Toggle navigation

Home

Article Category

Question Papers

General Knowlege

Popular Pages

Multiple Choice Question in 049

Multiple Choice Question in

Multiple Choice Question in TRADES-INSTRUCTOR---GR-II---SMITHY---TECHNICAL-EDUCATION

Multiple Choice Question in -current-affairs-2016

Question Answer in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in ASSISTANT-PROFESSOR---COMPUTER-SCIENCE-AND-ENGINEERING---TECHNICAL-EDUCATION

Multiple Choice Question in english

Multiple Choice Question in abbreviations-abbreviations-m

Multiple Choice Question in SSC CHSL 7 March 2018 Morning Shift

Multiple Choice Question in 072/2016

Multiple Choice Question in 100/2016

Question Answer Bank

Multiple Choice Question Bank

Question Answer Category

Multiple Choice Question Category

Home

->

Question Answer Bank

1. Parliament of which country has allowed 51% Foreign Direct Investment(FDI) in the country"s multi-brand retail sector on December 7, 2012?

Answer: India.

Previous Question

Next Question

Add Tags

Report Error

Reply

Type in

(Press Ctrl+g to toggle between English and the chosen language)

Post reply

Comments

Tags

Show Similar Question And Answers

QA->Parliament of which country has allowed 51% Foreign Direct Investment(FDI) in the country"s multi-brand retail sector on December 7, 2012?....

QA->What isthe India’s rank in terms of Foreign Direct Investment ( FDI) inflows, as per thelatest 2016 World Investment Report?....

QA->As per the recent report of the United Nations Conference on Trade and Development, which country emerged as the top destination for foreign direct investment (FDI)?....

QA->What per centof FDI is allowed in E-Commerce sector in India?....

QA->Star Hyper is a chain of retail stores in India created as a JV between Tatas and which global retail chain ?....

MCQ->

Read the following passage to answer the given question based on it. Some words/phrases are printed in bold to help you locate them while answering some of the questions.

Organized retail has “

fuelled

” new growth categories like liquid hand wash, breakfast cereals and pet foods in the consumer goods industry accounting for almost 50% of their sales said data from market search firm Nielsen The figures showed some of these new categories got more than 40% of their business from modern retail outlets.The data also suggests how products in these categories reach the neighbourhood kirana stores after they have established themselves in modern trade While grocers continue to be an important channel for the new and evolving categories we saw an increased presence of the high end products in modern trade For example

premium

products in laundry detergents dishwashing car air fresheners and surface care increased in availability through this format as these products are aimed at “

affluent

” consumers who are more likely to shop in supermarket/hypermarket outlets and who are willing to pay more for specialized products Some other categories that have grown exceptionally and now account for bulk of the sales from modern retail are frozen and With the evolution of modern trade our growth in this channel has been healthy as it is for several other categories Modern retail is an important part of our business said managing director Kellogg India. What modern retail offers to companies experimenting with new categories is the chance to educate customers which was not the case with a general trade store Category creation and market development starts with modern trade but as more consumer start consuming this category they “penetrate into other channels” said president food FMCG category Future Group the country’s largest retailer which operates stores like Big Bazaar But a point to note here is that modern retailers themselves push their own private brands in these very categories and can emerge as a big threat for the consumers goods and foods companies For instance Big Bazaar’s private label Clean Mate is hugely popular and sells more than a brand like Harpic in its own stores So there is a certain amount of conflict and competition that will play out over the next few years which the FMCG companies will have to watch out for said KPMG’s executive director (retail) In the past there have been instances of retailers boycotting products from big FMCG players on the issue of margins but as modern retail become increasingly significant for “

pushing

” new categories experts say we could see more partnerships being forged between retailers and FMCG companies Market development for new categories takes time so brand wars for leadership and consumer franchise will be fought on the modern retail platform A new brand can overnight compete with “

established

” companies by trying up with few retailers in these categories president of Future Group addedWhich of the following is being referred to as new growth category ?

...

