there has been a kind of regrouping or recovery, a very slow revival of energy and intellect. This isn't an idea that goes with the vision of the grandeur of old India and all that sort of rubbish. That idea is a great simplification and it occurs because it is intellectually, philosophically easier for Indians to manage.What they cannot manage, and what they have not yet come to terms with, is that ravaging of all the north of India by various conquerors. That was ruined not by the act of nature, but by the hand of man. It is so painful that few Indians have begun to deal with it. It is much easier to deal with British imperialism. That is a familiar topic, in India and Britain. What is much less familiar is the ravaging of India before the British.What happened from AD 1000 onwards, really, is such a wound that it is almost impossible to face. Certain wounds are so bad that they can't be written about. You deal with that kind of pain by hiding from it. You retreat from reality. I do not think, for example, that the Incas of Peru or the native people of Mexico have ever got over their defeat by the Spaniards. In both places the head was cut off. I think the pre-British ravaging of India was as bad as that.In the place of knowledge of history, you have various fantasies about the village republic and the Old Glory. There is one big fantasy that Indians have always found solace in: about India having the capacity for absorbing its conquerors. This is not so. India was laid low by its conquerors.I feel the past 150 years have been years of every kind of growth. I see the British period and what has continued after that as one period. In that time, there has been a very slow intellectual recruitment. I think every Indian should make the pilgrimage to the site of the capital of the Vijayanagar empire, just to see what the invasion of India led to. They will see a totally destroyed town. Religious wars are like that. People who see that might understand what the centuries of slaughter and plunder meant. War isn't a game. When you lost that kind of war, your town was destroyed, the people who built the towns were destroyed. You are left with a headless population.That's where modern India starts from. The Vijayanagar capital was destroyed in 1565. It is only now that the surrounding region has begun to revive. A great chance has been given to India to start up again, and I feel it has started up again. The questions about whether 50 years of India since Independence have been a failure or an achievement are not the questions to ask. In fact, I think India is developing quite marvelously, people thought — even Mr Nehru thought — that development and new institutions in a place like Bihar, for instance, would immediately lead to beauty. But it doesn't happen like that. When a country as ravaged as India, with all its layers of cruelty, begins to extend justice to people lower down, it's a very messy business. It's not beautiful, it's extremely messy. And that's what you have now, all these small politicians with small reputations and small parties. But this is part of growth, this is part of development. You must remember that these people, and the people they represent, have never had rights before.When the oppressed have the power to assert themselves, they will behave badly. It will need a couple of generations of security, and knowledge of institutions, and the knowledge that you can trust institutions — it will take at least a couple of generations before people in that situation begin to behave well. People in India have known only tyranny. The very idea of liberty is a new idea. The rulers were tyrants. The tyrants were foreigners. And they were proud of being foreign. There's a story that anybody could run and pull a bell and the emperor would appear at his window and give justice. This is a child's idea of history — the slave's idea of the ruler's mercy. When the people at the bottom discover that they hold justice in their own hands, the earth moves a little. You have to expect these earth movements in India. It will be like this for a hundred years. But it is the only way. It's painful and messy and primitive and petty, but it’s better that it should begin. It has to begin. If we were to rule people according to what we think fit, that takes us back to the past when people had no voices. With self-awareness all else follows. People begin to make new demands on their leaders, their fellows, on themselves.They ask for more in everything. They have a higher idea of human possibilities. They are not content with what they did before or what their fathers did before. They want to move. That is marvellous. That is as it should be. I think that within every kind of disorder now in India there is a larger positive movement. But the future will be fairly chaotic. Politics will have to be at the level of the people now. People like Nehru were colonial — style politicians. They were to a large extent created and protected by the colonial order. They did not begin with the people. Politicians now have to begin with the people. They cannot be too far above the level of the people. They are very much part of the people. It is important that self-criticism does not stop. The mind has to work, the mind has to be active, there has to be an exercise of the mind. I think it's almost a definition of a living country that it looks at itself, analyses itself at all times. Only countries that have ceased to live can say it's all wonderful.The central thrust of the passage is that

...

MCQ-> Read the following caselet and choose the best alternative

The BIG and Colourful Company

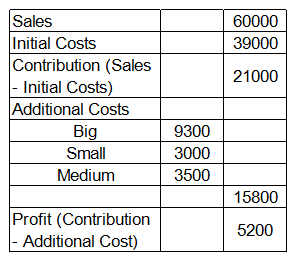

You are running "BIG and Colourful (BnC)" company that sells books to customers through three retail formats: a. You can buy books from bookstores, b. You can buy books from supermarket, c. You can order books over the Internet (Online). Your manager has an interesting way of classifying expenses: some of the expenses are classified in terms of size: Big, Small and Medium; and others are classified in terms of the colors, Red, Yellow, Green and Violet. The company has a history of categorizing overall costs into initial costs and additional costs. Additional costs are equal to the sum of Big, Small and Medium expenses. There are two types of margins, contribution (sales minus initial costs) and profit (contribution minus additional costs). Given below is the data about sales and costs of BnC:

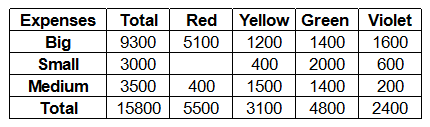

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below:

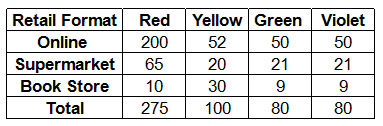

Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below:

Read the following statements: Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2. Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then...

×

×

Type The Issue

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below:

Each of the Big, Small and Medium cost is categorized by the manager into Red, Yellow, Green and Violet costs. Breakdown of the additional costs under these headings is shown in the table below: Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below:

Red, Yellow, Green and Violet costs are allocated to different retail formats. These costs are apportioned in the ratio of number of units consumed by each retail format. The number of units consumed by each retail format is given in the table below: Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then...

Read the following statements:

Statement I. Online store accounted for 50% of the sales at BnC and the ratio of supermarket sales and book store sales is 1:2.

Statement II. Initial Cost is allocated in the ratio of sales. If you want to calculate the profit/loss from the different retail formats, then...