MCQ-> Directions: Read the following passage carefully and answer the questions given below it. Certain words/phrases have been printed in bold to help you locate them while answering some of the questions. When times are hard, doomsayers are aplenty. The problem is that if you listen to them too carefully, you tend to overlook the most obvious signs of change. 2011 was a bad year. Can 2012 be any worse? Doomsday forecasts are the easiest to make these days. So let's try a contrarian's forecast instead. Let's start with the global economy. We have seen a steady flow of good news from the US. The employment situation seems to be improving rapidly and consumer sentiment, reflected in retail expenditures on discretionary items like electronics and clothes, has picked up. If these trends sustain, the US might post better growth numbers for 2012 than the 1.5 - 1.8 percent being forecast currently. Japan is likely to pull out of a recession in 2012 as post-earthquake reconstruction efforts gather momentum and the fiscal stimulus announced in 2011 begin to pay off. The consensus estimate for growth in Japan is a respectable 2 percent for 2012. The "hard landing' scenario for China remains and will remain a myth. Growth might decelerate further from the 9 percent that is expected to clock in 2011 but is unlikely to drop below 8 - 8.5 percent in 2012. Europe is certainly in a spot of trouble. It is perhaps already in recession and for 2012 it is likely to post mildly negative growth. The risk of implosion has dwindled over the last few months- peripheral economies like Greece, Italy and Spain have new governments in place and have made progress towards genuine economic reform. Even with some these positive factors in place, we have to accept the fact that global growth in 2012 will be tepid. But there is a flipside to this. Softer growth means lower demand for commodities, and this is likely to drive a correction in commodity prices. Lower commodity inflation will enable emerging market central banks to reverse their monetary stance. China, for instance, has already reversed its stance and have pared its reserve ratio twice. The RBI also seems poised for a reversal in its rate cycle as headline inflation seems well one its way to its target of 7 percent for March 2012. That said, oil might be an exception to the general trend in commodities. Rising geopolitical tensions, particularly the continuing face-off between Iran and the US, might lead to a spurt in prices. It might make sense for our oil companies to hedge this risk instead of buying oil in the spot market. As inflation fears abate, and emerging market central banks begin to cut rates, two things could happen. Lower commodity inflation would mean lower interest rates and better credit availability. This could set the floor to growth and slowly reverse the business cycle within these economies. Second, as the fear of untamed, runaway inflation in these economies abates, the global investor's comfort levels with their markets will increase. Which of the emerging markets will outperform and who will leave behind? In an environment in which global growth is likely to be weak, economies like India that have a powerful domestic consumption dynamic should lead; those dependent on exports should, prima facie, fall behind. Specifically for India, a fall in the exchange rate could not have come at a better time. It will help Indian exporters gain market share even if global trade remains depressed. More importantly, it could lead to massive import substitution that favours domestic producers.Let’s now focus on India and start with a caveat. It is important not to confuse a short run cyclical dip with a permanent derating of its long-term structural potential. The arithmetic is simple. Our growth rate can be in the range of 7-10 percent depending on policy action. Ten percent if we get everything right, 7 percent if we get it all wrong. Which policies and reforms are critical to taking us to our 10 percent potential? In judging this, let’s again be careful. Let’s not go by the laundry list of reforms that FIIs like to wave: The increase in foreign equity limits in foreign shareholding, greater voting rights for institutional shareholders in banks, FDI in retail, etc. These can have an impact only at the margin. We need not bend over backwards to appease the FIIs through these reforms they will invest in our markets when momentum picks up and will be the first to exit when the momentum flags, reforms or not. The reforms that we need are the ones that can actually raise our sustainable longterm growth rate. These have to come in areas like better targeting of subsidies, making projects in infrastructure viable so that they draw capital, raising the productivity of agriculture, improving healthcare and education, bringing the parallel economy under the tax net, implementing fundamental reforms in taxation like GST and the direct tax code and finally easing the myriad rules and regulations that make doing business in India such a nightmare. A number of these things do not require new legislation and can be done through executive order.Which of the following is not true according to the passage?

...

MCQ-> Directions : Choose the word/group of words which is most opposite in meaning to the word / group of words printed in bold as used in the passage.When times are hard, doomsayers are aplenty. The problem is that if you listen to them too carefully, you tend to overlook the most obvious signs of change. 2011 was a bad year. Can 2012 be any worse? Doomsday forecasts are the easiest to make these days. So let's try a contrarian's forecast instead. Let's start with the global economy. We have seen a steady flow of good news from the US. The employment situation seems to be improving rapidly and consumer sentiment, reflected in retail expenditures on discretionary items like electronics and clothes, has picked up. If these trends sustain, the US might post better growth numbers for 2012 than the 1.5 - 1.8 percent being forecast currently. Japan is likely to pull out of a recession in 2012 as post-earthquake reconstruction efforts gather momentum and the fiscal stimulus announced in 2011 begin to pay off. The consensus estimate for growth in Japan is a respectable 2 percent for 2012. The "hard landing' scenario for China remains and will remain a

myth

. Growth might decelerate further from the 9 percent that is expected to clock in 2011 but is unlikely to drop below 8 - 8.5 percent in 2012. Europe is certainly in a spot of trouble. It is perhaps already in recession and for 2012 it is likely to post mildly negative growth. The risk of implosion has dwindled over the last few months- peripheral economies like Greece, Italy and Spain have new governments in place and have made progress towards genuine economic reform. Even with some these positive factors in place, we have to accept the fact that global growth in 2012 will be

tepid

. But there is a flipside to this. Softer growth means lower demand for commodities, and this is likely to drive a correction in commodity prices. Lower commodity inflation will enable emerging market central banks to reverse their monetary stance. China, for instance, has already reversed its stance and have pared its reserve ratio twice. The RBI also seems poised for a reversal in its rate cycle as headline inflation seems well one its way to its target of 7 percent for March 2012. That said, oil might be an exception to the general trend in commodities. Rising geopolitical tensions, particularly the continuing face-off between Iran and the US, might lead to a spurt in prices. It might make sense for our oil companies to hedge this risk instead of buying oil in the spot market. As inflation fears abate, and emerging market central banks begin to cut rates, two things could happen. Lower commodity inflation would mean lower interest rates and better credit availability. This could set the floor to growth and slowly reverse the business cycle within these economies. Second, as the fear of untamed, runaway inflation in these economies abates, the global investor's comfort levels with their markets will increase. Which of the emerging markets will outperform and who will leave behind? In an environment in which global growth is likely to be weak, economies like India that have a powerful domestic consumption dynamic should lead; those dependent on exports should, prima facie, fall behind. Specifically for India, a fall in the exchange rate could not have come at a better time. It will help Indian exporters gain market share even if global trade remains depressed. More importantly, it could lead to massive import substitution that favours domestic producers.Let’s now focus on India and start with a caveat. It is important not to confuse a short run cyclical dip with a permanent derating of its long-term structural potential. The arithmetic is simple. Our growth rate can be in the range of 7-10 percent depending on policy action. Ten percent if we get everything right, 7 percent if we get it all wrong. Which policies and reforms are critical to taking us to our 10 percent potential? In judging this, let’s again be careful. Let’s not go by the laundry list of reforms that FIIs like to wave: The increase in foreign equity limits in foreign shareholding, greater voting rights for institutional shareholders in banks, FDI in retail, etc. These can have an impact only at the margin. We need not bend over backwards to appease the FIIs through these reforms they will invest in our markets when momentum picks up and will be the first to exit when the momentum flags, reforms or not. The reforms that we need are the ones that can actually raise our sustainable longterm growth rate. These have to come in areas like better targeting of subsidies, making projects in infrastructure viable so that they draw capital, raising the productivity of agriculture, improving healthcare and education, bringing the parallel economy under the tax net, implementing fundamental reforms in taxation like GST and the direct tax code and finally easing the

MYRIAD

rules and regulations that make doing business in India such a nightmare. A number of these things do not require new legislation and can be done through executive order.MYRIAD

...

MCQ-> Read the following passages carefully and answer the questions given at the end of each passage.PASSAGE 1In a study of 150 emerging nations looking back fifty years, it was found that the single most powerful driver of economic booms was sustained growth in exports especially of manufactured products. Exporting simple manufactured goods not only increases income and consumption at home, it generates foreign revenues that allow the country to import the machinery and materials needed to improve its factories without running up huge foreign bills and debts. In short, in the case of manufacturing, one good investment leads to another. Once an economy starts down the manufacturing path, its momentum can carry it in the right direction for some time. When the ratio of investment to GDP surpasses 30 percent, it tends to stick at the level for almost nine years (on an average). The reason being that many of these nations seemed to show a strong leadership commitment to investment, particularly to investment in manufacturing. Today various international authorities have estimated that the emerging world need many trillions of dollars in investment on these kinds of transport and communication networks. The modern outlier is India where investment as a share of the economy exceeded 30 percent of GDP over the course of the 2000s, but little of that money went into factories. Indian manufacturing had been stagnant for decades at around 15 percent of GDP. The stagnation stems from the failures of the state to build functioning ports and power plants and to create an environment in which the rules governing labour, land and capital are designed and enforced in a way that encourages entrepreneurs to invest, particularly in factories. India has disappointed on both counts creating labour friendly rules and workable land acquisition norms. Between 1989 and 2010 India generated about ten million new jobs in manufacturing, but nearly all those jobs were created in enterprises that are small and informal and thus better suited to dodge India’s bureaucracy and its extremely restrictive rules regarding firing workers It is commonly said in India that the labour laws are so onerous that it is practically impossible to comply with even half of them without violating the other half.Informal shops, many of them one man operations, now account for 39 percent of India’s manufacturing workforce, up from 19 percent in 1989 and they are simply too small to compete in global markets. Harvard economist Dani Rodrik calls manufacturing the “automatic escalator” of development, because once a country finds a niche in global manufacturing, productivity often seems to start rising automatically. During its boom years India was growing in large part on the strength of investment in technology service industries, not manufacturing. This was put forward as a development strategy. Instead of growing richer by exporting even more advanced manufactured products, India could grow rich by exporting the services demanded in this new information age. These arguments began to gain traction early in the 2010s.In new research on the “service escalators”, a 2014 working paper from the World Bank made the case that the old growth escalator in manufacturing was already giving way to a new one in service industries. The report argued that while manufacturing is in retreat as a share of the global economy and is producing fewer jobs, services are still growing, contributing more to growth in output and jobs for nations rich and poor. However, one basic problem with the idea of service escalator is that in the emerging world most of the new service jobs are still in very traditional ventures. A decade on, India’s tech sector is still providing relatively simple IT services mainly in the same back office operations it started with and the number of new jobs it is creating is relatively small. In India, only about two million people work in IT services, or less than 1 percent of the workforce. So far the rise of these service industries has not been big enough to drive the mass modernisation of rural farm economies. People can move quickly from working in the fields to working on an assembly line, because both rely for the most part on manual labour. The leap from the farm to the modern service sector is much tougher since those jobs often require advanced skills. Workers who have moved into IT service jobs have generally come from a pool of relatively better educated members of the urban middle class, who speak English and have atleast some facility with computers. Finding jobs for the underemployed middle class is important but there are limits to how deeply it can transform the economy, because it is a relatively small part of the population. For now, the rule is still factories first, not service first.According to the information in the above passage, manufacturing in India has been stagnant because there is

...

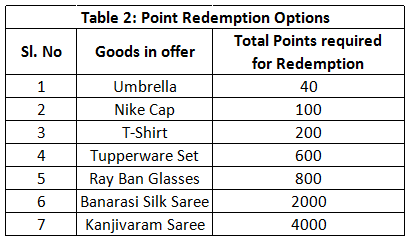

MCQ-> In order to quantify the intangibles and incentives to the multi brand dealers (dealers who stock multiple goods as well as competing brands) and the associated channel members, a

Company(X)

formulates a point score card, which is called as brand building points. This brand building point is added to the sales target achieved points for redemption. The sales target achieved point is allotted as per the table 3 of this question. The sum of brand building point and sales achieved points is the total point that can be redeemed by the dealer against certain goods, as shown in the second table.

The detail of the system is shown in the tables below

There are 10 multi brand dealers in Nasik and the sales that they have achieved in the end of a quarter are:

Maheshwari & Co has Company X signage along with other brand signage in the main entrance of the store, the exterior walls of the store have the painting of only company X, the side wall in the interior has the painting of Company X. The POP display of Company X is above the eye level with other brands while the stacking of goods of Company X is in the back row of the shelves. The brand building points when combined with the sales achieved points amounts to the total points that a dealer can accumulate in a quarter. The number of Tupperware Sets that Maheshwari & Co can redeem after the quarter (July to September) is?

...

×

×

Type The Issue

Terms And Service:We do not guarantee the accuracy of available data ..We Provide Information On Public Data.. Please consult an expert before using this data for commercial or personal use

Powered By:Omega Web Solutions

© 2002-2017 Omega Education PVT LTD...

Privacy

|

Terms And Conditions

Powered By:Omega Web Solutions

Powered By:Omega Web Solutions

There are 10 multi brand dealers in Nasik and the sales that they have achieved in the end of a quarter are:

There are 10 multi brand dealers in Nasik and the sales that they have achieved in the end of a quarter are:

Maheshwari & Co has Company X signage along with other brand signage in the main entrance of the store, the exterior walls of the store have the painting of only company X, the side wall in the interior has the painting of Company X. The POP display of Company X is above the eye level with other brands while the stacking of goods of Company X is in the back row of the shelves. The brand building points when combined with the sales achieved points amounts to the total points that a dealer can accumulate in a quarter. The number of Tupperware Sets that Maheshwari & Co can redeem after the quarter (July to September) is?

Maheshwari & Co has Company X signage along with other brand signage in the main entrance of the store, the exterior walls of the store have the painting of only company X, the side wall in the interior has the painting of Company X. The POP display of Company X is above the eye level with other brands while the stacking of goods of Company X is in the back row of the shelves. The brand building points when combined with the sales achieved points amounts to the total points that a dealer can accumulate in a quarter. The number of Tupperware Sets that Maheshwari & Co can redeem after the quarter (July to September) is?